The Sequel!

Share this article

Matt Stringer considers the implications of the revised Diverted Profits Tax provisions

Key Points

What is the issue?

Multinational groups that concluded they had no Diverted Profits Tax liability under the original provisions (‘DPT1’) may now find that they have a material liability under the revised provisions (‘DPT2’).

What does it mean to me?

Any group that may have been within the scope of DPT1 that concluded they should not have a charge should revisit this position in light of DPT2. Particular impact should be expected for those with cross-border royalty payments and a low tax IP owner.

What can I take away?

The background and logic behind DPT2, a summary of how the law is intended to operate, (and a burning desire to watch a lot of movie sequels).

Aliens. The Godfather: Part II. The Empire Strikes Back. Sequels that unexpectedly change the landscape, far exceeding the impact of their predecessor.

It’s time to add DPT2 to that iconic list!

DPT1: A reminder

Finance Act 2015 introduced DPT1 to take effect for profits arising from April 1 2015. DPT was a new tax – wholly separate from corporation tax – charged at 25% on profits that are considered to be artificially diverted from the UK. Its introduction was consistent with the wider OECD project regarding Base Erosion and Profit Shifting (‘BEPS’) and a response to the calls for the taxation of large multinationals to be revisited.

DPT1 applied in two scenarios: where there was a transaction lacking economic substance, or where there was avoidance of a UK permanent establishment (‘PE’). The actual legislation is not easy to follow and is complex. At a basic level for either scenario to apply there must be an arrangement or series of arrangements where income is ultimately taxed at a low (or nil) rate (or in an avoided PE scenario, a main purpose of reducing or avoiding a UK corporation tax charge). There are de minimis provisions such that only large multinationals are within the scope of the rules.

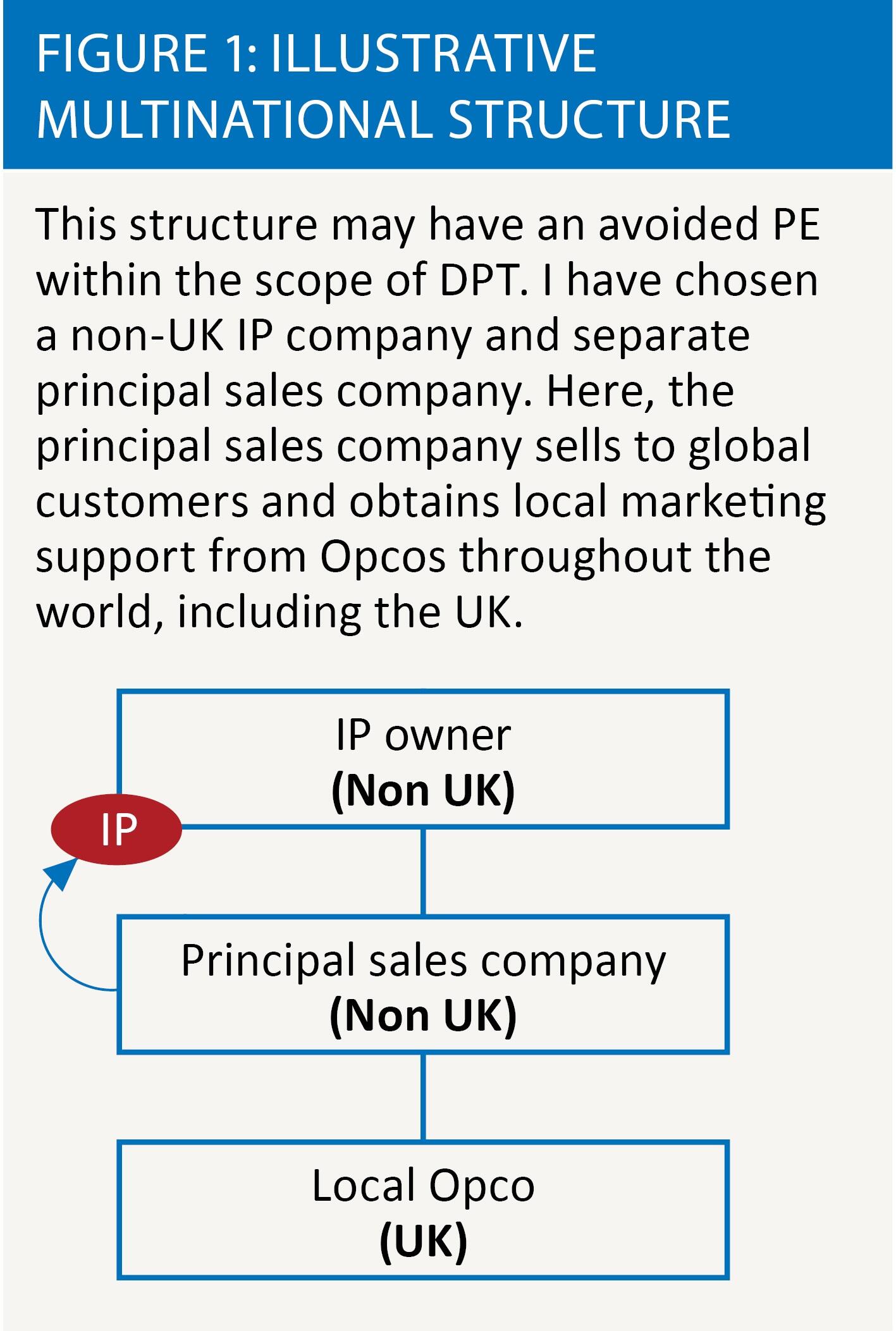

The avoidance of a UK PE scenario was particularly relevant for multinationals with a principal sales company outside of the UK. In this common business operating model, a principal sales company sells to customers across a number of jurisdictions and seeks local support (e.g. marketing) from a group company in the customer location. Subject to some other conditions, the principal sales company may then have an ‘avoided PE’, and be within the scope of DPT1. See figure 1.

A foreign company with an avoided PE is then required to consider whether it has a liability to DPT. In doing so, it should consider the alternative provision that it would have made, had any taxes on income not been a consideration. Broadly, where this would have resulted in the same type and amount of expenses of the foreign company, then the only profits subject to DPT are the ‘taxable diverted profits’ of the avoided PE. The law prescribes how taxable diverted profits should be calculated. Where the UK company is already fully rewarded for its activities, the taxable diverted profits may well be zero, i.e. a foreign company may well have an avoided PE, but with the amount attributed to that avoided PE being zero.

Scope/challenge of DPT1

You can see from the example above that ultimately, DPT1’s remit may not include bringing profits of low/zero tax jurisdictions within the scope of UK tax. In the example shown in figure 1, it is possible that:

a. the alternative provision that would have been entered into where tax was not a factor would still result in the same expenses of the principal sales company, given it requires access to the group IP to conduct its business. (It may for example have needed to pay an IP owner in a different jurisdiction in that theoretical scenario); and

b. the group have conducted a full transfer pricing study and concluded (and agreed with HMRC) that the UK marketing support services company receives adequate remuneration for its activities

The principal sales company therefore may have an avoided PE within the scope of DPT1, but could have no taxable diverted profits. So the new UK tax aimed at bringing artificially diverted profits within the UK tax net may not have resulted in an increased UK tax liability for groups with low/no tax IP owners. By introducing a new tax on profits, only those profits that could somehow be attributed to UK activities could be subject to tax. So whilst DPT1 did change the tax landscape, once the UK received its ‘fair share’ of global profits (based on appropriate transfer pricing) the ability to reach low/no tax profits from other jurisdictions disappeared.

DPT2: The sequel

The government announced on 16 March 2016 that it intended to introduce legislation in Finance Bill 2016 to reform the rules governing the deduction of income tax at source from payments of royalties. A technical note with some detail regarding the changes was published stating that certain changes would take effect from Royal Assent of the bill. On the evening of 27 June 2016 this note was updated, draft legislation published and certain changes (including DPT2) were to take effect from the very next day: 28 June 2016.

DPT2 tackles the issue discussed above regarding the UK’s remit to tax foreign profits. It does so by using a withholding tax mechanism to calculate an amount of diverted profit. This is explored below.

One can only speculate to the rationale and timing for a DPT sequel. The BEPS changes, though far reaching, have a longer timeframe to implement and this, against a backdrop on ongoing public scrutiny, may have prompted the change.

The mechanism of DPT2

A number of changes to UK royalty withholding tax were introduced in Finance Act 2016. One of these changes concerns when royalty payments are deemed to have a UK source.

For royalty payments made by a foreign company on or after 28 June 2016, where the royalty is connected with a trade carried on through a UK PE, the royalty may be deemed to have a UK source. This is regardless of whether the royalty amount would be deductible in calculating the profits of the UK PE. A foreign company with a UK PE paying a royalty to a group company must calculate the ‘just and reasonable’ portion of that royalty that should be sourced to the UK PE vs sourced to the foreign HQ. The portion which has a UK source is then prima facie subject to the basic rate of UK income tax via a withholding mechanism.

The same approach for UK PEs is then taken and applied to avoided PEs for DPT purposes. A foreign company with an avoided PE (even if it previously had no taxable diverted profits) that pays a royalty to a group company must now calculate the ‘just and reasonable’ proportion of the royalty that should be taken to have a UK source. The proportion of the royalty that would then be subject to UK withholding tax in an actual PE scenario is then subject to DPT.

Usual treaty principles may apply in both cases (where the treaty between the UK and the recipient of the royalty may act to reduce or eliminate the royalty withholding tax due/reduce the DPT charge on a proportionate basis). This is of course only of benefit where the UK has a treaty with the jurisdiction of the royalty recipient providing for a reduced rate.

Coming back to figure 1, the scope of DPT2 becomes clear – demonstrated by our illustrative group structure. While the UK may already be taxing an appropriate share of global profits (as determined by accepted transfer pricing principles), the royalty paid by the principal sales company requires consideration. Where the principal sales company has an avoided PE in the UK, we must now determine the ‘just and reasonable’ proportion of the royalty paid to the IP owner that should be sourced to the UK. The ‘just and reasonable’ outcome may depend on a number of factors and requires careful thought. This being said, where there is no treaty between the UK and the IP owning jurisdiction that could reduce royalty withholding tax, a proportion of the royalty must be allocated to the UK and then subject to DPT at 25%.

By altering the way in which a royalty may have a UK source, and extending these provisions to avoided PEs for DPT purposes, the UK has created a mechanism to levy a tax on profits in low/no tax jurisdictions (over and above an arm’s length UK profit).

Like Toy Story 2, DPT2 may not have received as much press as DPT1, but it will certainly go down in history as having the greater impact for those multinationals that feel its effect.

Looking to the future

After DPT1, some commentators thought that its introduction and the concept of an avoided PE was temporary – a sticking plaster – and that following further international tax reform under the BEPS programme, including the recommended introduction of a lower PE threshold, the need for DPT would vanish.

However, this now seems unlikely to be the case. The UK has so far rejected a lower PE threshold – assumingly as the existence of the avoided PE concept currently tackles any base erosion in that space. With DPT (especially DPT2), here to stay, we may see multinationals taking increased steps toward aligning profits with substance.

So DPT2 may be our concluding chapter. However, for many sequels, the second movie is not the end of the story. Corporate tax reform in the US may require tax authorities around the globe to re-think many domestic law concepts, and in the UK we have our own changing external environment – how will Brexit alter the landscape? Can we expect (dramatic pause) the concluding chapter in (another dramatic pause) a DPT trilogy? If so, let’s hope it’s more Return of the Jedi and less Alien 3.