Shark infested-waters

Share this article

A lot of trading now takes place over the internet, with three parties involved in most deals, the buyer, seller and website owner. Neil Warren considers the potential VAT challenges

Key Points

What is the issue?

Any business must know its relevant sales figure as far as both output tax payments and the VAT registration threshold is concerned. This can be tricky to determine when there are three parties involved in a deal.

What does it mean to me?

There is a temptation for business owners to always look at a deal in a way that gives the best VAT outcome. This approach should be discouraged and decisions based on the actual facts of a transaction.

What can I take away?

It is important to think about VAT issues at the planning stage of any venture. It will then be possible to properly plan contracts and commercial terms that make it very clear which business is acting as the principal as far as a three party deal is concerned.

There’s an old saying that ‘two’s company and three’s a crowd’. In recent weeks, I have been asked on four separate occasions about VAT issues involving three parties – two of them were linked to website sales and whether the website host was acting as principal or agent in selling services. I will share one of these examples with you and also look at the wider issue of getting to grips with three party transactions as far as the nation’s favourite tax is concerned, helped by a First-tier Tribunal case about cleaning services.

Background

There are always two key questions to consider when working through a VAT challenge:

- What is the supply?

- What is the consideration? (i.e. payment – usually in money).

I always enjoy telling the story about a query I dealt with a number of years ago about a builder who agreed to build a new social club for an organisation, in return for ownership of a plot of land owned by the club on which he could build new houses. The land was worth a seven-figure sum and the building work was standard rated – so that’s a lot of output tax due to HMRC. In effect, the consideration for the builder services was the market value of the land – a reminder that ‘consideration’ in the world of VAT does not only relate to money.

But when it comes to dealing with three party transactions, two further questions become relevant:

- Contracts: according to contractual issues, which party is supplying or receiving services and to or from whom?

- Commercial reality: what is the perception of the customer as far as the deal is concerned? In other words, which party does the customer consider he is dealing with?

To give a simple example, I act for accountants in practice and give VAT advice as a self-employed consultant. This work often involves me speaking directly to the final client but the contractual reality is that my company has a letter of engagement with the accountant, and the accountant has his own letter of engagement with the final client. And the client is fully aware that I am a consultant used by the accountancy practice when they have a VAT problem. So there can be no confusion that I might be providing my services to the final client – I invoice the accountant and he invoices his client. My turnover for VAT purposes is the fee that I charge the accountant.

Hiring handbags

The first of the queries I dealt with related to a business that hosts a website that means people can hire handbags on a temporary basis. You can picture the scene: a lady is attending a posh wedding and would like to be spotted with a top of the range handbag on her arm but doesn’t want to pay £2,000 to own it outright. So she goes on a website and hires a handbag for three days at, say, £30 a day, paying for the service online (plus a refundable damage deposit no doubt) and enjoys the handbag for just the weekend of the wedding. You can find anything on the internet if you look hard enough!

So what are the VAT issues here? The answer is that the first time when VAT becomes relevant is when the website owner collecting the payments from customers discovers that her ‘gross receipts’ are getting close to the annual VAT registration threshold i.e. £85,000 since 1 April 2017. This assumes of course that she does not have other forms of taxable income under her chosen legal entity. The registration threshold is checked on a rolling 12-month basis and then VAT registration takes effect on the first day of the second month after it has been exceeded.

So you’ve guessed it, as the gross fee income of the website approaches the VAT threshold, an important question suddenly arises: as far as the threshold is concerned, is the relevant figure for the website owner the gross sales she collects from customers or just the net commission she receives on the deal? Let us introduce some figures: Mary charges £20 a day for hiring out her handbag; the website owner Jill charges £30 a day to final customers who take possession of the bag for the days in question. Are Jill’s taxable sales £10 a day (the mark-up she makes on the deal, which is effectively a commission charged to Mary) or £30 a day based on the gross payment received from the final customer? You can see how important this question is: If Jill’s taxable sales are limited to the commission she receives, she can effectively collect £255,000 of annual fees from the hirers before her 1/3 commission requires her to register for VAT.

Customer complaints

When I reviewed the website in question, it appeared to be very clear that the main deal was between the handbag owner and handbag hirer. There was a very important comment on the site that said: ‘If you are unable to resolve any complaint with the owner of the goods, then contact us and we will raise it on your behalf.’ This is a clear indication that the main supply excludes the website owner – she is acting as an agent and receiving a commission payment. Her role is as an intermediary and she only takes responsibility for any deficiency in the product that the customer suffers if the direct route between the other two parties fails to provide a solution. Another important point was that the hirer gave feedback about the quality of service she had received from the handbag owner, again indicating that the owner was providing the service directly to the hirer.

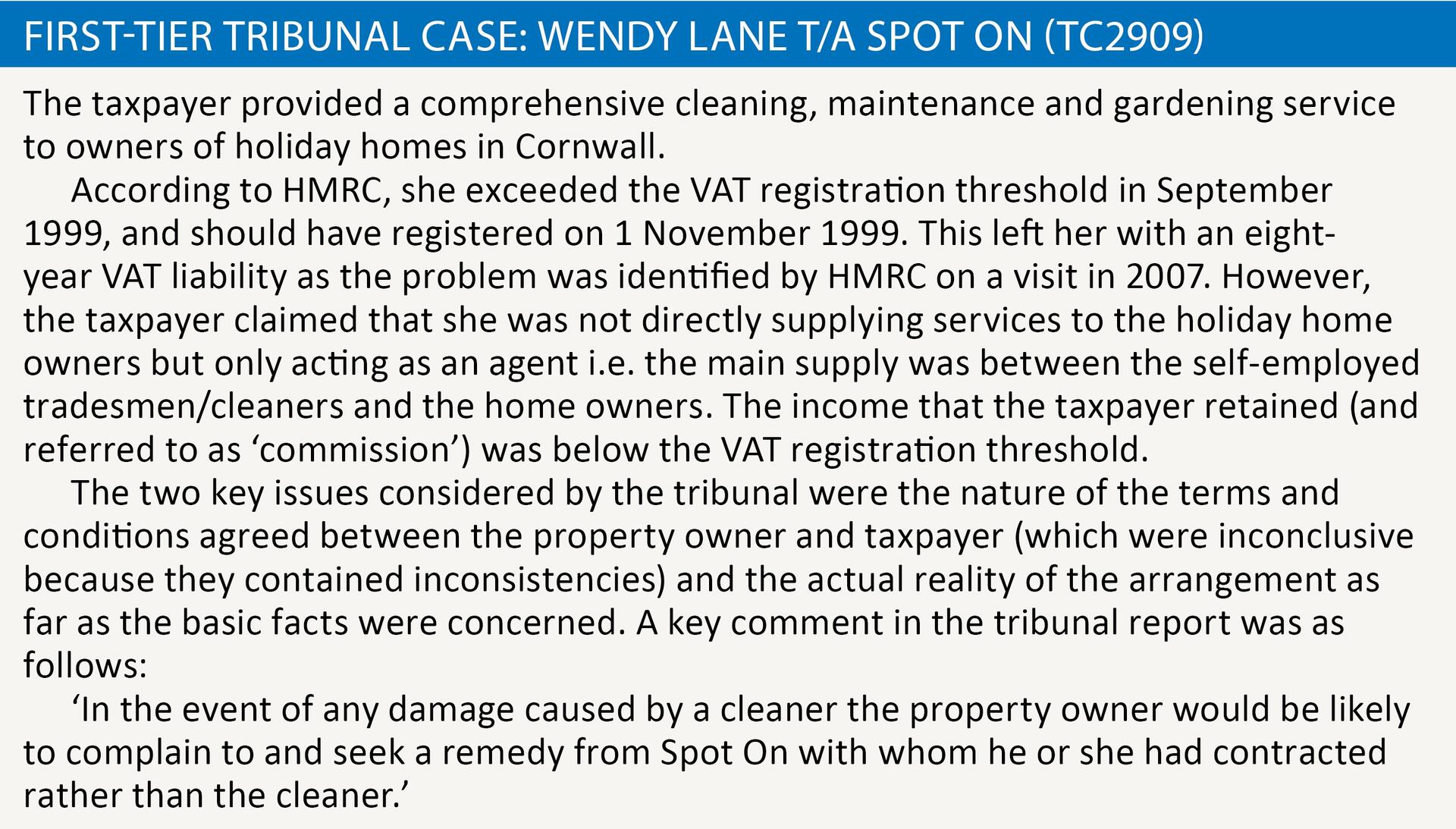

When I was on the speaking circuit, a case I enjoyed talking about to highlight the key issues of three party transactions involved Wendy Lane T/A Spot On (TC2909). This case did not produce a happy ending for the taxpayer. See First-tier Tribunal case.

The appeal was dismissed – the taxpayer was deemed to be acting as a principal.

Final tale

An unfortunate habit of clients and some accountants is to wear the wrong glasses when looking at three party transactions, with a tendency to see an arrangement in the best possible light in terms of the VAT position when the reality might be very different. Think about this issue if you act for any taxi, hairdressing or beauty industry clients where a main business such as e.g. a hairdressing salon utilises the services of a range of self-employed individuals such as stylists. Always remember that HMRC can go back up to 20 years to correct a belated VAT registration – the time period is not capped at four years as is the case with the correction of errors on previous VAT returns.

To share a final story with you, I advised on another scenario recently involving a musical concert where the three relevant parties were the venue, the production company organising the show and the punters buying the tickets – and both the production company and venue thought the other business was accounting for output tax on the ticket sales. A key message with VAT is to always consider issues at the planning stage of a deal, rather than when the money starts to roll in, by which time it is a case of trying to sort things out after the horse has bolted. It’s all very tricky … and three party transactions are certainly a part of the VAT system where there are shark infested waters in abundance. All swimmers must take great care!