Saving VAT on builder services: when the 5% rate applies

Share this article

Work carried out by builders is sometimes subject to 5% VAT rather than 20%, a big saving for property owners who cannot claim input tax. The lower rate applies in three main situations.

Key Points

What is the issue?

Builders often prefer to ‘play safe’ and charge 20% VAT on their services, even when the 5% rate might apply. As well as increasing the project cost to building owners who cannot claim input tax, there will also be a problem if owners claim input tax based on a 20% VAT charge when 5% should apply.

What does it mean to me?

Make sure your builder and property clients are aware of the three main situations when 5% VAT applies to builder services: the conversion of a non‑residential building into a dwelling or building to be used for a relevant residential purpose; work on a dwelling that has not been lived in for at least two years; and a project that will result in a change in the number of dwellings.

What can I take away?

The VAT savings with the 5% rate can be considerable, especially as the rate extends to materials provided by builders as part of their work. And the savings can be further extended by having a ‘design and build’ project; i.e. a lower rate of VAT will also extend to professional fees.

The starting point with any supply of goods or services in the UK is that they are subject to VAT at 20%. You must then consider if there is a potential window in the legislation for either zero-rating or exemption to apply or, in some cases, a reduced rate of 5%. I will focus on the latter rate in this article and when it applies to builder services.

Materials and labour

In the case of builder services subject to 5% VAT, there is an extra ‘win’ because the reduced rate also applies to any materials provided by builders as part of their work. So, if a plumber supplies labour and materials to fit a new bathroom suite, the entire job will be subject to 5% VAT if the labour charge qualifies for the lower rate.

Materials purchased on a stand-alone basis from, say, builder merchants are always standard rated. It is therefore logical for property owners to buy materials through their chosen builders and save 15% VAT, as long as the builder doesn’t wipe out the VAT saving by applying a mark-up of 16% or more for the materials in question.

Situation 1: Non-residential building converted to residential use

I recently read that a stone-built church is being sold in Scotland, and it was described as having ‘potential for development or conversion’. The logical outcome is that the church will be purchased by a property developer and converted into flats which will then be rented out or sold when they are complete.

This is the first situation when builder services will qualify for 5% VAT, when a non-residential building is converted into either dwellings or a building that will be used for a ‘relevant residential purpose’. Dwellings include houses, bungalows, apartments and bedsits (see VAT Notice 708 para 14.4 for the conditions of a ‘dwelling’). Buildings to be used for a relevant residential purpose include homes for elderly people, and student and nursing accommodation. In the case of relevant residential purpose work, the builder must be given a certificate by the property owner (see VAT Notice 708 para 18.1).

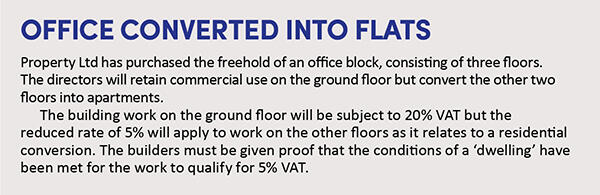

Residential conversions are very common in our big cities; for example, the Northern Quarter in Manchester has many apartments that used to be factories and warehouses. Barn and office conversions are also popular (see Office converted into flats).

Situation 2: Change in number of residential units

Imagine that you have purchased a detached house, and intend to convert it into two semi-detached houses and hopefully sell them for a profit. The sale of the houses will be exempt from VAT, which means there is no scope to reclaim input tax, even if you are VAT registered. However, the work carried out by builders will again be subject to 5% VAT because the project is producing a change in the number of dwellings; i.e. from one to two.

My emphasis of the word ‘change’ is deliberate. The 5% rate also applies if the number of residential units is reduced with a project; e.g. two semi-detached houses are converted into one detached house. This is perhaps surprising because the purpose of the 5% rate has always been to increase the number of habitable dwellings on our shores. But it is the change in number that attracts the lower rate of VAT (see VAT Notice 708 para 7.3).

Apartments are considered on floor-by-floor basis

If a project involves building work being carried out on a block of apartments, the number of units is always considered on a floor-by-floor basis. So, if a block consists of 12 apartments before a project starts – four on each of three different floors – and ends with the same number but two on the ground floor, six on the first floor and four on the second floor, the building work will be subject to 5% VAT in relation to work on the ground and first floors. However, work on the second floor will be standard rated because the number of units is unchanged (see VAT Notice 708 para 7.3.1).

Situation 3: Residential property not lived in for at least two years

The third situation when building work will qualify for 5% VAT is when a residential property has been empty for at least two years; i.e. not lived in during that period of time. However, there is an extra hurdle: the builder(s) carrying out the work will need proof of the empty period, such as council tax information, electoral register data, housing office records, and so on. The evidence must be from a third-party source. It would not be acceptable for the property owner to sign a statement stating the property has not been lived in for at least two years, or ask his accountant or solicitor to write a letter on his behalf.

As an amusing aside, HMRC helpfully confirms in its guidance that illegal occupation of a property by squatters is ignored for the purpose of the two-year window. Was this ever in doubt? Hopefully not (see VAT Notice 708 para 8.3.3).

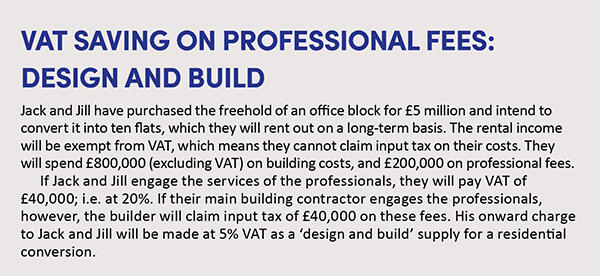

VAT saving on professional fees

Professional fees are always subject to 20% VAT; e.g. the services of architects, surveyors and project managers. A potential VAT planning solution is for the professionals to provide their services directly to the builder in cases where a 5% project applies to building work; and then the builder’s contract to the property owner is for a ‘design and build’ service, which attracts a 5% VAT rate on the entire fee, including materials and professional fees (see HMRC VAT Manual VCONST02720). See VAT saving on professional fees: design and build.

Image

Dispelling four common myths

Builders often know some basic rules about VAT but struggle with the finer points of the legislation, similar to a teenager on holiday in Paris trying to get by with a bit of half-remembered GCSE French. Here are four important facts that are often misunderstood:

1. VAT certificates are not needed for dwellings

If a builder is working for a property owner and the building will be used for either a ‘relevant charitable purpose’ or a ‘relevant residential purpose’, the owner must issue a certificate to the contractor confirming the intended use of the building to support any 0% or 5% rates of VAT. But certificates are not necessary for any work carried out on dwellings (see VAT Notice 708 para 17.1).

2. Reduced VAT rate also applies to subcontractors

With work carried out on dwellings, if the project qualifies for the reduced rate of VAT, the same rate is charged by all builders carrying out work; i.e. subcontractors working for other builders, as well as the main contractor working for the owner.

3. Reverse charge applies to 5% work

If a builder invoices another builder, and the builder receiving the invoice is both registered for VAT and CIS, the reverse charge has applied to these invoices since 1 March 2021. In other words, the first builder does not charge VAT on his sales invoices, and his customer accounts for the VAT in Box 1 instead, also claiming input tax in Box 4. The reverse charge applies to construction services subject to 5% and 20% VAT but – quite logically – not zero-rated services.

4. Correct VAT rate must always be charged

One of my favourite tales is about a builder who insisted on charging a property owner 20% VAT on a job that qualified for the 5% rate, on the basis that he used the flat rate scheme and would be out of pocket if he only collected 5% VAT. He argued that this should not be an issue for the owner because input tax could be claimed for the project in question.

The builder is partly correct: the 5% rate is not a good deal if he uses the flat rate scheme but that is irrelevant. The correct VAT rate must always be charged and customers can only claim input tax based on the correct rate of VAT that applies for the supply in question.