Signposting changes

Share this article

Jane Mellor considers twelve professional standards topics that members need to consider to stay compliant

Key Points

What is the issue?

The challenge of keeping up to date with membership requirements and legislative changes affecting professional standards.

What does it mean to me?

It is important to review policies, procedures and practices to ensure you meet existing and new requirements not only in relation to tax matters but also non-tax professional matters.

What can I take away?

This article acts as a checklist covering areas where legal requirements or guidance has changed over the last year.

As we approach the end of one tax year and the start of another many tax people take time to draw breath and consider all the other areas which they may not have had time to think about over the busy self-assessment return months. Now might be an opportune time to consider a number of professional standards areas and make sure you have considered the implications of changing requirements and updated guidance.

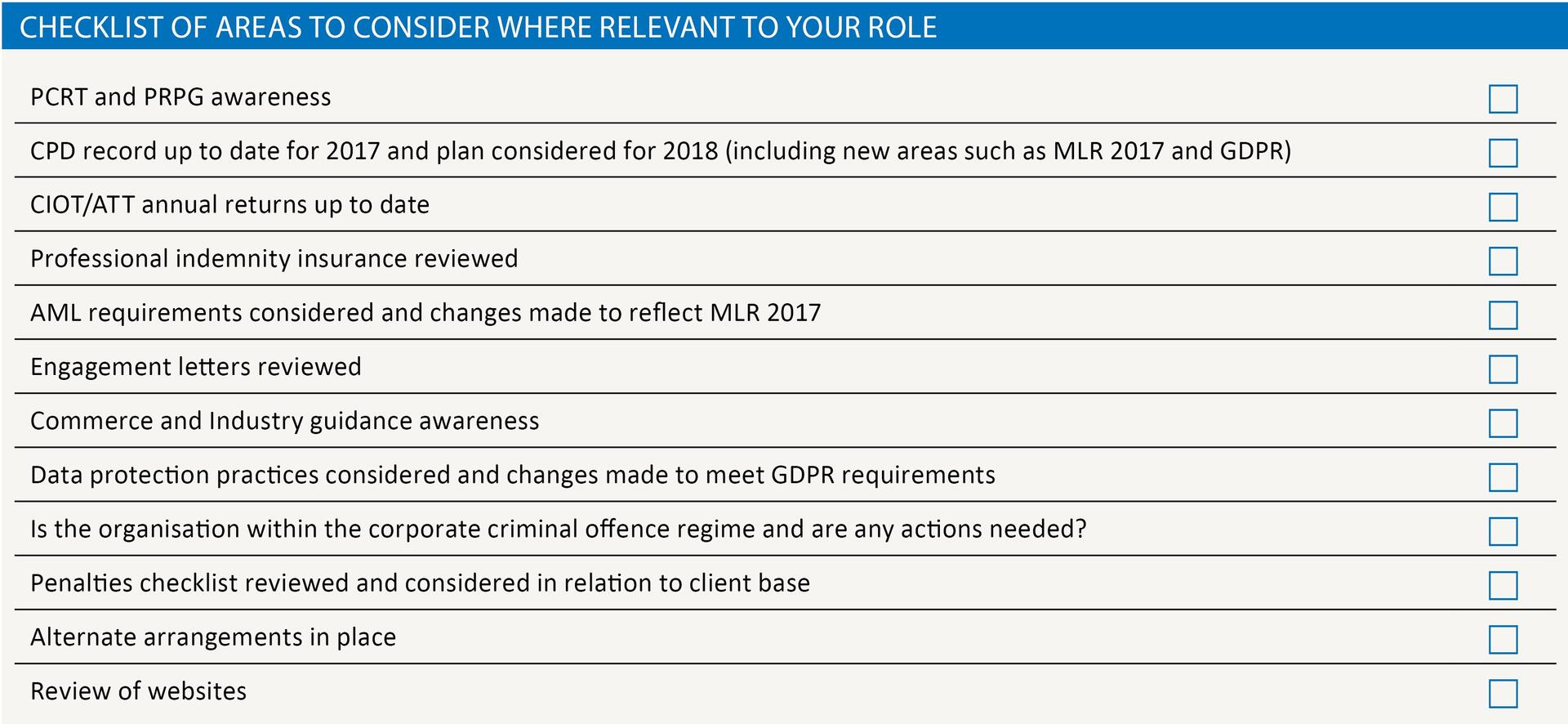

This article has been produced with a checklist at the end so you can tick off each area once considered no matter which tax field you work in. It is not exhaustive and there may be other areas you want to take the opportunity to consider.

1. Professional Conduct in relation to Taxation (PCRT) and Professional Rules and Practice Guidelines (PRPG)

All members are required to comply with PCRT (CIOT and ATT) and PRPG. As well setting out membership obligations there is a lot of useful practical information included in these documents which will help members in their work.

It is particularly important that members are aware of the update to PCRT which came into force on 1 March 2017 and includes five new tax planning standards. An updated edition of PRPG will be issued later this year.

2. Continuing Professional Development (CPD)

CPD is important because it helps members to carry out professional and technical duties competently throughout their working life. The CPD regulations applying to members changed on 1 January 2017. As a reminder:

‘compliance with the Regulations is compulsory for all members of the Chartered Institute of Taxation (CIOT) and the Association of Taxation Technicians (ATT) and Advanced Diploma in International Taxation (ADIT) affiliates who:

1.2.1 provide tax compliance services, advice, consultancy or guidance in tax including, without limitation, those in private practice, the public sector, commerce, industry or not for profit sector;

1.2.2 do not fall in paragraph 1 above but who use the designation, CTA, CTA (Fellow), ATII, FTII, Chartered Tax Adviser, ATT, Taxation Technician, ATT (Fellow), Taxation Technician (Fellow), ADIT affiliate or International Tax Affiliate of the Chartered Institute of Taxation.’

Members are required to perform such CPD as is appropriate to their duties, subject to some exemptions which are set out in the guidance.

The CIOT and ATT undertake a random audit of CPD records each year and members should be prepared in case they are selected. Now is a good time to make sure records to the end of December 2017 are complete and a plan has been considered for 2018. For further guidance on CPD see the updated regulations and guidance and the article which appeared in the December 2016 issue of Tax Adviser. CPD records forms are also available on the websites.

3. Annual return

The annual return helps CIOT and ATT to keep member records up to date. It provides the means by which members self-certify that they have met their requirements in relation to CPD and Professional Indemnity Insurance (PII) where relevant. Anti-Money Laundering (AML) supervisor details are also required from members in practice and this is a crucial part of the monitoring required by CIOT and ATT as supervisors. Members are also asked to provide answers to a number of questions in relation to their conduct.

The completion of the CIOT or ATT annual return is a compulsory requirement of membership. If members have any returns outstanding please bring these up to date promptly by logging on to the membership hub.

4. Professional Indemnity Insurance (PII) (Principals in practice only)

PII is important because it protects members and their clients and therefore members in practice are required to have PII which complies with the CIOT and ATT regulations. When renewing PII cover members should consider the nature of their practice and whether the minimum required by the regulations is appropriate. It is also important to be transparent and forthcoming on the proposal form for PI insurance and it is worth looking again at Karen Eckstein’s article in the October 2017 issue of Tax Adviser.

5. Anti-money Laundering (AML) Supervision (Principals in a practice only)

It is a legal requirement that members providing tax advice must be registered for AML supervision. Sole practitioners whose only AML Supervisor professional body is the CIOT or ATT should be registered with the respective body for supervision. Members of other professional bodies should be registered with those bodies where appropriate.

In addition the Money Laundering Regulations (MLR) 2017 brought in a number of changes and members in practice must consider what changes they need to make within their practice to meet new requirements. The AML newsletters issued by the Professional Standards team since July 2017 refer to these changes and a free webinar is also available. The CIOT and ATT have recently produced a set of updated frequently asked questions which gives members further guidance. Members should also refer to the updated AML guidance for the accountancy sector (known before as CCAB guidance) and the tax sector appendix (CIOT and ATT).

6. Engagement letters

It is not mandatory for members to provide their clients with engagement letters but it is strongly recommended to have them in place. Pro forma letters are available on the websites (CIOT and ATT) for members to tailor for their practice. Members should note that where they do not provide engagement letters there is still a minimum amount of information which must be provided to clients under the requirements of the Services Directive and a summary is included on the websites.

It is important to ensure the letters are regularly reviewed and updated where the terms or scope of the engagement has changed. Updated pro forma engagement letters which will reflect technical changes, including new legislation such as GDPR, will be issued later this year. Watch out for announcements over the coming months.

7. Members working in Commerce and Industry

The CIOT and ATT have responded to member feedback from those working in Commerce and Industry who requested guidance focused on their particular circumstances. Over the last year guidance has been published on both the CIOT and ATT websites. This includes:

An introduction to the Senior Accounting Officer (SAO) regime. This is likely to be of particular interest to those members working for or providing information to the SAO or those who work for a company which has recently met the threshold to be within the regime.

Frequently asked questions in relation to dealing with irregularities/differences of opinion and being asked to provide advice in a personal capacity.

8. Data protection and cyber security

The protection of data and the security of IT systems is an important area when members are considering how to protect their businesses. Members should be registered with the Information Commissioners Office (ICO) and now is an ideal time to review current data protection arrangements particularly in view of the changes applying from 25th May 2018 when the General Data Protection Regulations (GDPR) come into force.

Emma Rawson (ATT Technical officer) has written two articles covering this which provide a good introduction to members and you may also like to refer to ‘Taming the Wild West’, an article on GDPR which appeared in Tax Adviser in October 2017. However much still remains unclear under GDPR. We have collated a number of queries from members on the practical application of GDPR and we are seeking clarification on these points.

Cyber security goes hand in hand with protecting your data and if you haven’t already done so why not take advantage of the free cyber security training available on the websites?

Employees need to be aware of issues in relation to GDPR and cyber security. Employed members should ensure their own CPD reflects the data protection and cyber security information they need to do their jobs.

9. Criminal Finances Act 2017

Corporate bodies and partnerships must consider the implications of new legislation on corporate offences of failure to prevent the criminal facilitation of tax evasion (Criminal Finances Act 2107) which was introduced on 30 September 2017.

This is a complex area but the following elements are required in order for the offences to apply:

- Fraudulent tax evasion by a taxpayer (either an individual or a legal entity) under existing law

- The criminal facilitation of the tax evasion by a person associated with the corporate, acting in that capacity (referred to as a ‘relevant body’) who is acting in that capacity

- The relevant body failed to prevent the person associated with it from committing the criminal facilitation act

The relevant body has a defence if:

- It has put in place ‘reasonable prevention procedures’ to prevent its associated persons from committing tax evasion facilitation offences; or

- It is unreasonable to expect the relevant body to have such procedures in place

An introductory note is included on the websites and it is important that those businesses that come within the legislation ensure they have adequate policies and procedures in place. Staff should also be aware of the potential implications of their actions on their employer and should take note of policies and procedures in this area.

10. Penalties applicable to clients and advisers

We have already covered a number of areas which members need to consider to meet the regulatory and legislative requirements on their practices. Members should also take a moment to consider some of the recent changes which might be relevant when handling and advising clients.

A number of new penalties have been introduced through legislative changes over recent years in the areas of tax avoidance and offshore tax evasion and non-compliance. As tax penalty legislation is updated it is important that tax advisers are aware of these changes and seek to minimise exposure to these penalties for their clients and for their own practice.

Following feedback from members, the CIOT has produced a summary of the changes to the avoidance and offshore penalty regimes in recent Finance Acts and the Criminal Finances Act 2017. These changes relate to penalties chargeable on both taxpayers and tax advisers.

The checklist is intended as a guide for members to help them when considering the implications in relation to their clients and their practice, and to assist members in meeting the professional standards required from them. The list is not exhaustive and does not cover routine compliance penalties.

The intention is to keep the checklist up-to-date as and when new legislation and/or guidance is published. It can be found on the CIOT website.

11. Appointing an alternate

One of the last things members want to think about is what would happen if they were ill or passed away. Advance planning is important here for the protection of a member’s practice and clients.

The appointment of an alternate is strongly recommended so that someone could step in to run a practice in a member’s absence. The CIOT and ATT have updated the guidance document covering this and the guidance includes a sample agreement.

We understand that a number of members have had difficulties in identifying an alternate local to their practice and who would be willing to take on this role. We are eager to hear feedback if this has been your experience and would ask you to email us with details of your experiences.

12. Review of websites

Many members now have websites to advertise their services. It is important to review these on a regular basis and ensure the content is up to date. A number of common issues have been identified in relation to member websites and a guidance note has been issued which covers some hints and tips for members when reviewing their site (CIOT and ATT).

Conclusion

In the ever changing world of tax there is already more than enough to do servicing the needs of clients or the entity you work for and keeping up to date with technical changes. Understandably there can be little spare time to deal with all of the other administrative requirements. It is, however, important for members to carve out some time to deal with membership and legislative requirements and by picking off jobs in small bite sized chunks members can save themselves from headaches down the line.