Practice makes perfect!

Share this article

Chris Mattos shares the results of a practice based study of what life could be like under HMRC’s Making Tax Digital proposals

Key Points

What is the issue?

The Making Tax Digital consultation document, ‘Bringing business tax into the digital age’, assumes a listing approach and thus an inherent problem is being proposed. I felt that it was important to go one step further to the theoretical arguments with a study of the potential effect of the proposed changes.

What does it mean to me?

Over 90% of members considered that compulsory digital record keeping and quarterly reporting will place an additional burden on their practice.

What can I take away?

The study showed that using an App to digitalise the accompanying paperwork was nearly 40% slower than recording just the transactions in Microsoft Excel.

On 18 March 2015, George Osborne announced the end to the tax return and painted a picture of a new digital relationship between HMRC and the taxpayer. Fundamentally, the majority of the tax profession seem to be in agreement that a move to digital recording is a good thing. This is on the basis that keeping track of a business’s finances is much easier as you go along than trying to recall events from more than 18 months ago. Since the Budget 2015 announcement, there has been much talk about ‘Making Tax Digital’, and particular concerns have been raised by the tax profession regarding the timetable to implement and the lack of referencing to the role of the tax agent.

On 15 August 2016, six consultation documents were released by HMRC which provided a high level overview of the intended changes together with the proposed legislation to allow the introduction of digital tax. The first of these consultation documents, ‘Bringing business tax into the digital age’, asked a number of questions (44 in total), which aimed to collect evidence to support the proposed new record keeping that HMRC envisages.

As a practitioner, and based on the concerns shared with me in my role as editor-in-chief of Tax Adviser magazine, I have repeatedly highlighted two themes which continue to give me cause for concern. Firstly, small businesses already have little time to juggle the demands placed on them, after all they are often managing director, head of finance, head of business development, head of IT, head of advertising, head of HR – the list goes on – and before all of these they have to run the day-to-day side of a business while often managing family commitments too. The changes assume that less time will be involved but I think only the most skilled project manager will see a similar level of administration.

The truth of the small business is that the owner is a passionate technician; a skilled baker of bread and pizza, a specialist lime plasterer or an IT Cloud expert. With all these demands on the owner’s hands it is not unusual for them to seek counsel to help them with the business side of their enterprise; a business coach, an entrepreneurial mentor, their accountant, or the latest management book. And the advice they receive: ‘Do what you are good at and earn the premium you can from that. Get others to do the tasks that are of lesser value.’

Makes sense. It is something I can testify to myself, as I’m not afraid to admit to not being a fan of payroll administration so have always outsourced my PAYE compliance.

The second theme, a point I highlighted in my April 2016 editorial for Tax Adviser, is that if there is to be a change in the digital relationship, some attention should also be given to an underlying tension between taxpayer and HMRC which I witness very regularly. This is the fear factor. The anxiety that clients have of doing things wrong. The brown envelope syndrome.

The solution of making things easier through software is definitely the way forward. My whole practice is based on the ability to file tax returns, do my own bookkeeping and retrieve clients’ files from the cloud. I like cloud based accounting software and am regularly using the associated App. But I understand the system and have 20 years of experience of accountancy and tax to help me. Clients don’t have this. If they did, why would they ever ask for help preparing even simple tax returns? Why do clients who have prepared their own tax and VAT returns before want my firm to help them? The answer is the relief that passing the records to someone they trust and the time saved trying to remember how the tax system works. I witness time after time relieved sighs and smiles which have replaced once anxious expressions.

But now a new message is emerging. A contradictory approach. Enter ‘John the plumber’ (via YouTube: http://tinyurl.com/h8hgrf9) and a proposal that it is much easier for a business to keep on track of its records in real time. There is absolute sense in this. Ask a small business about its finances close to the filing deadline and you get a blur – most of the January headaches come from a lack of memory of what passed over a year ago. But what skills does the accountancy and tax profession have to solve this inherent problem that is encountered year after year? We have the science of double-entry bookkeeping, the art of bank reconciliations and the sense of getting the balance sheet figures right. All of these are the skills of bookkeepers, accountants and tax advisers – I have met very few entrepreneurs that share them.

Of course, many clients already use some form of digital record keeping – we have a range of clients that use Excel and some that use online software. One of the biggest issues we find with clients that use digital records is incompleteness. As diligent as they are it is usual to find transactions that have been missed – regular direct debits without a timely invoice, or an invoice that is available online, are classic examples. The reason for this is that the client has taken a listing approach and so when they get to the end of their recording they do not have a way to check they have missed anything. Many of our bookkeeping queries to clients are for copies of invoices which haven’t been sent with the main batch we have received. How do we know about this missing paperwork? We have recorded all of the bank transactions and have reconciled these differences.

The consultation assumes a listing approach and thus this inherent problem is being proposed into the system.

Much of what I have noted above I have also heard from other commentators or members of the technical teams at CIOT, ATT and LITRG. Much of this has been relayed to HMRC. However, at this time of writing I am not sure these points are being seriously addressed, maybe because to date everything has been theoretical.

It is also worth noting that similar concerns were evident from the recent ‘Making Tax Digital – CIOT and ATT member survey’. Based on 1,082 responses, some of the key highlights included:

- More than 95% considered that compulsory digital record keeping and quarterly reporting will place an additional burden on their clients.

- More than 90% considered that compulsory digital record keeping and quarterly reporting will place an additional burden on their practice.

- Around 40% considered that compulsory digital record keeping and quarterly reporting will increase errors by their clients.

On the basis of the above, I felt that it was important to go one step further to the theoretical arguments with a study of the potential effect of the proposed changes. So we took three ingredients:

- A gap year student (with no experience of bookkeeping or tax, to be our ‘John the plumber’ – albeit with possibly more IT skills – I’m not sure they teach Excel pivot tables at plumbing college)

- A set of invoices and expense receipts for three businesses, already sorted into the proposed sections suggested by HMRC, which related to a recent VAT period; and

- The tools to record the transactions – an old style paper cash book, a PC (with Excel and access to super-fast broadband) and an iPhone.

Methodology

The study was performed using quarterly accounts from three different businesses – business A, an IT services provider (1 December 2015–31 March 2016), business B, a caterer and bakery (1 October 2015–29 February 2016), and business C, a plasterer (1 January 2016–31 March 2016) – all of which are clients of my firm, Chris Mattos Tax, Chartered Tax Advisers based in Stroud, Gloucestershire.

Performing the study was Patrick Dicks, a 20 year old with two years of experience studying mathematics, but no qualifications in accounting or business management (A-levels of A*, A and B in Maths, Further Maths and Physics respectively). I consider that Patrick’s level of relevant competency with regards to financial management is likely to be at least on a par with the majority of small business owners.

Aims

For each of these businesses, the aim was to record the quarterly account details via three different mediums; by handwriting, by a spreadsheet in Microsoft Excel and via Expensify, a market leading expenses recording App which includes auto-recognition scanning to detect name of supplier, date and cost. The App used for this study is one of the market leaders in the field of cataloguing expenses using auto-recognition. It has 2.5 million users and has been developed over the past seven years with over $15 million invested to date. Although cloud based accountancy software currently provides the ability to assign an image of the backing documentation (including via a photo), we were not aware of one that used an auto-recognition system to help record the transactions. Each of these nine total individual processes were timed, with difficulties and observations noted.

The key focus of the study is the difference in the timings between the different recording methods within each business. For example, business A used the App in a different way to the other businesses because all of its purchase invoices were received in digital format, so each of these was allocated to the relevant transaction. Businesses B and C were both recorded by photographing receipts and invoices using the mobile App. Any differences in timings were analysed to find out if any method stands out as being much faster. The final part of the study was to compare the accuracy of each method, to see if any method was prone to clear systematic errors when compared with the others.

Assumptions

It should be noted that accounts for each of the three businesses had already been filed and sorted prior to the study – by date and also by the categories outlined by HMRC. Clearly this is not representative of a real life situation for a small business owner, however, since this scenario is consistent between all three businesses, it is fair to assume that it does not affect the results.

Key results

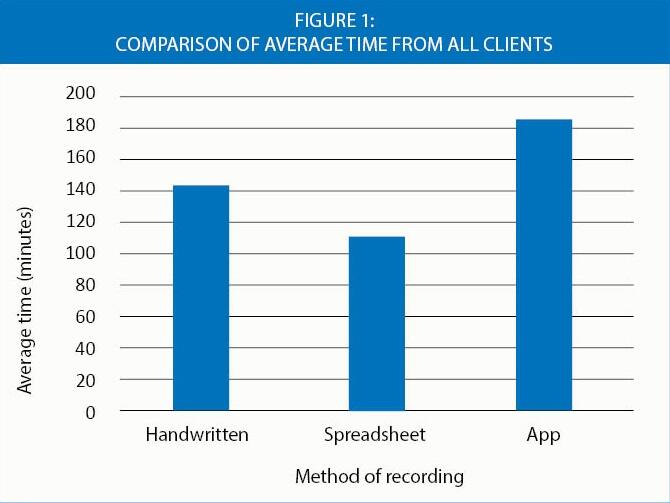

The study showed a considerable average difference in timings between the methods, notably that using an App to digitalise the accompanying paperwork was nearly 40% slower than recording just the transactions in Microsoft Excel, and even handwriting produces a quicker finished product than the mobile App, by about 20%. See figure 1.

In particular, business B required in excess of five hours work to digitally enter all details, over doubling the time when using a spreadsheet.

We found high error rates in the auto-recognition function, as high as 50%, and there is a high need of a manual override to get the correct recording.

In terms of the accuracy of the final output, all three methods were consistently similar for recording turnover. Use of the App, however, saw discrepancies between the recordings of expenses. Our concern is that if a logical methodology is followed businesses will be inclined to assume any App is robust and that they have entered a complete record of their transactions. The listing methodology does not give a business an approach which will allow them to double check their figures – such as a bank reconciliation.

The primary focus of analysis is the time each of these methods takes in recording the full accounts details; HMRC states that digitalising should make the process quicker and easier, but our results show that by taking a digital record of the backing documentation this will add to the time and costs to keep records.

Final thoughts

I have had the ambition of being a paperless office since my firm started a couple of years ago and the area that has held us back the most is how to move paper receipts into a digital format in an efficient way. This study has given us an opportunity to reflect on this and as a result we have acquired a specialist, multi-sized paper feed, super quick scanner. This will help us to digitalise our existing client records in a reasonable period and will also be a valuable a tool which will help us be ready for the increased work that we now expect as a result of the introduction of Making Tax Digital.