Reverting to the standard annual investment allowance: Impact on incorporated businesses

Share this article

In the second part of our feature on the end of the temporarily increased annual investment allowance on 31 March 2023, we examine the impact which the reversion to the standard allowance will have on businesses within the charge to corporation tax.

Key Points

What is the issue?

The alignment of the change in the corporation tax rate with both the annual investment allowance (AIA) limit change and the end-date of the super deduction within that period can again make timing of qualifying expenditure and the accounting date sensitive.

What does it mean for me?

The corporation tax effect of expenditure within the relevant limits will be determined by the ratio of months in that period which fall before and after midnight on 31 March 2023.

What can I take away?

The effective tax rate applied to the AIA on expenditure incurred in the second straddling period will vary depending on a company’s year-end, with the rate increasing the later that year-end falls in the financial year to 31 March 2024.

As the temporarily increased annual investment allowance (AIA) is due to revert to the standard £200,000 AIA limit from 1 April 2023, the transition period will have potentially significant impacts on businesses claiming the allowance, resulting in some surprising results in relevant tax assessments. The first part of this article was published in the April 2022 issue of Tax Adviser. Here, we examine the impact of the transition on incorporated businesses.

Incorporated businesses with a second straddling period do not have to contend with the basis period transitional rules. However, the alignment of the change in the corporation tax rate with both the AIA limit change and the end-date of the super deduction within that period can again make timing of qualifying expenditure and the accounting date sensitive.

The government announced at the Spring Statement that it is considering ways to incentive business to increase capital investment, with a view to announcing proposals at the Autumn Budget (see the Capital section at bit.ly/3Kpou0F). This article ignores the impact of any changes which may result from that review and must be read accordingly.

Profits charged at main rate of corporation tax

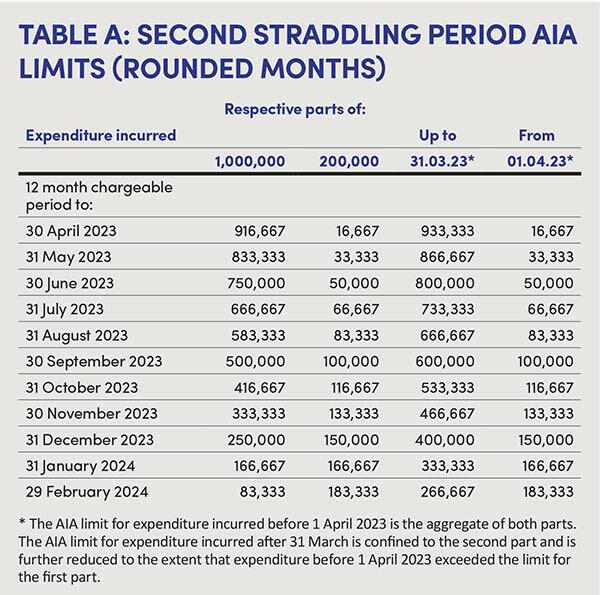

The AIA limits in respect of qualifying expenditure incurred in the second straddling period will vary, as shown in Table A, by reference to the date of expenditure. The corporation tax effect of expenditure within the relevant limits, however, will be determined by the ratio of months in that period which fall before and after midnight on 31 March 2023. For example, a main rate company with a 31 December 2023 year end will have three twelfths of its total AIA for the second straddling period relieved at 19% and the other nine twelfths relieved at 25%.

On qualifying expenditure of £400,000 (incurred before 1 April 2023 in that second straddling period), the corporation tax relief for that company is £94,000:

(3/12 x £400,000 @19%) + (9/12 x £400,000 @ 25%)

This amounts to an overall effective rate of 23.5% on the expenditure. By contrast, that same £400,000 of AIA qualifying expenditure in the previous accounting period to 31 December 2022 would have attracted corporation tax relief at only 19% (relief of £76,000). This demonstrates why the super deduction was needed to incentivise investment in plant and machinery before the corporation tax rate increase on 1 April 2023.

However, if the expenditure of £400,000 was instead incurred by the same company in the nine months from 1 April 2023, the AIA cap of £150,000 would apply (as shown in Table A). Whilst the 19% and 25% rates would still apply for the respective parts of the second straddling period, the capping of the AIA would limit its effect in that period to a tax reduction of only £35,250:

(3/12 x £150,000 @19%) + (9/12 x £150,000 @ 25%)

Ignoring any writing down allowances on the £250,000 balance of expenditure which attracted no AIA, the effective rate of relief on the £400,000 expenditure would be just 8.8%.

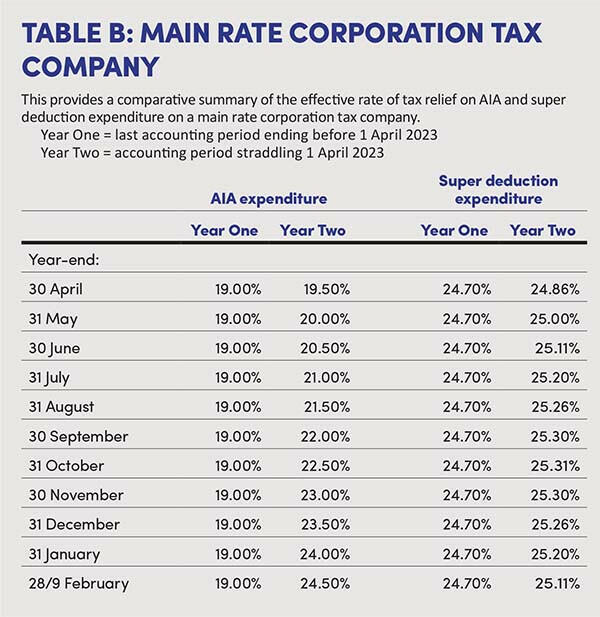

The effective tax rate applied to the AIA on expenditure incurred in the second straddling period will vary depending on a company’s year end, with the rate increasing the later that year end falls in the financial year to 31 March 2024. With a year end of 30 April 2023, it is only 19.5%; with a year-end of 29 February 2024, it is 24.5%. Table B summarises the effective rates on AIA qualifying expenditure within the relevant limits with different year ends (this needs to be read in conjunction with Table A). In the example just given, the use of a company with a 31 December year end meant that its £400,000 expenditure (if incurred before 1 April 2023) was exactly at the AIA limit.

If the expenditure of £400,000 by the same main rate company with a 31 December year end was incurred in the three months before 1 April 2023 and qualified for the super deduction, what would the tax effect be?

Because that expenditure occurred in a chargeable period which ended on or after 1 April 2023, the headline rate of 130% for the super deduction would be subject to the reduction required by Finance Act 2021 s 11. That prevents the company benefiting from both the uplifted rate of allowance and relief at 25% on part of that allowance.

This ‘damping’ of the super deduction is achieved by restricting the 30% bonus element in proportion to the part of the period which falls before 1 April 2023. So, for our 31 December year end company, the super deduction factor is not 130% but 107.5%:

(100 + 3/12 x 30)%

The uplifted amount of £430,000 (£400,000 x 107.5%) would produce a tax reduction of £101,050:

(3/12 x £430,000 @19%) + (9/12 x £430,000 @ 25%)

This gives an overall effective rate of 25.26% on the £400,000 of expenditure.

That same level of super deduction qualifying expenditure in the previous accounting period to 31 December 2022 would produce corporation tax relief of £98,800 (£400,000 x 130% x 19%), giving a slightly lower effective rate of 24.7%.

The effective tax rate applied to the super deduction on expenditure incurred in the second straddling period (in AIA terms) varies only slightly with different year ends. The rate increases gradually from 24.86% with a year end of 30 April 2023 to 25.31% with a year end of 31 October, before easing back to 25.11% with a year end of 29 February 2024. (Table B summarises the effective rates with different year ends.)

The effective rate of relief on AIA qualifying expenditure within the relevant limit for a main rate company relief, if incurred in the second straddling period, is determined by a combination of the company’s year end and any capping of the AIA by the transitional rules. By contrast, the effective rate of relief on super deduction qualifying expenditure incurred (necessarily before 1 April 2023) in that period will be close to 25% regardless of the company’s year end.

Profits charged at small profits rate

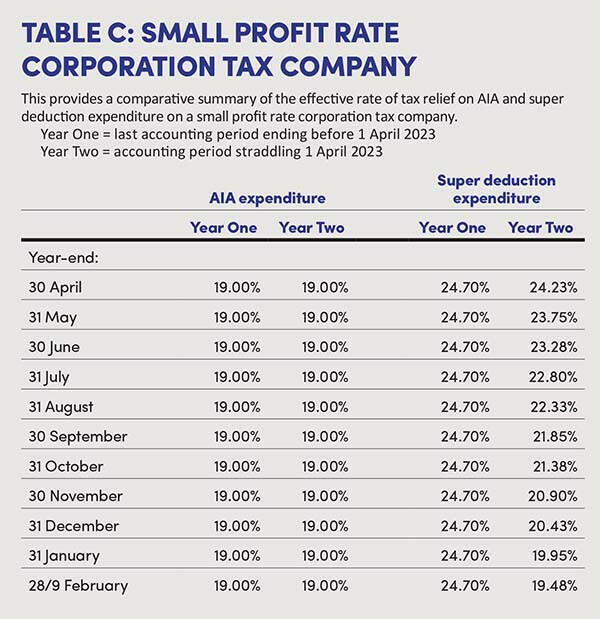

For a singleton company (i.e. a company that is not a member of a group), where the whole of its taxable profits for the second straddling period would be charged at the small profits rate even if they had no AIA entitlement (because they did not exceed £50,000), any AIA qualifying expenditure within the relevant limit would necessarily be relieved at 19% – as it would have been in the previous chargeable period and as it would be in the subsequent chargeable period (assuming no change in the small profits rate or limits). For example, if such a company had a 30 June year end, the effective rate of relief would be a flat 19% whether it incurred £20,000 of AIA qualifying expenditure in its second straddling period to 30 June 2023, the preceding period to 30 June 2022 or the succeeding period to 30 June 2024. The only sensitivity of timing of expenditure by such a company would be confined to any impact of the transitional rules on AIA limits (see Table A), which would not be relevant in this example.

If instead that same level of expenditure was incurred by the company before 1 April 2023 in the second straddling period and qualified for super deduction, the effective rate of relief would not be quite so predictable. The super deduction would be subject to the same ‘damping’ as described above for a main rate company, despite the company being unable to obtain tax relief at 25% from 1 April 2023. As nine months of its period to 30 June 2023 fell before 1 April 2023, its super deduction entitlement would be £24,500:

£20,000 x (100 + 9/12 x 30)%

As the company’s corporation tax rate both up to 3 March 2023 and from 1 April 2023 would be a constant 19%, the effective rate of relief on the expenditure would be 23.28%:

£24,500 x 19% / £20,000

That same level of super deduction qualifying expenditure in the preceding period to 30 June 2022 would have enjoyed the same effective rate of relief of 24.7% as any other company.

Table C summarises the effective rates of relief for both AIA and super deduction with different year ends and demonstrates the increased damping effect with later year ends. It will be seen that the timing of AIA qualifying expenditure by a company within the small profits rate is only sensitive if the AIA transitional capping rules apply (Table A). By contrast, super deduction qualifying expenditure of such a company is more effective if incurred in its accounting period which ends before 1 April 2023.

Profits eligible for marginal relief

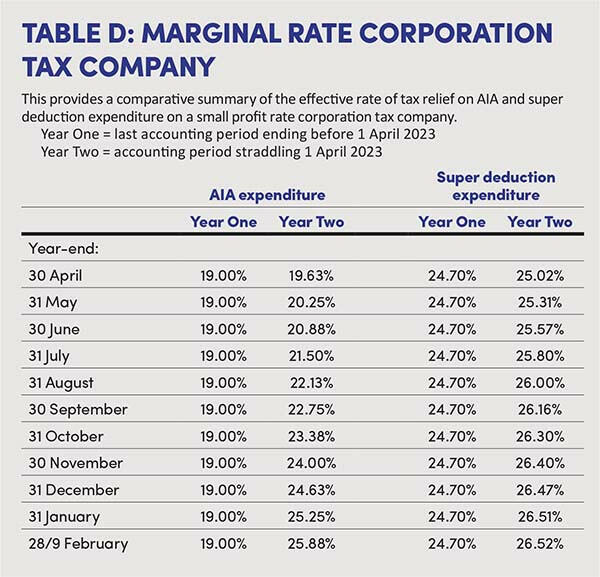

For a singleton company whose taxable profits in the second straddling period without any AIA expenditure would otherwise lie between the £50,000 and £250,000 thresholds, the timing of any AIA expenditure can be significantly more sensitive than for a company within the small profits rate. For example, take such a company with a 31 October year end, an identified need to incur qualifying expenditure of £180,000 sometime in the 14 months between (say) 1 October 2022 and 30 November 2023, and taxable profits (ignoring that planned expenditure) regularly around the £250,000 level. If that expenditure was incurred in October 2022, it would create an entitlement to AIA of £180,000 which would result in a tax reduction for the period to 31 October 2022 of £34,200 (£180,000 @ 19%).

Incurring that expenditure in the five months to 31 March 2023 would again create an entitlement to AIA of £180,000 (which would be within the cap for the first part of the second straddling period). However, in this case the corporation tax rate change would mean that five twelfths of that would attract relief at 19% (so £14,250) and seven twelfths would attract relief (in simplified terms) at the effective marginal small profits rate of 26.5% (so £27,825), giving a combined tax reduction of £42,075 and an overall effective rate of relief of 23.38%.

By contrast, incurring that same expenditure of £180,000 in the seven months starting from 1 April 2023 would, for a company with a 31 October year end, create a capped entitlement to AIA of £116,667 (see Table A). Five twelfths of that capped amount would attract relief at 19% (so £9,236) and the other seven twelfths would benefit from the marginal rate of 26.5% (so £18,035). This would give a combined tax reduction of £27,271 for the period and an overall effective rate of relief of only 18.47% on the £180,000 expenditure (ignoring writing down allowance on the non-AIA eligible amount taken to the pool).

If the company was able to defer the same expenditure until after 31 October 2023, AIA would be available on the whole £180,000 and the whole of that amount would be relieved at the marginal rate of 26.5% giving a tax reduction of £47,700.

For the same company, if the £180,000 expenditure could be incurred in the five months before 1 April 2023 and qualify for the super deduction, that allowance would be damped from 130% to 112.5%:

(100 + 5/12 x 30)%)

Five twelfths of the allowance of £202,500 (£180,000 x 112.5%) would be relieved at 19% (so £16,031) and seven twelfths would be relieved at 26.5% (so £31,303), giving a combined tax reduction of £47,334 and an effective rate of relief of 26.3%. Had that super deduction qualifying expenditure of £180,000 been incurred in the company’s year to 31 October 2022, it would have benefited from an effective rate of relief of 24.7%.

The reintroduction of the marginal rate from 1 April 2023 inevitably makes the timing of expenditure more sensitive. In the scenario just considered, there is a danger zone for AIA qualifying expenditure incurred in the months of the second straddling period which fall after 31 March 2023 because of the transitional rules. Super deduction qualifying expenditure in the months to 31 March 2023 would benefit from a greater effective rate of relief than if that expenditure had been incurred in the previous period. However, in the particular scenario, the most beneficial rate of relief (just) arises where the expenditure is incurred in the subsequent period, the accounting period which begins after 31 March 2023.

Hopefully, you will be able to rely on your software to make all the right calculations. Maybe, however, this article will be helpful in explaining why your software’s answers appear a bit counterintuitive.