A simpler way of giving

Share this article

The OTS’s second report on inheritance tax seeks to simplify and clarify the tax rules, explains Bill Dodwell

Key Points

What is the issue?

The OTS’s second report on inheritance tax contains 11 recommendations to deliver a more coherent and understandable structure of the tax.

What does it mean to me?

The proposed simplifications – including lifetime gifts, capital gains tax, businesses and farms and term life assurance – would reduce the administrative burden of inheritance tax.

What can I take away?

Delays in the new Chancellor’s response are likely in the current climate, but a positive reception would benefit tax advisers, donees and recipients.

In January 2018, Chancellor Philip Hammond asked the Office of Tax Simplification to review inheritance tax. The key part of his letter said:

‘The review should include a focus on the technical and administrative issues within IHT, such as the process of submitting returns and paying any tax due, as well as practical issues around routine estate planning and disclosure. It could also look at how current gifts rules interact with the wider IHT system, and whether the current framework causes any distortions to taxpayers’ decisions surrounding transfers, investments and other relevant transactions.’

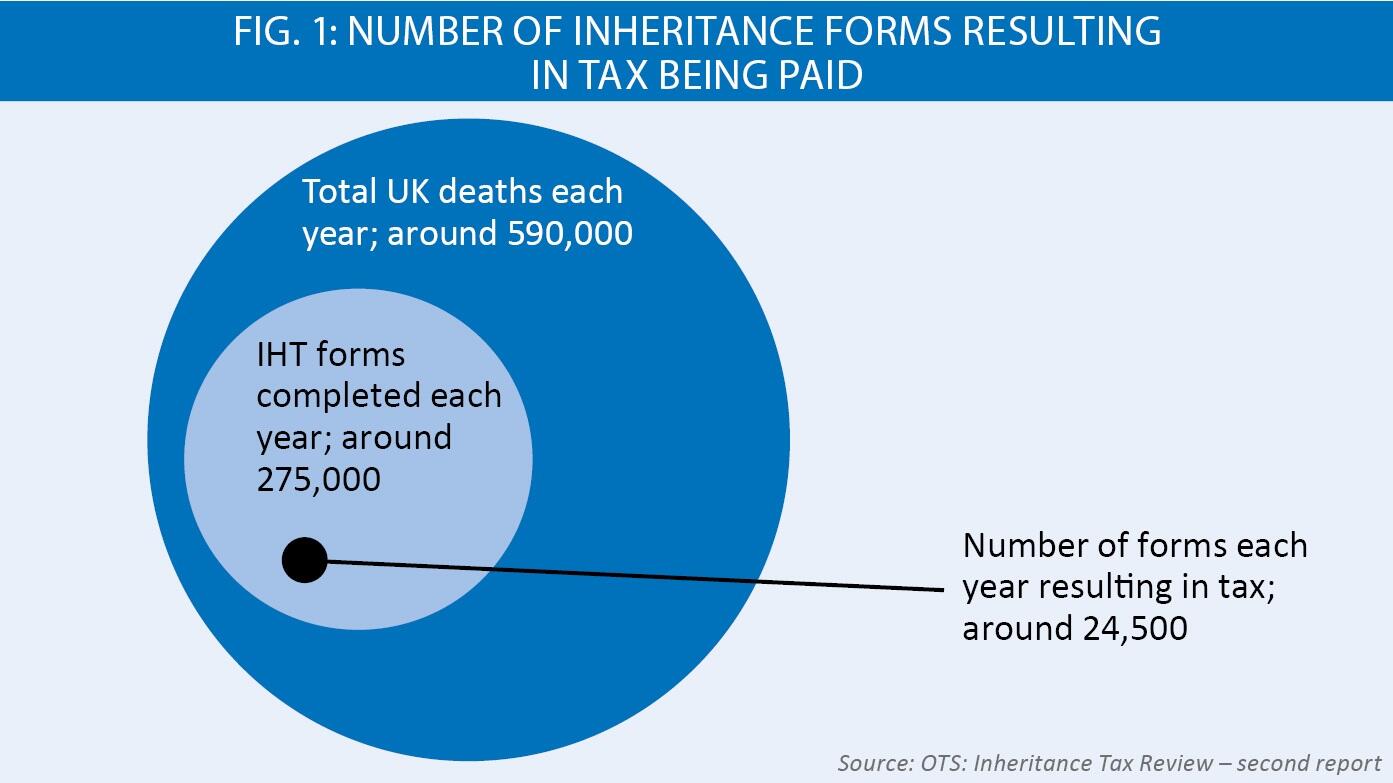

The first report was published last November and focused on the administrative aspects of the tax. The most striking point is that over 270,000 estates are required to file inheritance tax forms – but less than 10% (fewer than 25,000 estates) actually have a tax liability (see Fig. 1). There was little information available about inheritance tax, since the manual systems used and the small number of taxpayers meant there was little investment in gathering data. One big benefit of the OTS’s review was that HMRC’s Knowledge Analysis and Intelligence group gathered substantial amounts of information – which has now been published.

Inheritance tax was introduced in 1986 and applies primarily on death, but also to gifts made to individuals within seven years of death and to lifetime gifts other than to individuals, charities and qualifying political parties. It’s not a gift tax, such as applies in Ireland and which applied in the UK under the previous capital transfer tax regime. Currently, it brings in about £5.2bn, which should be seen in the context of total taxation of about £750bn.

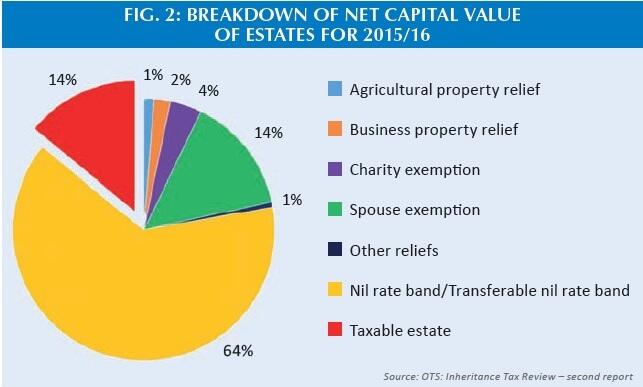

It’s a tax rather defined by its reliefs and exemptions, which at least theoretically vastly exceed the tax raised (see Fig. 2).

The nominal cost of the £325,000 nil rate band is about £17bn. Charity reliefs are about £900m, which is almost all represented by the exemption for gifts to charity with a small amount for the 4% rate reduction where at least 10% of the estate goes to charity. Business property relief costs over £700m, with agricultural property relief costing another £300m.

The OTS carried out a survey to seek evidence for its work. There were over 3,000 responses, with the majority being from individuals actually or potentially affected. The OTS also received 500 written comments.

Alternatives?

Some respondents wanted the OTS to look at alternatives to inheritance tax. However, that wasn’t within the remit set by the Chancellor. Where possible, though, data was published to help others considering alternatives. One of the ideas put forward is that inheritance tax should be scrapped and replaced by capital gains tax on death. Whilst perhaps more people are familiar with capital gains tax, imposing it on death would mean that about 200,000 estates would be liable to pay it instead of the 25,000 liable to inheritance tax. The underlying reason is that the CGT exempt amount is £12,000 – not £325,000. The overall yield would be halved as well, even if the main residence exemption was removed on death. Half the money and eight times as many returns… There is unfortunately no available data on other replacement tax options, such as a gift tax.

Other suggestions were to abolish the residence nil rate band – and instead boost the general nil rate band by a similar amount. The residence nil rate band does turn out to be complicated to understand, since it applies only on death, where the deceased owned a main residence, has a total estate below £2m and leaves money to lineal descendants (principally children and grandchildren). However, most of the objections came from those who disliked the policy – which goes beyond the simplification remit of the OTS. It’s also worth understanding that if the residence band were abolished, it would give only enough money to add about £50,000 to the general nil rate band. It would also mean an additional 5,000 or so estates would be liable to pay inheritance tax.

The final observation concerned agricultural and business property relief. Again, the comments overvalued the costs of the reliefs, thinking that their abolition could allow the rate of inheritance tax to be cut to 20% from 40%. This proved over-optimistic; the numbers from HMRC suggest that the rate could only be cut to 33%.

Recommendations

The report contains 11 recommendations to deliver a more coherent and understandable structure of the tax. Four main areas are grouped as packages, where some elements have an Exchequer cost and others raise money. They are:

- the taxation of lifetime gifts;

- looking at who pays tax where lifetime gifts are taxable;

- simpler exemptions for lifetime gifts; and

- a review of business exemptions to ensure they are focused on the policy goals and are consistent across different taxes.

Lifetime gifts

There are several exemptions from inheritance tax relating to lifetime gifts, which haven’t changed since the 1980s. These are exemptions for the first £3,000 given away each year, for individual gifts of up to £250, gifts to someone getting married or entering a civil partnership and regular gifts out of a person’s disposable income.

The survey and other consultations have revealed that the taxation of lifetime gifts is both widely misunderstood and administratively burdensome.

Accordingly, the OTS recommends the following steps:

- Replace the multiplicity of lifetime gift exemptions with a single personal gift allowance, to be set at a sensible level, and incorporate an increased lower threshold for small gifts. The exemption for regular gifts should be reformed or replaced with a higher personal gift allowance.

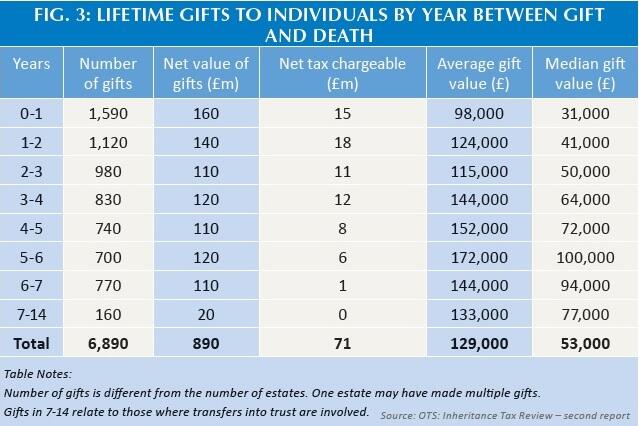

- Shorten the seven-year period to five years (significantly reducing the workload on executors) and abolish the tapered rate of inheritance tax (which many find works in a counter-intuitive way). Data made public for the first time shows the tax paid on gifts six or seven years before death is low (see Fig. 3).

Finally, where there is inheritance tax to pay on lifetime gifts, the OTS recommends that the government explore options for simplifying and clarifying the rules on who is liable to pay this tax, and how the £325,000 threshold is allocated between different recipients. At present, lifetime donees are primarily liable for any inheritance tax on the gift they receive – and the nil rate band is allocated to gifts in the order in which they are made.

Few – other than specialists – appreciated this and many people don’t seek tax advice before giving away assets or money.

Capital gains tax, businesses and farms

The OTS consultation highlighted complexity in the interaction between inheritance tax and capital gains tax, as well as in relation to the reliefs available for businesses and farms. Aspects of the regime distort the decisions that families face when passing assets to the next generation, where there are different tests applying to what is broadly the same activity.

The underlying policy is to permit family businesses and farms to pass to the next generation without a tax lability – so they can remain in family ownership, without needing to be sold to pay tax liabilities. However, there are different definitions for trading activities in capital gains tax and inheritance tax. Business asset holdover relief in CGT requires that substantially all the activity is trading. This is a version of the substantial shareholdings’ exemption for the sale of trading companies and is generally taken to mean that over a period 80% of the assets, profits and employees are engaged in trading activities. By contrast, the equivalent test for inheritance tax is ‘mainly’, which is taken as meaning that just over 50% of the activity is trading-related. The OTS recommended that the government should consider whether these differences were justified in the light of policy objectives.

One area where distortions can apply concerns the so-called capital gains tax uplift on death. CGT isn’t charged on death and the beneficiaries receive the property at market value. The report recommends that this uplift shouldn’t apply where an inheritance tax exemption also applies. Instead, the beneficiary should take over the capital gains base cost of the deceased. This means that there would still be no tax to pay (either CGT or inheritance tax) where the business or farm remains in family ownership. However, if it is sold then one level of tax on the growth in value would apply.

A similar approach should apply where the inheritance tax spouse exemption applies; after all, if property had been transferred between living spouses it would go on a no gain, no loss basis. Having different rules on death encourages people to hold on to assets when it would be better to transfer them earlier.

Term life assurance

Whilst term life assurance might be a niche area, the OTS was aware that policies written in trust remained outside the estate but without this complexity, the proceeds would form part of the estate. In many cases, inheritance tax would probably not apply, due to the spouse exemption and/or the nil rate band. However, it seemed an unnecessary complexity for a protection product. Accordingly, it was recommended that all term assurance should be exempt from inheritance tax. This recommendation did not extend to any policy with a savings element, such as whole life assurance.

As a Chancellor-commissioned report, it has been laid before Parliament and it will be for the new Chancellor to consider a response. No doubt it won’t be near the top of his in-tray but we hope that the proposals will be taken forward in the future.

The full report is on GOV.UK and the animation highlighting the main points is on YouTube.