Subsidy, or not subsidy?

Share this article

Matt Stringer explores the design of the FCPE and the EC’s investigation into the regime

Key Points

What is the issue?

The EC have presented initial arguments that the UK’s Finance Company Partial Exemption regime (‘FCPE’) may represent unlawful state aid. An in-depth probe by the EC now begins.

What does it mean to me?

Should the EC conclude that the regime does represent state aid, the UK Government would be instructed to collect significant amounts of additional taxes from Groups which made use of the regime. Groups utilising the FCPE should consider their position.

What can I take away?

Some insight into the design of the UK CFC rules, the Finance Company Partial Exemption, and an overview of what to expect from the EC’s investigation.

On 26 October 2017, the European Commission (‘EC’) gave notice to the UK Government of a decision to investigate certain elements of the UK Controlled Foreign Company (‘CFC’) regime on the basis that they may represent unlawful state aid. An official publication was released on 24 November 2017. A successful challenge by the EC could give rise to significant costs for many multinationals.

Introduction to the UK CFC regime

The UK’s CFC rules were introduced in 1984 to prevent the diversion of UK profits to overseas subsidiaries by multinationals. The concept of the UK CFC rules has always been that certain profits of subsidiaries located overseas may be subject to a UK tax on a current basis, where certain conditions are met.

After a substantial consultation process, the rules were reformed as part of Finance Act 2012, to be effective 1 January, 2013. The 2013 reforms were, to some large extent, in response to a challenge in the European Courts that the old rules were inconsistent with the EU Freedom of Establishment principle. (More on this to come in a future article!)

An overriding aim of the 2013 reforms was that the UK CFC rules should minimise the compliance burden for both business and HMRC. The rules were designed to prevent artificial diversion of profits from the UK to jurisdictions where they would be subject to a lower level of tax. They should not interfere, as far as possible, with multinationals’ commercial decisions in how to arrange their overseas operations.

Operation of the CFC rules

The regime operates by applying certain ‘gateways’ to different types of profits to identify any that have been diverted from the UK (Chapter 3), which will then be charged to tax at the level of a UK parent (the ‘water’s edge’ company). After passing ‘through’ a gateway, the two most common chapters for UK companies with overseas subsidiaries to consider are Chapter 4: Business Income and Chapter 5: Non-Trading Finance Income. Chapters 6, 7 and 8 of the rules contain rules for other kinds of profit which are not explored here.

Chapter 4’s main test looks to identify profits that are attributable to UK activities by considering Significant People Functions and Key Entrepreneurial Risk Taking Functions (‘SPF’s and ‘KERT’s) of the business; who undertakes these functions; and where they take place. Chapter 4 requires a majority of these functions to be performed in the UK before an apportionment arises.

Chapter 5 contains much more stringent rules for identifying profits which could be subject to a CFC apportionment. Any UK based SPF/KERT functions in relation to the profits is enough to trigger an apportionment (as opposed to the need for a majority in a Chapter 4 context). Further, any capital contributed from the UK to the overseas subsidiary which then generates the non-trading finance profits is a sufficient connection for an apportionment to arise.

This means that certain non-trading finance profits of a UK CFC would not be subject to current tax in the UK at all – those profits which cannot be traced to a capital contribution from the UK, and where there is no (or very little) functionality in the UK in relation to generating those profits. These profits are simply not within the scope of Chapter 5.

The rules also contain wide reaching Entity Level Exemptions (Chapters 10 through 14) which, where the relevant conditions of the exemption are met, act to completely exclude that entity from the CFC regime – regardless of the nature of its profits. Broadly, these exemptions provide a simple way of concluding that a CFC should not be subject to an apportionment where the CFC is, for example: subject to a reasonable level of tax, immaterial in terms of its profits or profit margin, or resident in a location where the UK has deemed the risk of artificial profit diversion to be low.

The Finance Company Partial Exemption (‘FCPE’)

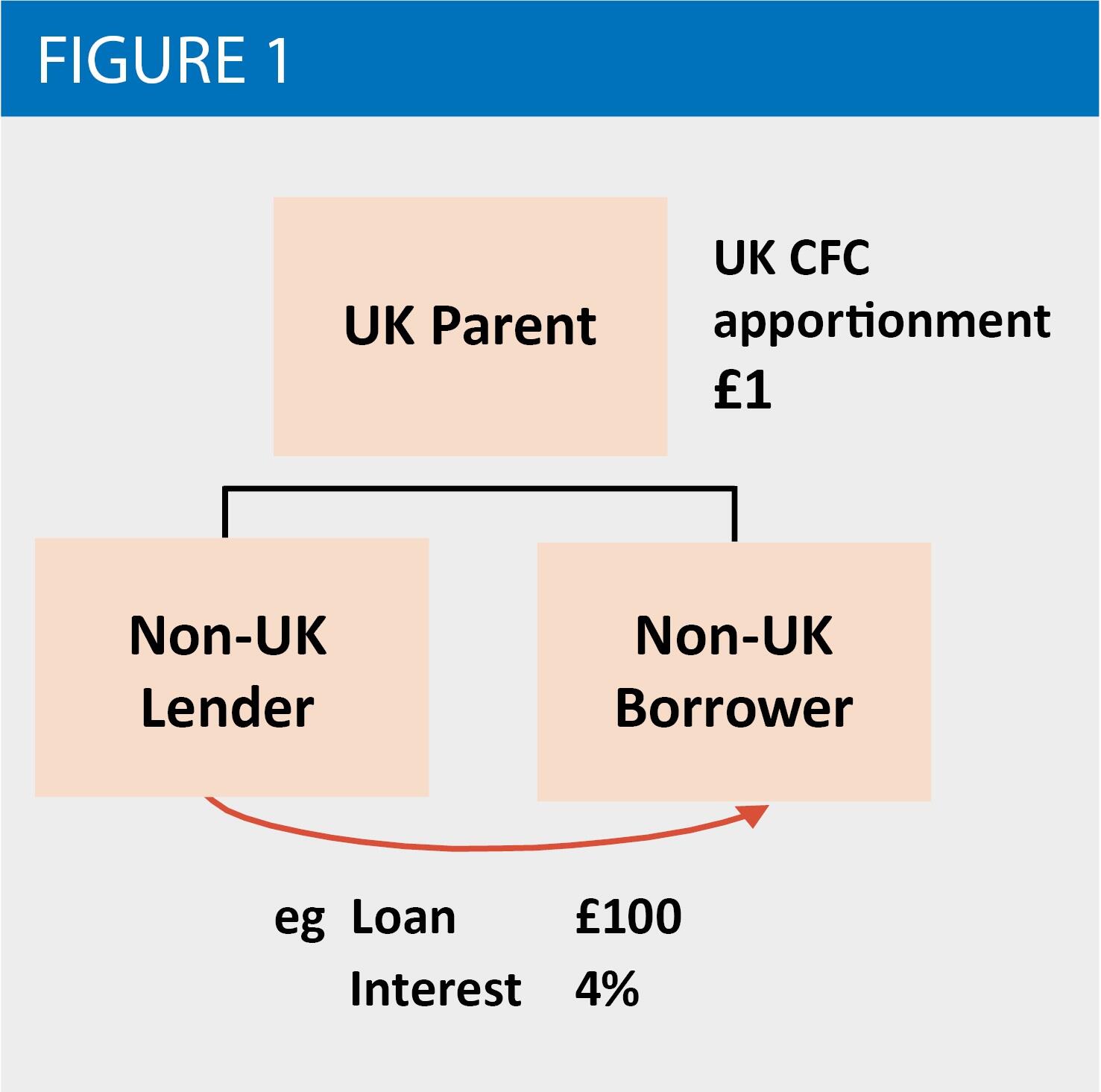

Chapter 9 of the rules contains the FCPE. The FCPE is a 75% exemption from an apportionment where (i) there are profits which constitute qualifying loan relationship profits (‘QLRP’) and (ii) a business premises condition is met.

For the profits to be QLRP, the relevant loan must:

- Be a loan relationship as defined in CTA 2009

- Have an ultimate debtor which is connected to the CFC and controlled by the same UK company which controls the CFC

- Not be excluded from being qualifying, by virtue of a number of tests (broadly focussed on ensuring that the loan does not give rise to a UK tax deduction)

Where these conditions are met, there is no need for any tracing of the SPF/KERT functions associated with the financing profits. Instead, 25% of the finance profits are apportioned to the UK and subject to tax on a current basis.

This approach is of course different from the detailed analysis of people, functions and risks that we see in a Chapter 4 context. The joint approach of Chapters 5 and 9 enables a UK company to establish the appropriate level of apportionment in respect of a CFC’s financing activity, via a mechanical calculation and satisfaction of certain basic conditions. See Figure 1.

The FCPE’s introduction recognised that it is much more difficult to undertake an analysis of people, functions and risks relating to financing activity than it is for other types of business activity, and to do so would be a highly subjective task. Activity relating to generation of financing profits is often mobile and changeable, and limited in its scope.

A further, more complex exemption exists which can act to exempt more than 75% of non-trading finance profits. Whether this ‘full’ exemption may be availed depends on the origin of the funds lent or the net interest expense of the Group at UK level.

Next steps in the State Aid investigation

An overview of the next steps in the process are provided below:

The EC presented their ‘opening decision’ on 26 October 2017 and it was published on 24 November 2017. This decision outlines the EC’s preliminary analysis as to why they have concerns that FCPE may represent unlawful state aid.

The UK Government had one month from the opening decision to submit their response, i.e. by 26 November 2017. Other interest parties also had one month to respond to the decision – meaning the EC are likely to receive other responses by 24 December 2017.

Any third party responses will be forwarded to the UK Government, who may also offer their comments on the responses.

The EC must then progress the investigation which will involve further meetings and letters between the UK Government and the EC.

When ready, the EC will issue a final decision as a ‘non-aid decision’ or a ‘negative decision’. A negative decision would include an order for the UK to recover the aid. In this instance, this would mean HM Treasury are directed to recover the additional tax from Groups who have utilised the FCPE. It is possible that the EC could issue a final decision before the end of 2018.

A negative decision could be appealed before the General Court, which is likely to take a couple of years. Both the UK Government and the affected taxpayers could appeal the decision to the General Court. A further appeal to the ECJ of the General Court’s judgement could then be made on any point of law. This means that it may be several years before the matter is finally resolved.

In a future article I will explore the EC’s initial arguments as to why the FCPE represents unlawful state aid, as well as the arguments that HM Treasury and others may be looking to make as to why it is not. We will then move on to consider the implications of a negative decision, including the impact of a world where Chapter 5 of the UK rules exists without Chapter 9.