Annual investment allowance: reverting to the standard limit

Share this article

Unless there is a further extension to the temporarily increased annual investment allowance, the transitional provisions will apply to any chargeable period which straddles 1 April 2023. We examine the impact on unincorporated businesses

Key Points

What is the issue?

The reversion to the standard £200,000 AIA limit from 1 April 2023 means that the more months in the second straddling period that fall after 31 March 2023, the lower will be the overall AIA limit for that whole period and the greater the potential benefit of incurring any qualifying expenditure before that date.

What does it mean for me?

The conjunction of the transitional rules for both the AIA and basis periods can produce surprising results in the 2023/24 assessment.

What can I take away?

Taxpayers with a 5 April year end should take great care to avoid being treated as having incurred qualifying expenditure in any of the five low-scoring days at the beginning of April 2023.

The annual investment allowance (AIA) has been with us for 14 years, helpfully blurring the tax significance for many taxpayers of whether expenditure is capital or revenue. In the last nine years, however, the AIA’s more affluent cousin, the temporarily increased AIA, has usurped the AIA’s position as the really useful capital allowance. In 87 of the 123 months between 1 January 2013 (when the temporarily increased AIA arrived) and 31 March 2023 (when it is next scheduled to depart), the temporarily increased AIA will have held sway, although the levels of both allowances have varied in that period (see Table A).

I wrote an article for Tax Adviser in March 2013 which highlighted the arithmetical intricacies required by the transitional provisions when the temporarily increased AIA arrived or departed during a chargeable period. Broadly speaking, the provisions applying whenever the temporarily increased AIA expenditure ceiling is introduced during a chargeable period (or increased as happened from April 2014) are logical. The provisions which apply whenever the ceiling reverts to the standard AIA level are by contrast counterintuitive.

Successive extensions to the duration of the temporarily increased AIA have meant that there has so far been only one occasion when the limit reverted to the standard AIA level – on 1 January 2016. Businesses whose chargeable period aligned with the calendar year were spared any strange arithmetic. However, for a business with (say) a 31 March 2016 year-end, the transitional provisions meant that, if all its qualifying expenditure on plant and machinery in that chargeable period was incurred in the three months from 1 January 2016, its actual AIA limit was only £50,000 (three twelfths of £200,000). By contrast, the limit for expenditure in the first nine months of that period would have been £425,000 (nine twelfths of £500,000, plus three twelfths of £200,000).

Unless there is a further extension to the temporarily increased AIA, the ending of the current extension to 31 March 2023 (announced in the 27 October 2021 Budget) means the transitional provisions in Finance Act 2019 Sch 13 para 2 will apply to any chargeable period which straddles 1 April 2023 (defined in the legislation as the second straddling period).

In this article, I assume that there will be no extension of the temporarily increased AIA beyond 31 March 2023 and that the standard level of AIA will remain at £200,000. Unless otherwise indicated, all calculations use rounded months for simplicity, even where statute requires calculations to be made in days. The whole article considers the implications of capital expenditure for businesses with a year-end other than 31 March.

The choice of 31 March 2023 as the departure date for the temporarily increased AIA is understandable. For incorporated businesses, it coincides with the scheduled end-date for both the 130% super deduction and the 50% special rate allowance, and the introduction from 1 April 2023 of the 25% corporation tax rate. For unincorporated businesses, it avoids adding complexity to the calculations of taxable income for 2023/24 in which the unrelated transitional rules for basis periods may apply.

The reversion to the standard £200,000 AIA limit from 1 April 2023 means that the more months that fall after 31 March 2023 in the second straddling period, the lower will be the overall AIA limit for that whole period, and the greater the potential benefit of incurring any qualifying expenditure before that date. That is the case for both incorporated and unincorporated businesses.

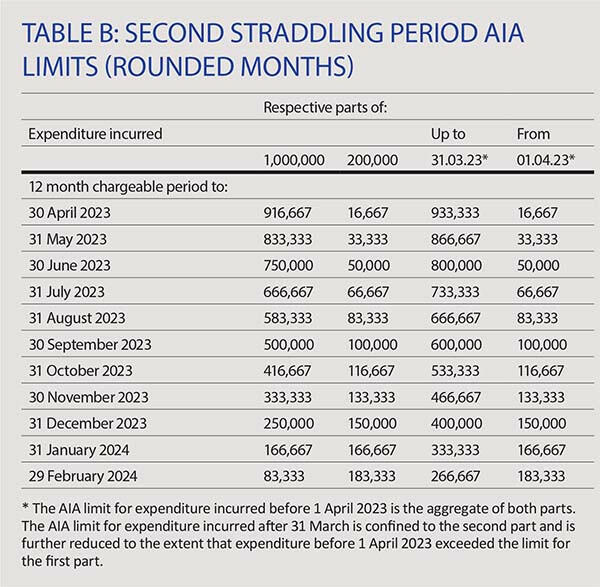

Table B summarises the effective AIA limit in the second straddling period with different year ends, assuming that the standard AIA limit will remain at £200,000:

- The limit for expenditure incurred before 1 April 2023 is the aggregate of the time-apportioned parts of the £1 million and £200,000 limits.

- By contrast, the limit for expenditure after 31 March 2023 is confined to the time-apportioned part of the £200,000 limit. That is further restricted to the extent that expenditure before 1 April 2023 ‘borrowed’ AIA from the later part of the period. Such borrowing would occur, for example, if expenditure before 1 April 2023 exceeded the time-apportioned part of the £1,000,000 limit.

The tax saving effect of AIA eligible expenditure in the second straddling period will of course depend on the tax rate at which profits are charged.

Implications for unincorporated businesses

For any unincorporated business with a second straddling period other than one which ends between 1 and 5 April 2023, the taxable profits of that chargeable period will be assessable for 2023/24. However, the time-apportioned profits for the months from the end of the second straddling period up to 5 April 2024 (the ‘transition part’) will also be assessed in 2023/24 (because of the abolition of basis periods – see the Finance Act 2022 Sch 1 para 65). For example, the 2023/24 assessment for a business with a 31 October year end will be:

- the aggregate of its profits for the year to 31 October 2023 and its profits for the subsequent five months to 31 March/5 April 2024 (determined by time-apportionment);

- less any permitted adjustments in respect of overlap profits, spreading of the transition profits, etc.

Any capital allowances due on expenditure incurred at any time in the year to 31 October 2024 would in that situation be subjected automatically to that time-apportionment. This transitional stretching of the basis period has the potential to change the marginal tax rate on the income assessable in 2023/24. It also gives added significance to the capital allowances that can be claimed for 2023/24, whether related to expenditure in the second straddling period or in what I refer to as the succeeding period – the period whose profits have to be time-apportioned.

The conjunction of the transitional rules for both the AIA and basis periods can produce surprising results in the 2023/24 assessment. Whereas the timing of expenditure within the second straddling period is critical, the impact in that assessment of AIA on expenditure incurred in the succeeding period depends not on the timing of the expenditure within that period, but rather on how many of the months in that period fall in the tax year to 5 April 2024. Expenditure incurred after that date is just as effective as expenditure incurred on or before that date; however, the more months in that period which fall after that date, the less tax relief will be due on that expenditure, even if it was incurred on or before 5 April 2024.

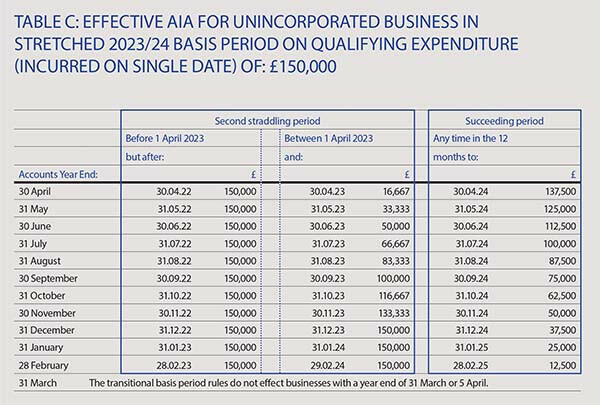

Table C compares the effective AIA available in the 2023/24 assessment on a single item of qualifying expenditure of £150,000 incurred at different times between the beginning of a business’s second straddling period and the end of the succeeding period.

Table C shows that, regardless of the accounts year end, full AIA is available in the 2023/24 assessment on expenditure of £150,000 incurred before 1 April 2023. However, if expenditure of £150,000 is incurred after 31 March 2023, the interaction of the two separate transitional provisions is more complex. If the second straddling period ends before 1 August 2023, it will (at that level of expenditure) be more effective to delay the expenditure until the succeeding period. Conversely, if the second straddling period ends after 31 August 2023, the 2023/24 assessment would benefit more if the expenditure was incurred in the second straddling period than in the succeeding period. It is essential to appreciate that the advantage between incurring expenditure before and after the end of the second straddling period changes with the level of expenditure in addition to the accounts year end.

Before concluding, it is appropriate to consider the impact of the AIA transitional provisions on a business with a year end of 5 April 2023. Section 12 of the Finance Act 2022 gives no indication of any exceptional treatment for a business which has only five days after 31 March 2023. Such a business (typically but not necessarily unincorporated) therefore has an aggregate AIA ceiling for its second straddling period of £989,041:

(360/365 x £1,000,000) + (5/365 x £200,000).

Expenditure up to that level could all qualify for AIA if incurred before 1 April 2023. However, expenditure incurred in the five days up to 5 April 2023 would have an AIA ceiling of just £2,740, even if the business had no qualifying expenditure in the whole of the previous 360 days.

A quick revision on when expenditure is treated as incurred for capital allowance purposes might be useful at this stage (see Capital Allowances Act 2001 s 5 and any more specific provisions which might be relevant) before advising any client with a 5 April year end that they should take great care in agreeing dates, delivery times, etc. in order to avoid being treated as having incurred qualifying expenditure in any of these five low-scoring days at the beginning of April 2023. A practical alternative could be to adopt a 31 March year-end starting with the accounts year to 31 March 2023 (or indeed 2022), although any wider implications of this would need careful consideration.