Set your alarms

Share this article

Dawn Register and Helen Adams consider the actions needed as a result of the forthcoming Requirement to Correct

Key Points

What is the issue?

The Finance Bill will include a requirement to correct any failures or errors resulting in undeclared UK tax related to offshore matters or offshore transfers.

What does it mean to me?

The UK tax affairs of clients with offshore issues should be reviewed to establish whether any corrections or a ‘protective’ disclosure may be needed before 30 September 2018, taking into account any applicable extended assessment time limits.

What can I take away?

Making a full, voluntary disclosure before the deadline will avoid high penalties and other sanctions.

HMRC has an ongoing agenda to tackle all forms of ‘non-compliance’. Legislation in the first Finance Bill of 2017 was designed to force full disclosure to HMRC of all offshore (i.e. non-UK) related matters or relevant ‘offshore transfers’ assessable to UK tax. Failure to ‘correct’ before the deadline will result in large penalties, even in circumstances where there was never any deliberate behaviour, and other sanctions.

This legislation, known as the Requirement to Correct (‘RTC’), was one of many measures put on hold ahead of the snap general election in June 2017. HMRC’s announcement on 13 July 2017 confirmed that the RTC will form part of the Finance Bill scheduled for publication shortly after the end of Parliament’s 2017 summer recess, probably with the correction deadline of 30 September 2018 unchanged.

The RTC deadline purposely coincides with the first full automatic exchange of financial information between all countries participating in the OECD led Common Reporting Standard (‘CRS’). Both the early and late adopters of the CRS should be fully operational by September 2018, resulting in more than 100 countries exchanging tax reporting data globally. It also follows the 31 August 2017 deadline for advisers to notify certain clients of the need to review their UK tax affairs (SI 2016/899).

Consequently, there is considerable urgency for taxpayers to review the UK tax implications of their non-UK assets and general offshore activities to establish whether corrections are needed.

What is the ‘Requirement to Correct’?

The RTC requires the correction of any UK Income Tax, Capital Gains Tax or Inheritance Tax relating to ‘offshore’ tax non-compliance by the RTC deadline, which is expected to be 30 September 2018. It affects all liabilities which are not fully corrected by 5 April 2017 regardless of the type of behaviour causing the issue and whether it arose from a failure to notify, failure to submit returns or errors in previously submitted tax returns.

The ‘offshore’ aspect encompasses ‘offshore matters’ and ‘offshore transfers’. An offshore matter is one where tax is charged on or by reference to:

- Income arising outside the UK

- Assets located outside the UK

- Activities carried on wholly or mainly outside the UK

- Anything having effect as if it was one of the above.

An offshore transfer broadly is something which is not an offshore matter and, instead, all or part of the income and gains on which the tax is charged was received in a territory outside the UK or transferred to a territory outside the UK on or before 5 April 2017. There is a separate, similar IHT test.

The taxes covered demonstrate that these measures are primarily aimed at individuals, trusts and estates tax liabilities. The RTC is essentially a requirement to submit a full disclosure to HMRC quantifying the undeclared tax. There is no statutory obligation to agree the position or pay the tax, interest and penalties before the deadline.

What happens if the correction deadline is missed?

HMRC will use information at its disposal, including CRS data, to identify cases for investigation using its CONNECT computer system. These investigations will either be civil (e.g. via HMRC’s Code of Practice 9) or criminal investigations with a view to prosecution. HMRC’s 2016/17 Annual Report and Accounts reiterated HMRC’s aim to increase prosecutions of ‘wealthy individuals and corporates’ to 100 per annum by the end of this Parliament. This will probably represent a significant increase in the number of prosecutions as the NAO’s report in October 2016 noted that one high net worth person was successfully prosecuted since 2009 although ten others were under criminal investigation in October 2016. Advisers should also be mindful that they could risk being labelled an ‘enabler’ of offshore tax non-compliance by HMRC (FA 2016, Sch 20).

To give HMRC more time to process the information due under the CRS, assessment time limits which would normally expire during the period from 6 April 2017 to 4 April 2021 inclusive will be extended to finish on 5 April 2021. Otherwise standard statutory assessment time limits apply. HMRC’s investigations could result in discovery assessments being issued to bring undeclared tax into charge where enquiries are not already open for affected tax years. Late payment interest will also be imposed.

Where someone fails to fully correct all irregularities by the RTC deadline HMRC will charge ‘Failure to Correct’ (‘FTC’) penalties instead of existing penalties (e.g. FA 2007, Sch 24 or FA 2008, Sch 41 penalties). Having a ‘reasonable excuse’ will be the only defence against FTC penalties. A ‘reasonable excuse’ is expected to exclude:

- Reliance on professional advice which is deemed ‘disqualified’;

- Situations where the excuse ceases and the issue was not remedied without undue delay;

- Insufficiency of funds attributable to events within the taxpayer’s control;

- Failures by another person, unless the taxpayer took reasonable care to avoid them.

- The draft legislation suggested that advice will be disqualified if it:

- was given to the taxpayer by an ‘interested person’ or as a result of arrangements between an interested person and the person who gave the advice:

- was addressed to or given to a person other than the taxpayer;

- was given by an independent person without appropriate expertise; or

- failed to take into account the taxpayer’s specific circumstances

unless, the taxpayer checked whether the advice was disqualified before the RTC deadline and reasonably believed that it was not.

An ‘interested person’ includes someone who facilitated the taxpayer participating in the ‘relevant avoidance arrangements’. These were broadly defined as arrangements whose main purpose or one of its main purposes could be reasonably concluded to be the obtaining of a tax advantage (which includes a reduction or deferral of a tax liability). Arrangements include any ‘agreement, understanding, scheme, transaction or series of transactions’. This broad drafting may therefore, for example, disqualify advice on an offshore trust structure for a non-UK domiciled individual as well as on an avoidance scheme.

FTC penalties are expected to comprise:

- a 200% financial penalty of the final amount of undisclosed, assessable tax which may be mitigated to no lower than 100% unless special circumstances exist;

- a further 50% uplift, as an offshore asset moves penalty, to the 100% to 200% financial penalty in the event of any attempt to move assets to another jurisdiction, after the Finance Bill gets Royal Assent and before the correction deadline, to escape FTC penalties despite the taxpayer knowing that they should correct their UK tax position. The effective penalty band in those circumstances is 150% to 300% of the final amount of undisclosed tax;

- an additional financial penalty of 10% of the value of the offshore assets in cases where the undisclosed tax exceeds £25,000 for any tax year.

The level of penalties set out above essentially converts even innocent and careless errors to deliberate ones when you compare current penalties to FTC penalty levels. FTC penalties cannot be suspended either.

In addition HMRC is expected to publish the details of any taxpayer who fails to correct their tax position despite knowing at any time in the RTC period that they had non-compliance to correct. This applies where:

- the tax at stake on which FTC penalties are levied exceeds £25,000; or

- at least five FTC penalties are charged.

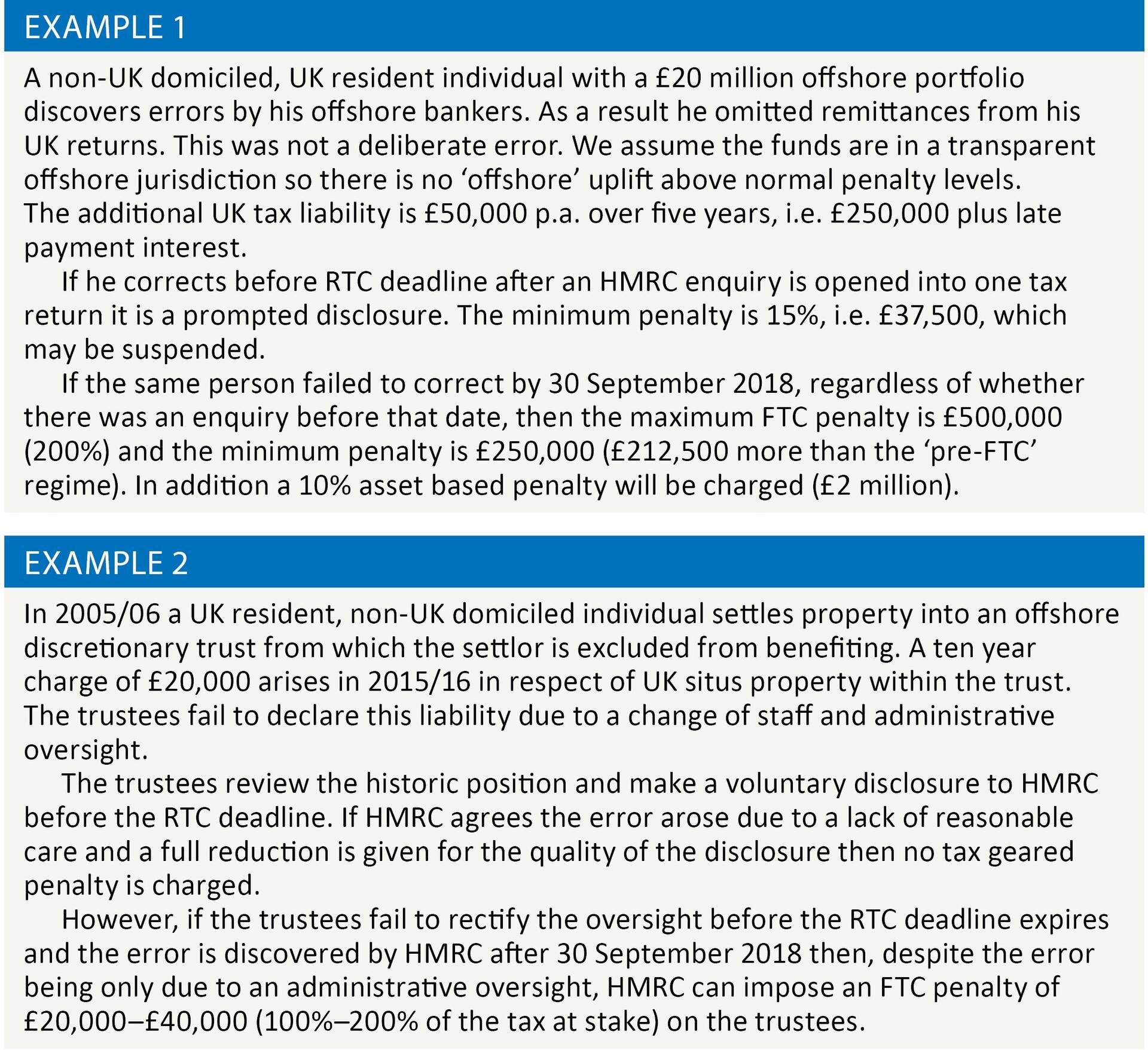

Examples of the RTC’s and FTC’s effects

A RTC may arise from a range of situations from a failure to notify or submit returns and errors in returns through to falling foul of the more complex and esoteric anti-avoidance provisions designed to capture non-UK ‘offshore’ structures. See examples 1 and 2.

The examples show that the potential for inadvertent errors with regard to non-UK interests and non-UK activities is very wide. Other examples could include deliberate omission of income and gains arising from offshore investments or a person submitting returns assuming they were non-UK resident or domiciled without getting advice to check whether they met the conditions for this status. The RTC places a heavy burden of responsibility on any parties with overseas interests connected to the UK in any way to review their arrangements carefully to ensure they are fully tax compliant.

The correction process

The RTC deadline will approach quickly so it is vital that all overseas interests are reviewed as a matter of urgency to establish whether ‘correction’ is necessary. Reviews should consider whether offshore aspects are technically correct and also whether implementation (e.g. remittances, constructive or direct) is free from failure. In addition, reviews should consider why any errors or failures arose in order to identify how many years of tax liabilities need to be quantified due to extended assessment time limits and the level of any penalties. Any hassle and additional cost now must be weighed against the need to protect from the steps and sanctions that HMRC may use in future.

Corrections are made by giving HMRC the information which would have been included in a correct tax return and which would enable or assist HMRC to calculate the tax due. In practice this will be achieved via a voluntary disclosure through HMRC’s Worldwide Disclosure Facility (a disclosure process rather than an amnesty) or by alternative means e.g. amendment or submission of tax returns within existing statutory deadlines or via Code of Practice 8 or 9 disclosures. Specialist advice should be sought as appropriate, especially where there is any risk of HMRC suspecting deliberate behaviour as it may opt for a criminal investigation.

It is essential to review ongoing enquiries to establish whether a full factual disclosure has been made to HMRC of all matters for all years (not just those under enquiry). If not, then a disclosure must be submitted before 30 September 2018 in order that HMRC does not impose FTC sanctions.

In offshore cases there are often areas of risk; grey areas where HMRC may seek to assess further tax but where advisors think that technical arguments exist as to why no UK tax is payable. These may encompass issues such as residence, domicile and anti-avoidance rules re: offshore structures. In such circumstances careful thought must be given to whether a full voluntary ‘nil tax’ disclosure of all the facts should be made to HMRC. Without such a full disclosure, the risk of FTC sanctions will remain.

In summary

The RTC’s potential to capture the full range of oversights is huge – from a simple failure to understand reporting requirements through to blatant tax evasion. Even with no deliberate intent, ‘Failure to Correct’ penalties of up to 300% of the potential lost tax revenue combined with 10% asset based penalties will apply where full disclosure is not submitted to HMRC by 30 September 2018. Taxpayer’s details could also be published publicly on the government’s website. This timescale may be altered but the need to take action is still highly pertinent.

The good news is that a complete and correct voluntary disclosure of UK tax issues before the RTC deadline will ensure that the FTC sanctions will not apply. The more favourable current statutory penalty regime will apply instead, where the potential penalty levels are generally lower and substantial reductions (even to nil penalties in some circumstances) apply for unprompted disclosures.

A review is therefore a necessity rather than a ‘nice to have’ and work should begin without delay.