Tackling tax evasion: how can HMRC do better?

Share this article

We consider what more HMRC could do to tackle tax evasion following recent parliamentary and NAO reports.

Key Points

What is the issue?

While HMRC’s estimates show the criminal attacks tax gap is reducing, the other tax evasion and hidden economy parts of the tax gap remained stubbornly high (estimated at £7.7 billion for 2022/23). HMRC is under pressure to set a strategy and tackle these parts effectively.

What does it mean for me?

Taxpayers suspected of evasion need to understand how HMRC uses its powers to sanction and penalise evaders and how to best navigate investigations and disclosure processes.

What can I take away?

HMRC should open more compliance checks into suspected tax evasion, but it remains essential for advisers to encourage voluntary disclosures where clients need to admit deliberate wrongdoing.

In February 2025, the House of Commons’ Public Accounts Committee (PAC) published its report on tax evasion in the retail sector (see tinyurl.com/3fcn8mju), highlighting ongoing challenges in HMRC’s efforts to combat non‑compliance. The National Audit Office (NAO) analysed the administrative cost of the tax system, offering recommendations for enhancing compliance yield (see tinyurl.com/

269pds7f). These publications emerge at a critical juncture as, in the 2024 Budget, the Chancellor emphasised the importance of closing the tax gap to the government’s fiscal strategy.

In HMRC parlance, tax evasion is equivalent to deliberate wrongdoing. Deliberate behaviour includes intentionally making a statement which, at that time, the person knew was inaccurate; i.e. they intended to mislead HMRC (see the cases of HMRC v Tooth [2021] UKSC 17 at [42] – [47] and C F Booth Ltd v HMRC [2022] UKUT 217 (TCC)). Deliberate behaviour also occurs where a taxpayer suspects that a document contains a mistake ‘but deliberately and without good reason chooses not to confirm the true position before submitting’ it to HMRC (see CPR Commercials Ltd v HMRC [2023] UKUT 61 (TCC)).

Understanding tax evasion statistics

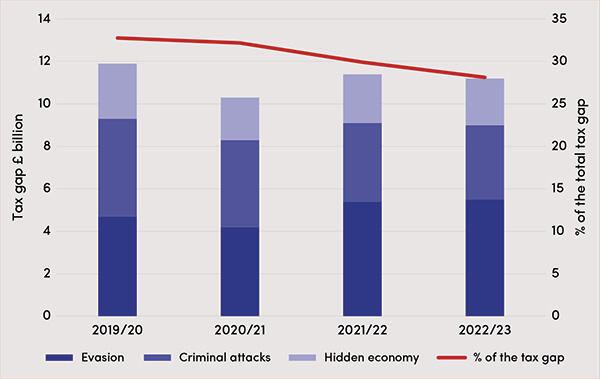

As the graph shows, the ‘tax evasion gap’, which we calculated by combining HMRC’s figures for evasion and the hidden economy, stayed stubbornly high over the last four years. In contrast, the amount HMRC estimates is lost to ‘criminal attacks’ reduced from £4.6 billion in 2019/20 to £3.5 billion in 2022/23. Criminal attacks are tackled separately by its Fraud Investigation Service (FIS) and, whilst they are also within the legal definition of evasion, they are not the focus of this article.

However, these statistics require careful interpretation. HMRC’s research reveals that rather than being entirely caused by deliberate behaviour, some hidden economy non-compliance may arise from a lack of awareness, misunderstanding of obligations or perception of low risk of detection – particularly among smaller businesses and self-employed individuals (see our Tax Adviser article ‘The hidden economy: behavioural challenges in September 2023). Furthermore, the current statistics have notable limitations:

1. Behavioural segmentation gaps: The tax gap attributable to evasive behaviours is not broken down by taxpayer types or industry sectors, making devising and evaluating targeted interventions challenging. However, the PAC report said that 81% of tax lost to evasion in 2022/23 arose from small businesses.

2. Yield attribution: While HMRC reports compliance yield figures for different operational areas, these are not categorised by behaviour type. It remains unclear what proportion of yield stems from tackling deliberate non-compliance. Similarly, no statistics are published on penalties levied (such as a split of the number and value of Finance Act 2007 Sch 24 error penalties between deliberate and careless behaviour). Without knowing yield and penalties, how does HMRC know whether its interventions are effective in tackling the tax evasion gap?

3. Intervention effectiveness: Limited data exists on the comparative effectiveness of different compliance approaches. For instance, we lack comprehensive information on actual vs expected yield generated from nudge letter campaigns compared to enquiries or investigations.

4. Detection limitations: By its very nature, evasion involves non-disclosure, often through cash transactions or offshore arrangements. It sometimes involves concealment, for example using false invoices. This makes reliable estimation and detection inherently difficult despite the large volume of data held by HMRC. HMRC may be assisted by the NAO’s new guidance on helping public bodies improve fraud and error estimation.

HMRC’s compliance activities provide additional context (see

tinyurl.com/y4wpbmmj). In 2023/24, HMRC only started 268 (417 in 2022/23) tax fraud investigations under the Contractual Disclosure Facility (COP9), some of which probably opened because of voluntary disclosures requesting COP9 via CDF1 forms. Overall numbers of open COP9s fell as HMRC closed more cases than it opened; 2,077 cases were ongoing at 31 March 2024. Criminal investigations resulted in 501 charging decisions, with 302 successful prosecutions.

However, COP9 yield figures cannot be compared to the tax gap to judge the effectiveness of HMRC’s work in tackling evasion, as these cases relate to multiple tax periods whereas the tax gap is an estimate for one year. While these figures demonstrate HMRC’s commitment to pursuing serious cases of tax fraud, they only represent a proportion of overall activity to tackle tax evasion as that work is also undertaken elsewhere in HMRC.

HMRC’s current approaches to tackling evasion

HMRC employs multiple strategies to address the tax evasion gap, combining data analysis, compliance checks and preventative work. Some frauds are prevented by its systems. It analyses multiple disparate data sources (including third-party and offshore data) to identify potential cases for investigation, applying a risk-based approach to decide whether to open compliance checks.

Depending on the nature of the risk, suspected tax at risk and its policy (see tinyurl.com/594393v3), HMRC can open criminal investigations with a view to prosecution. Other suspected serious frauds are dealt with under COP9 or using general compliance check processes involving information notices, discovery assessments and substantial tax-geared penalties. It also launches targeted campaigns for specific sectors showing high non-compliance; e.g. the Electronic Sales Suppression disclosure process (see tinyurl.com/3wakb74n) and nudge letters on online marketplace sales (see tinyurl.com/2ueuv32p).

However, deterring evasion and encouraging compliance should be more cost-effective than investigations. In addition to general education via YouTube, social media and gov.uk, HMRC issues proactive educational nudge letters. It adopts processes to restrict businesses’ ability to trade without filing returns; e.g. hidden economy conditionality (Finance Act 2021 Sch 33 and Finance (No2) Act 2023 s 342).

It hopes that its powers to issue substantial tax-geared penalties (particularly for offshore non-compliance) and to publish deliberate defaulters’ details (Finance Act 2009 s 94) will deter too. Enablers of tax evaders may be deterred by corporate criminal offences for failure to prevent tax evasion, dishonest tax agents and enablers of offshore non-compliance, as well as the forthcoming informants reward scheme.

PAC and NAO recommendations

The PAC report noted that HMRC intends to increase the staff in FIS and the number of prosecutions. PAC recommended that HMRC improve its approach to tackling tax evasion by taking steps including:

- creating a strategy for tackling tax evasion and setting SMART objectives;

- working with Companies House and the Insolvency Service to develop a plan for working jointly to tackle frauds and phoenixism and measure the deterrent effect of their work, as subsequently confirmed by the Spring Statement; and

- undertaking further data analysis to check if the tax evasion gap is bigger than estimated.

The NAO report’s recommendations focused on cost-effectiveness. The most relevant to tackling non-compliance are:

- Compliance yield per case worker (productivity) should increase annually.

- HMRC should better evaluate its ‘upstream’ compliance activities (i.e. those trying to prevent non‑compliance) so it knows which are most effective at reducing the need for future compliance work.

- HMRC could consider the risk associated with different agents and how that may affect the level of compliance work.

Other opportunities for HMRC

While these reports provide valuable insights, we believe that additional measures could further enhance HMRC’s ability to address tax evasion.

Enhanced data collection and sharing

Recent and forthcoming initiatives present opportunities for improved compliance monitoring:

- The Digital Platform Reporting regime (effective from 2025) provides HMRC with additional data on income earned through digital platforms.

- Crypto-asset reporting requirements from 2027 may illuminate previously opaque transactions and ownership of cryptoassets.

- The proposed landlord database (Renters’ Rights Bill Part 2 Chapter 3) could significantly enhance the visibility of rental income, although the Bill’s text (particularly clause 87) does not clearly establish HMRC’s access rights.

However, these data sources will only help HMRC to tackle tax evasion if it allocates resources to analyse the data and investigate identified risks. The government expects that compliance checks will be better targeted in future due to investment in AI and advanced analytics.

Tax Administration Framework reforms

HMRC’s ongoing review of the Tax Administration Framework presents opportunities to build compliance considerations into system design. The outcome to HMRC’s ‘New ways to tackle non-compliance’ consultation confirmed that HMRC will be empowered to require taxpayers to correct mistakes, effectively making it impossible to ignore nudge letters. However, its current narrow scope does not encourage disclosure of other mistakes or the same mistake for other years. It may be better to enact a general ‘requirement to correct’ obliging taxpayers to tell HMRC about mistakes (for example, by registering to disclose) within (say) 90 days of becoming aware of them. Whilst not doing so is already a criminal offence, HMRC’s prosecution policy means that few taxpayers are prosecuted or feel at threat of prosecution – hardly an incentive to stop evading tax and put things right.

While tax advisers are required by Professional Conduct in Relation to Taxation (PCRT) to encourage clients to disclose fully and cease acting if a client refuses to disclose mistakes (as well as submitting Suspicious Activity Reports), a civil requirement to disclose may incentivise compliance if its implementation is effectively publicised by HMRC. HMRC’s research on improving communications may help it to encourage compliance more effectively and bust the myth that it will not catch up with tax evaders (see

tinyurl.com/3kavpf9z).

HMRC is consulting on strengthened behavioural penalties and tougher non-financial sanctions. HMRC’s research found that there was no evidence that publishing details of deliberate defaulters effectively deters tax evasion and that the public are generally unaware of it (see tinyurl.com/mrx764bs).

Instead, the experience of being investigated by HMRC and the subsequent financial penalties made the biggest impact on taxpayers. Of course, if taxpayers are unaware of potentially substantial tax-geared penalties when they start evading taxes, where is the deterrent?

A balanced approach might include the following:

- Make it simpler to make disclosures: HMRC really only needs two routes (COP9 and one other that covers all disclosures of non-deliberate behaviour).

- Put information on error penalty bands on notices to file returns and as on-screen prompts immediately before a taxpayer starts completing their tax return.

- Expand hidden economy conditionality activity (if it is effective at improving compliance), possibly extending it to other sectors (including those envisaged in HMRC’s 2024 consultation), coupled with requiring third parties such as letting agents or banks to notify clients (e.g. those opening bank accounts for a new business) to register to file tax returns.

- Tackle the expectation gap: raise public awareness of HMRC’s work and the data it holds so taxpayers perceive that there is a higher risk of being caught and appreciate the downsides of evasion. Equally, help taxpayers to understand the benefits of voluntarily rectifying mistakes and that proactively complying with their tax obligations can only help. To support this, HMRC should publish data on annual case numbers and yield to encompass all cases where deliberate behaviour penalties are imposed (not just COP9s).

- Open more compliance checks into suspected deliberate behaviour.

Supporting voluntary disclosures

Tax advisers play a vital role in promoting compliance. When clients want to disclose historic tax evasion, practitioners should refer to CIOT’s Guidance for Members (see tinyurl.com/5n98d222 ) and:

- Listen to the client, using open questions to establish what went wrong and why.

- Before registering for a voluntary COP9 via Form CDF1 or completing outline disclosure forms, check that the cause was ‘deliberate’ behaviour. McColgan v HMRC [2019] UKFTT 369 (TC) indicates that it can be difficult to later reclassify behaviour as merely careless without contemporaneous evidence.

- Help the client to understand the pros and cons of their different options for voluntary disclosures, seeking specialist advice if this is not your normal area of work. Don’t forget, only COP9 provides protection from prosecution in exchange for a complete disclosure.

- Remember professional obligations under the Money Laundering Regulations: a Suspicious Activity Report may be required.

- Warn clients about late payment interest continuing to accrue, ask them to identify funds to pay their liabilities, and advise on appropriate payments on account when amounts are known.

- Ensure that clients stop their deliberate behaviour immediately and starts fully complying with their UK tax obligations. If they decline to do so or to make a full disclosure then you may need to cease acting (see PCRT Helpsheet C at tinyurl.com/3d5wfnak).

- Explain the process so the client knows what to expect, including warning them about tax-geared penalties, that their details may be published and the managing serious defaulters regime (see tinyurl.com/3scme3nu). The Public Procurement Act 2023 came into effect on 24 February 2025 so government suppliers and connected persons may need legal advice as they can be excluded from public contracts based on ‘mandatory exclusion grounds’, such as being involved in tax evasion.

In conclusion

The recent PAC and NAO reports highlight progress and persistent challenges in tackling tax evasion. While HMRC tries to prevent non‑compliance and tackle tax evasion, it must do much more to raise awareness of its work to create an effective deterrent. Tax advisers should expect increased HMRC compliance activity too.

© Getty images