Real estate investment trusts

Share this article

David Westgate considers the purpose, benefits and process of becoming a REIT and the tax implications arising

Key Points

What is the issue?

The REIT structure has benefits but is accompanied by obligations.

What does it mean for me?

Whether to become a REIT means a number of important conditions must be considered in the context of the company’s business model.

What can I take away?

An overview of the tax structure of REITs and the applicable conditions.

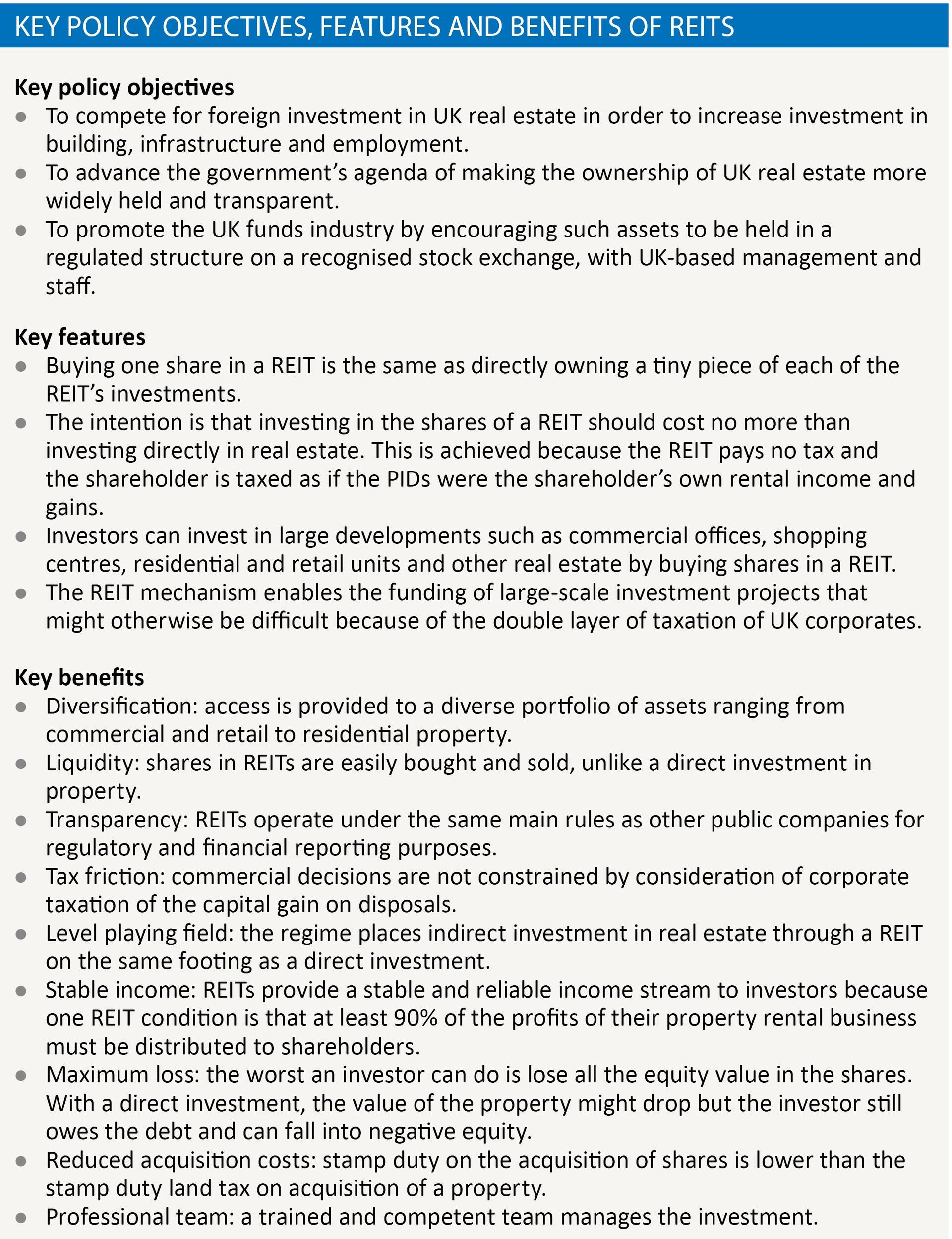

Subject to a number of conditions, a UK real estate investment trust (REIT) is a company, or a group of companies with a parent company, that has elected to be a REIT under the UK tax legislation.

The election exempts a REIT from paying corporation tax on its qualifying property rental income and capital gains. This removes the ‘double layer’ of taxation at company and shareholder level. Instead, a shareholder in the REIT pays tax on corporate dividends derived from its property rental business (called a property income dividend or PID) as if they were income and gains from the shareholder’s directly owned property rental business.

This mechanism is designed to place investors in a REIT on the same footing as direct investors in property. It enables them to access the risks and rewards of investing in a risk-diversified portfolio of property assets, which financial constraints would often make impossible if they had to buy property directly.

History

REITS started life in the US in 1961 when President Eisenhower signed into law the REIT Act. Congress wanted to allow investment in portfolios that comprise large-scale building projects that a single investor could not access individually, were diversified (having a minimum number of investments so that risks on one building were partly offset by risks on another) and income producing (primarily from rent).

US REITs had a chequered early history and the legislation was refined over time, improving competitiveness and enabling the REIT industry to flourish.

The key lessons learned from the development of US REIT legislation have shaped the development of REIT regimes around the world.

UK legislation

The initiative for UK REITs was driven by a desire to stem the flow of investment offshore and produce a well-regulated, liquid investment vehicle. The regime would also protect UK tax revenues because PIDs would be subject to withholding tax, accounted for through a CT61, unless specifically exempted.

The UK REIT regime was finally launched on 1 January 2007. The legislation has been rewritten into Part 12 of the Corporation Tax Act 2010 (CTA 2010) and there have been updates in FA 2012, FA 2013 and FA 2014 to enhance the regime’s attractiveness.

Becoming a REIT

For a company (or the principal company of a group) to become a UK-REIT, under CTA 2010 ss 523-524 it must file a written notice specifying a start date.

A company may give notice only if it is UK tax resident and is not an open-ended investment company (OEIC). In addition, it must meet several conditions in every accounting period. These are outlined below.

Change in tax basis on becoming a REIT

On entering the REIT regime, the accounting period for a company’s property rental business (PRB) will cease and a new accounting period will commence for corporation tax purposes. The deemed cessation does not apply to any other non-PRB ‘residual’ activities carried on by the company before entering the REIT regime.

At the point of entry, the assets used in the existing PRB will be rebased to market value, any consequential gains or losses being ignored.

Losses pertaining to the pre-entry PRB cannot be used in the post-entry PRB and vice versa.

After entry, PRB rental income and capital gains on sales of investments used in the PRB, will not be subject to corporation tax. Under IFRS accounting, any deferred tax liabilities recognised on investment properties in the PRB are not required.

Capital allowances are deemed to be transferred into the REIT regime at their tax written down value, and no balancing allowances or charges arise. They must be claimed under the REIT ‘shadow’ regime, by which the calculation of PRB for PID purposes is calculated on a corporation tax basis. Thus, capital allowances are a key driver in managing the PID.

REIT conditions and tests

A UK REIT must comply with various conditions and tests. These are set out in CTA 2010 Part 12 supplemented by the HMRC manuals under “Guidance on real estate investment trusts” (though some of this needs updating).

The UK REIT conditions and tests can be thought of as having two broad objectives: the protection of tax revenue and the reduction of risk for investors.

Company conditions

These conditions must be met if a company wishes to become a UK REIT. They achieve the government’s prime objective of ensuring a wide investor base, liquidity in the shares (which must be listed or traded on a recognised exchange) and transparency (due to the market scrutiny of being listed on a stock exchange and conforming to the exchanges regulations).

Key company conditions under CTA 2010 s 528:

- UK tax resident (dual resident companies are not permitted).

- The REIT must not be an open-ended investment company, meaning it will issue a fixed rather than floating number of shares.

- The company’s shares must be listed or admitted to trading on a recognised stock exchange and this is subject to a three year grace period for new REITs.

- Cannot be a ‘close company’ (ie not controlled by five or fewer participators) though this is subject to a three-year grace period for new REITs.

- Only one class of ordinary shares may be listed or traded on a recognised exchange. The only other class of shares it may issue is non-voting restricted fixed rate preference shares which can only be convertible into ordinary shares.

- A REIT’s debt may not be linked to business activity ie its results.

Property rental conditions

This condition is consistent with spreading investment risk across a diversified investment portfolio. In addition, an upper limit prevents too large an investment by a REIT in a single asset.

Key property rental conditions under CTA 2010 s 529:

- The UK REIT must own at least three single rental properties throughout each accounting period. Rental property includes leasehold interest.

- The condition is satisfied if you let three separate units in a multi-let property.

- No one property or leasehold interest can account for more than 40% of the fair value of the gross assets of the PRB.

- Owner-occupied properties are excluded from the above.

Balance of business condition

A key principle of the investment activity of a UK REIT is that there is a separation of the ‘tax-exempt’ PRB and other taxable ‘residual’ business activities. A qualifying PRB is a UK or overseas property business that generates its income from land for rent and this is defined further in CTA 2009 s 207. Rental income does not include income from the ‘occupation’ of land, such as farming, or trading in land by development and sale, which is considered a ‘residual’ activity.

This separation into two distinct businesses ensures that at least 75% of the profits and assets relate to the low-risk, tax-exempt business. Up to 25% of profits and assets can arise from residual activities such as development activity, allowing management – to a controlled extent – to operate a mix of businesses.

The income and gains arising in the residual business are subject to corporation tax in the normal way, and the ring-fencing of the two businesses ensures that there is no cross-contamination of losses.

Key balance of business conditions under CTA 2010 s 531:

- In the accounting period at least 75% of a REIT’s total income-profits (before tax) must arise from its tax-exempt PRB.

- At the beginning of the accounting period at least 75% of the total fair value of the assets of the REIT must comprise assets involved in its tax-exempt PRB.

This condition is tested using the company or consolidated group results prepared under IFRS and adjusted for non-recurring items.

Distribution condition

This condition ensures that investors receive high levels of income from the qualifying PRB, thus providing stable long-term income and certainty for investors. A high distribution requirement also protects the UK tax base because the point of taxation for a UK REIT is in the hands of investors, where distributions may be subject to withholding tax at 20%. Distributions from the PRB in the hands of investors are taxed as a PID and distributions from the residual business are taxed as ordinary dividends in the normal way.

UK investors are subject to tax at their marginal rate, with an offset for any withholding tax suffered. UK pension funds and some other types of investor can claim exemption from withholding tax. Non-UK investors should consider the relevant double tax treaties.

Key distribution conditions under CTA 2010 s 530:

- A UK company or principal company of a group REIT must distribute at least 90% of the profits of its PRB calculated on a tax basis. Since FA 2013, it must also distribute 100% of any PID received from another UK REIT (which is not taxable in the investor company).

- The distribution must be made by way of ordinary dividend. Since FA 2012, a stock dividend will satisfy this requirement. See CTA 2010 s 530 (6A)-(6D).

- The distribution must be made on or before the filing date of the company’s tax return for the accounting period.

- In the hands of investors, the PID is taxable as property rental income rather than dividends. The recently introduced £5,000 allowance for dividends received by individuals is not available. However, the PID is still treated as a dividend under double taxation conventions.

Financing restriction

This condition ensures that the REIT is not so highly geared that high interest costs significantly reduce the level of income to be distributed to investors or increase risk for them. This condition also reduces the scope for extracting profits of the REIT exempt business as interest rather than a PID (which is subject to withholding tax).

Explanation of the financing restriction under CTA 2010 s 543:

- The UK REIT regime uses a ratio test that compares profits of a UK REIT’s tax-exempt business with its financing costs. Both the profits and financing costs are calculated in accordance with CTA 2010 s 544.

- The tax-exempt profits must be at least a 1.25 multiple of financing costs.

- The REIT will be subject to a tax charge if there is excess interest, although the tax charge can be waived in certain conditions as per CTA 2010 s 543 (7).

Corporate ownership restriction (holder of excessive rights)

Because any income distributed by a UK company would normally be treated as an ordinary dividend, a corporate, overseas shareholder that is beneficially entitled to 10% or more of the shares might benefit from a reduced rate of withholding tax.

To avoid these shareholders receiving substantial dividends, taxed at a low or zero rate, the Treasury introduced a revenue protection measure, which imposes a tax charge on the REIT if it pays a dividend to a holder of excessive rights.

Explanation of the ownership restriction under CTA 2010 ss 551-554:

A tax charge will apply if a distribution is paid to a company or entity that is either beneficially entitled (directly or indirectly) to 10% or more of the dividends paid, 10% or more of the share capital, or controls 10% or more of the voting rights in the principal company.

Three-year development rule

A threshold is in place that broadly aims to distinguish between trading for a profit and normal development of an investment asset.

Explanation of the development rule under CTA 2010, s 556:

Where a property has been acquired by the company or the group which is a member of a UK REIT and:

- the property has been developed since acquisition

- the cost of the development exceeds 30% of the fair value of the property at the later of the date the company acquired the property or the date the company joined the regime, and

- the company disposes of it within three years of completion of the development,

the asset is treated as having been disposed of in the course of the company’s residual business. A chargeable gain is calculated in the normal way and subject to corporation tax.

Important bear traps to consider

Some transactions can have an adverse impact on the balance of business test or the PID. These include but are not limited to hedging transactions, overage payments, fair value movements through the income statement and significant levels of property development.