Points make penalties

Share this article

Anton Lane examines the new penalty rules due to be imposed for the late submission of tax returns and the late payment of taxes

Key Points

What is the issue?

Late payment penalties and late filing penalties are changing, with the details published in the 2021 Budget tax documents.

What does it mean to me?

You need to be aware of the new penalty regime for late submissions and payments, as well as interest harmonisation, that could be more costly for clients who miss deadlines.

What can I take away?

Taxpayers need to be encouraged to meet payment and filing deadlines now. They need to be aware the rules are changing, or the outcome could be costly.

Details of the new late submission penalties, late payment penalties and harmonised interest announcements were published, as anticipated, in the 2021 Budget tax related documents. Also included was the consultation outcome in respect of ‘follower notices and penalties’.

The late submission and late payment penalties follow three consultations between August 2016 and March 2018, and the Policy Paper published on 6 July 2018. It was then proposed that the implementation will initially be for income tax self-assessment (ITSA) and VAT. Corporation tax currently remains outside the scope of the new late submission penalties, although the government has asserted that the new approach will apply in the future. The government estimates that the measures will raise £155 million per year by 2024/25.

The new penalty regime will apply to those taxpayers who persistently submit tax returns late and/or make payment of tax late, while at the same time being ‘more lenient on those who make the occasional slip up’. HMRC estimates that about 4 million individuals within the ITSA regime will benefit from the replacement of flat rate penalties with a points-based regime.

The Finance Bill 2021 includes provisions introducing the new penalties for:

- VAT taxpayers for periods starting on or after 1 April 2022;

- ITSA taxpayers with business or property income over £10,000 per year (who are required to submit quarterly digital updates through Making Tax Digital for ITSA) for accounting periods beginning on or after 6 April 2023; and

- all other ITSA taxpayers or accounting periods beginning on or after 6 April 2024.

Late submission penalties

Existing penalties

For ITSA, a taxpayer currently receives a late submission penalty of £100 as soon as a return is late, with a £10 daily penalty if the return is still outstanding three months after the deadline. A penalty of £300 or 5% of the tax liability (whichever is greater) becomes chargeable where a return is outstanding six months after the deadline and again at 12 months. Together, these penalties should not exceed 100% of the tax due.

There is currently no standalone late submission penalty for VAT. The Default Surcharge is a combined late payment and late submission sanction.

New penalties

Under the new penalty scheme for late submission, a taxpayer who misses a submission deadline will be notified by HMRC that they have received a ‘penalty point’ (not an actual penalty). Points accrue separately for VAT and income tax self-assessment. If a taxpayer accumulates a threshold number of points, they will receive a fixed financial penalty of £200.

If the taxpayer who has been issued with a fixed penalty continues to miss submission deadlines, they will be liable for a further fixed penalty for each additional missed obligation, even if they have paid the fixed rate penalty.

In principle, this sounds simple; however, the mechanics may make it more difficult in practice. HMRC has to levy and monitor points within a timeframe, and points may alter according to events (such as leaving VAT groups). It also has to monitor the reduction of points following periods of good compliance. Breach of thresholds need to be identified and penalties assessed. HMRC has discretion and taxpayers may request reviews or appeal.

IT automation is likely to monitor the accrual of points, although the legislation may require an officer to make assessments.

Multiple submission obligations

If the taxpayer has more than one submission obligation – for example, they are required to provide an annual ITSA return and quarterly VAT returns – they will be operating under more than one point system.

Where two or more failings relate to the same submission obligation in the same month, the taxpayer will generally only incur a single point for that month to prevent the taxpayer reaching the points threshold too quickly to be able to improve their compliance. However, this rule will not apply if the taxpayer has different MTD for ITSA submission obligations, such as a regular update deadline, an end of period statement and a final declaration in the same month.

If a taxpayer misses all three deadlines in a single month, they can incur three penalty points.

If a taxpayer with MTD for ITSA submission obligations has two or more businesses and is required to submit separate regular updates and end of period statements (EOPS) for each business, they will have a one point total for each of those submissions across the different businesses.

For example, a taxpayer with three businesses who fails to meet an ITSA regular update deadline in the same quarter for one, two or three of those businesses will therefore only accrue one point. If that taxpayer also misses the EOPS deadline for any or all of those businesses in the same period, they will accrue an additional point; and a failure to provide a final declaration for any or all of those businesses would accrue another point.

Expiration of points

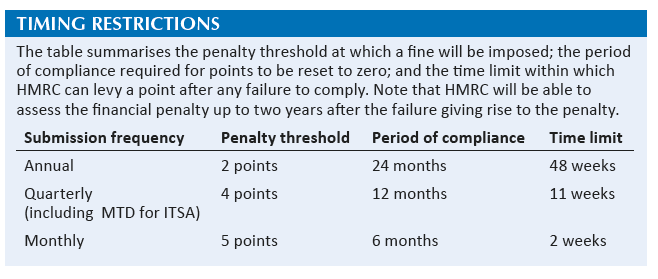

Points don’t live forever. Generally, points will automatically expire after 24 months, calculated from the month after the failure occurred, provided that the taxpayer remains below the points threshold. If the taxpayer reaches the penalty threshold, all points will expire after the taxpayer has met their submission obligations for a set period of compliance; and the taxpayer has submitted all the submissions that were due within the preceding 24 months. The period of compliance is linked to the taxpayer’s submission frequency (ranging from six months for monthly submissions to 24 months for annual submissions).

Additional information

HMRC can also levy points where it discovers previous submission obligations.

Where a tribunal decision results in the cancellation of a point or a financial penalty, HMRC will have 12 months from the date of the tribunal decision to levy a point or financial penalty that would have accrued for failures that occurred but were not added to the points total because the taxpayer was at the penalty threshold.

HMRC will have 12 months to add additional points following the date of discovery or the date of the tribunal decision.

A discretionary power will allow HMRC not to levy a point or charge a penalty. This power will be exercised in line with published guidance.

Where points have already been levied, those taxpayers who wish to challenge the levy must use the reviews and appeals process: internal review and/or appeal to the First-tier Tribunal. The appeal process will follow that against assessments of tax. Grounds of reasonable excuse will remain relevant.

Taxpayers can request changes to how often they submit their VAT returns, and HMRC can ask a business to change the frequency of returns (for example, asking a business to report their VAT monthly or quarterly instead of annually). To avoid penalising those who change their filing frequency, the taxpayer’s points will be adjusted according to the change they are making.

If changes are made to the taxpayer’s points total, the oldest points will be removed first (although not to below zero), and relevant time limits will be calculated from the most recent points. If points are added to their total, the time limits will be calculated from their most recent points.

The following mechanism will be used for the adjustment:

VAT groups

When the representative member of a VAT group is replaced, the new member will take over the points of the outgoing representative and the penalty points will not change.

However, where a group member leaves a VAT group and registers for VAT as a separate taxable person, they will start with zero points. Any previous penalties will remain with the original VAT group.

Upon forming a VAT group, any incurred penalty points accumulated by group members will not be transferred to the new group.

Non-standard accounting periods

Where submissions for non-standard accounting periods are agreed and periods are transitional, they will be excluded from the regime unless there is a deliberate failure to submit.

Late payment penalties

Existing penalties

The current penalties for late payment of ITSA amount to 5% of the unpaid tax due after three months; a further 5% penalty of tax outstanding after six months; and a further 5% penalty of tax outstanding after 12 months. If the taxpayer makes a time to pay agreement with HMRC, the penalty is suspended. HMRC extended the period for taxpayers to pay ITSA in 2021 without incurring penalties because of the impact of Covid-19.

For late payment of VAT, the Default Surcharge is a combined late payment and late submission sanction.

New penalties

The new late payment penalties will apply both to VAT businesses and ITSA taxpayers. The penalty consists of a first penalty; and an additional penalty with an annualised penalty rate.

Under the new regime:

- A taxpayer will not incur a penalty if the outstanding tax is paid within the first 15 days after the due date.

- After Day 15: the penalty is set at 2%of the outstanding tax.

- After Day 30: the penalty is set at 4%of the outstanding tax.

- After Day 31: an additional penalty is set on outstanding tax which accrues on a daily basis at 4% of the outstanding amount. This will stop accruing when the taxpayer pays the tax due.

A taxpayer can request a time to pay arrangement from HMRC and agree a schedule to pay any outstanding tax. This will stop a penalty from accruing any further from the day the taxpayer approaches HMRC, as long as the taxpayer honours the terms of the time to pay arrangement.

A taxpayer can request a time to pay arrangement from HMRC and agree a schedule to pay any outstanding tax, which will stop a penalty accruing any further.

HMRC has stated that it will take a ‘light-touch’ approach to the first penalty in the first year of operation. HMRC will not assess the first penalty at 2% after 15 days, allowing taxpayers 30 days to make payment or enter a time to pay agreement. This is, however, subject to the caveat that a taxpayer is doing their best to comply with the arrangement! Therefore, the first penalty that is charged will be the 4% rate at day 30.

HMRC does retain its discretionary power to reduce or not charge a penalty. The circumstances giving rise to the late payment will be considered during this assessment. If HMRC considers that the circumstances do not amount to a reasonable excuse, the taxpayer may request a review and/or appeal to the First-tier Tribunal.

Interest harmonisation

HMRC will charge late payment interest on tax that is outstanding after the due date, irrespective of whether any late payment penalties have been charged. Late payment interest will accrue on unpaid taxes, including amounts subject to a time to pay arrangement.

Interest will apply from the payment due date until the date received by HMRC. The interest rate will be 2.5% above the Bank of England base rate.

The rate of interest on overpaid tax is, of course, lower and is set at 1% less than the Bank of England base rate (with a minimum rate of 0.5%). Interest runs from the later of the last day the payment was due to be received or date received until date of repayment.