Starting from scratch

Share this article

Jo White considers the IHT challenges for land with development potential

Key Points

What is the issue?

With the government imposing higher housing on local councils, more individuals are being approached to sell their land for development.

What does it mean to me?

Development value can increase individual’s estates for IHT purposes meaning IHT planning is becoming more critical.

What can I take away?

The timing of the planning is important where land values are subject to increases. It is possible for the whole family to benefit from the sales proceeds of the land and help to minimise your clients IHT exposure. Multiple taxes need to be considered to ensure the overall position is presented to the client.

Living in the South East of England I see a number of clients who are approached by developers to purchase their land. This could be because they are looking to develop on the site straight away or they may do in the future.

When looking at inheritance tax planning for such clients the immediate issue to address is whether the land they own has increased in value. This is as a result of being approached by a developer, or indeed they own land where their neighbour has recently sold it for such purpose.

‘Hope’ or ‘development’ value can result in increased inheritance tax exposure to their estate. It can also mean starting to lose the Main Residence Nil Rate Band due to their estate’s value increasing beyond £2,000,000. By 2020/21 this could mean a loss of a further £350,000 of relief against their combined estates’ value when calculating any inheritance tax payable.

Given the potential increase in value and the limited availability of inheritance tax reliefs, it is these assets which can prove valuable when considering inheritance tax planning. If the client is happy to give away some or all of the current value and potential development value then the gift can be fixed at today’s value and the enhanced value will completely fall outside of their estate. A double bonus perhaps?

When I sit down with such clients it is important to understand what the land is being used for. Is the land at the bottom of their garden? Is the land currently being used in their farming business? Do they run a non-agricultural business from the site? Where possible you want to benefit from any reliefs available and therefore understanding the use of the land can better allow you to assess the reliefs available.

This article does not cover any Scottish or Welsh tax considerations and therefore separate thought needs to be given to these where the land or individuals are situated outside of England.

Capital Gains Tax

The gift of the land itself will be a disposal for Capital Gains Tax (CGT) purposes with the ‘sales proceeds’ being equal to the current market value of the land. This means the recipient of the land has a base cost equal to the market value at that time allowing only the increase in value from this point to be subject to future CGT for them unless of course an election is possible to holdover the gain arising.

It is possible the land has been owned a long time or where it has historically been solely for agricultural use, it could have a relatively low value per acre. This could mean that that a significant amount of CGT could be due on the transfer of the asset.

If the land is being used in a business then it may be possible to hold-over the gain subject to certain conditions. TCGA 1992 s 165(2) states that relief for gifts of business assets is available where the asset has been used for the purpose of a trade carried out by the transferor.

If the land is being used for agricultural purposes then under TCGA 1992 Part 1 Sch 7, a hold-over relief claim is available providing the land qualified for APR under IHTA 1984.

If the land was part of the donor’s garden then it may be possible to claim Principle Private Residence relief. However, TCGA 1992 s 222(2) states that this relief is only available if the land being disposed of is within the permitted area. Even though TCGA 1992 s 222(3) states that land included in the relief can be larger than 0.5 hectares (approx. 1.2 acres) if ‘… the size and character of the dwelling-house, that larger area is required for the reasonable enjoyment of it (or of the part in question) as a residence’. The land has to be used as part of your garden, therefore a field at the bottom of the garden fenced off, or an areas used as stables and a paddock wouldn’t be included so full CGT would be payable.

If the land is being transferred into trust for a number of individuals’ benefit (say, the client’s children and grandchildren) then hold-over relief under TCGA 1992 s 260 will be available. This will mitigate the CGT liability on the initial transaction but clients should be aware that as the original cost becomes the trustee’s base cost this will mean a higher CGT liability could arise in the future when the land is later sold. This also assumes that the value (on the diminution in value principles) is covered by the Nil Rate Band; otherwise an immediate charge to inheritance tax will arise (unless APR/BPR is in point).

At this stage it is worth noting that if the land in question had decreased in value then there would be no immediate profit which would be subject to tax. This transaction would generate a capital loss. If the disposal was to a connected person (child, grandchild for example) then the loss would be a clogged loss under TCGA 1992 s 18(2) and only relievable against any chargeable gains generated by further disposals of assets to the same person(s).

Inheritance tax

A gift to an individual absolutely is a Potentially Exempt Transfer (‘PET’). Providing the donor survives seven years from the date of the gift then no inheritance tax will be payable on their death. If they die within the seven year period then taper relief (IHTA 1984 s7(4)) may be available reducing the inheritance tax payable. Remember however, that Taper Relief applies to any tax payable and not to the value gifted, so if the value of the gift is covered by Nil Rate Band, no taper will apply.

A gift to a trust is a Chargeable Lifetime Transfer (‘CLT’). Any value transferred in excess of the Nil Rate Band (currently £325,000 per person) will be subject to a lifetime inheritance tax charge at 20%. When considering whether or not there is any lifetime IHT payable you need to consider any other CLT’s made in the previous seven years. If there have been then the value of these gifts will be used to reduce the available Nil Rate Band which can be offset against the value of gift for calculation purposes.

Depending on how the asset has been used by the donor it may be possible to claim Agricultural Property Relief (‘APR’) or Business Property Relief (‘BPR’). These reliefs reduce the value of the gift being made for IHT purposes providing certain conditions are met. This is unlikely to be the case where the land with development potential is part of the donor’s home.

APR is assessed first. If the land being transferred is used for agricultural purposes then APR can be claimed. Under IHTA 1984 s 117 the land has to be used for the purposes of agriculture by the donor for two years up to the date of the gift or by a third party for seven years prior to this date. If APR can be claimed then this reduces the agricultural value of the land only. This is very important when considering land with potential development opportunities as any ‘hope’ value would not be subject to the relief. In these circumstances we would therefore want to try and transfer the land before any ‘hope’ value is established to maximise the APR claim.

BPR is then looked at in the context of a gift to an individual or to a trust. BPR can be applied to the whole value of the asset (including hope value) where the asset has been used for business purposes for up to two years before the date of the transfer. If the donor is a farmer and farms their own land, either physically or through a contract farming arrangement then the whole value could potentially qualify for APR/BPR.

Whilst we would only assess the amount of APR or BPR on the donor’s death when looking at any PET’s these reliefs are invaluable when transferring assets into a Trust as it could create the opportunity to transfer value much greater than the available Nil Rate Band into trust.

It is critical to remember that if a death occurs within seven years of a gift which qualified for APR/BPR, then the APR/BPR qualifications still need to be satisfied also at the point of death. In summary, the transferee needs generally still to own the asset and it needs to continue to qualify for relief up to the date of death. A sale of a qualifying asset after the gift within the seven years will generally result in the value of the gift falling back into the estate on that death.

Stamp Duty Land Tax (SDLT)

Where unencumbered land is gifted to an individual or a trust then no SDLT should arise. However, where the donor wishes to gift land which is subject to a mortgage SDLT could arise. This is on the basis that if the land is being gifted with the debt attached, i.e. the donee assumes the liability, then the assignment of that debt is consideration for SDLT purposes.

It may be possible for the client to refinance their assets and borrowings relating to the land under review so that it becomes unencumbered at the point of transfer. They should however seek independent financial advice to check the suitability of this.

It is also worth noting at this stage that previously for IHT purposes any borrowing was matched against the asset that it was secured against. This is no longer the case. Instead if you borrow against a non-qualifying BPR asset in order to purchase a BPR qualifying asset, the debt will be deductible against the BPR asset not the asset subject to IHT.

Use of Trusts

Although trusts can have a number of benefits in being created they do come with their own tax consequences. It is therefore important to make clients aware that if they do want to use a trust there could be potentially trust IHT liabilities every 10 years or when the capital is distributed to the beneficiaries. This will depend on a number of factors including the value of the assets held, the reliefs available and the type of trust formed.

Transactions in land

This is outside of the scope of this article, but whenever land is being sold for development purposes, it is important to also consider this anti-avoidance provision, to ensure that a charge to income tax does not arise on the gain on the ultimate sale of and for development.

Case studies

Land part of your home

Let’s look at Mr and Mrs Jones. They own land which has been part of their home for a number of years. The county council in which their property is situated has recently released a list of areas where they are allowing further development. One of the areas includes where their home is situated. Their neighbour has already been approached by a developer to purchase the bottom of their garden for a small development and Mr and Mrs Jones believe this could be the case for them in due course.

Mr and Mrs Jones are currently looking at ways of mitigating their combined inheritance tax position. They have a number of assets worth in excess of £2.5m between them. This is before any increase in the value of their land due to future developments. They have sufficient pensions and other income to manage their monthly outgoings, both paying higher rates of tax and therefore are happy to consider gifting some assets to their two children now.

Mr and Mrs Jones’ property sits in three acres of land which includes a fenced off field which is likely to be attractive to developers.

Mr and Mrs Jones were able to pay off their mortgage against this property a few years ago. It is therefore unencumbered and we can ignore any SDLT implications.

As the property is more than the permitted area we need to consider if the land which could be potentially developed is considered part of their garden for CGT purposes. Unfortunately as the site concerned is completely separate from their dwelling, PPR would not be available.

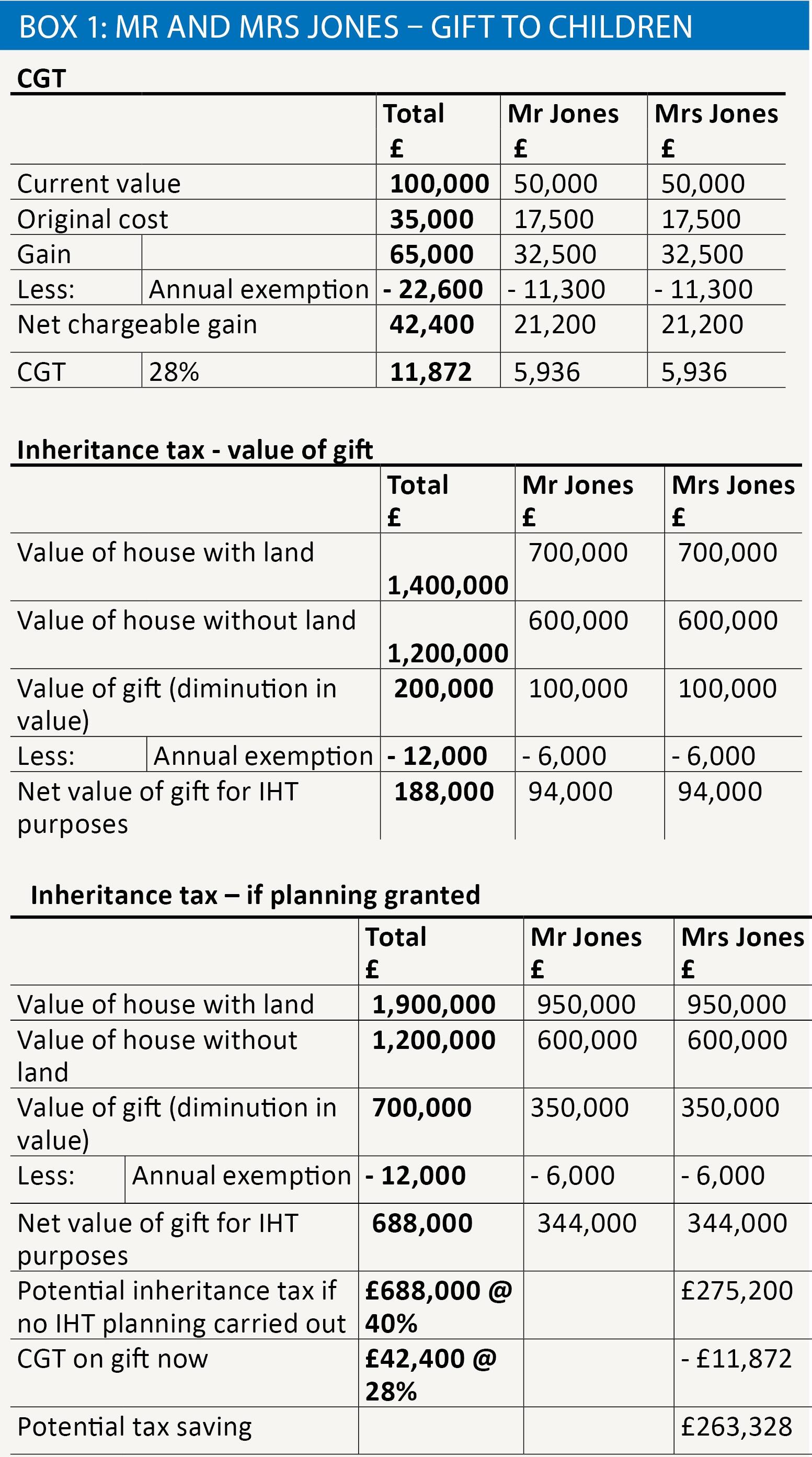

Mr and Mrs Jones have had the land area valued and it is estimated that currently it is worth £100,000. The same area of land was valued at £35,000 when they purchased the property in 1990.

It is estimated that if planning permission is granted on the land it could be worth £600,000.

The land hasn’t been used for any purpose other than their home for the whole period they have owned it.

If Mr and Mrs Jones were to transfer the land to their two children absolutely then we would estimate the CGT liability to be £11,872. This is based on the land being disposed of qualifying as residential property under TCGA 1992 s 4BB. On this basis the higher rate of 18% or 28% would be applied to any gain rather than the lower non-residential CGT rate, as per TCGA 1992 s 4(2A) .

For IHT purposes the gift would be a PET and therefore providing they survived seven years from the date of the gift no inheritance tax would be payable. As no reliefs are available for IHT purposes the value of the gift will be £200,000 under the diminution of value principles set out in IHTA 1984 s 3(1) . As Mr and Mrs Jones haven’t made any other gifts in the last two years they can each use their annual exemption from this current year and previous year (totalling £6,000) against the gift. This therefore reduces the gift value to £94,000 each.

Given the value of the land could be potentially £600,000 this option will save them £263,328 in potential tax. See box 1.

Given the potential value of the land Mr and Mrs Jones wanted to explore the possibility of using a trust structure. One of their children is married and their first grandchild is due in a few months. The other child is in a long term relationship. Whilst they trust their children they felt it may be better to allow the money to be used for all generations and also keep a level of control over what happens to the money, certainly in the shorter term.

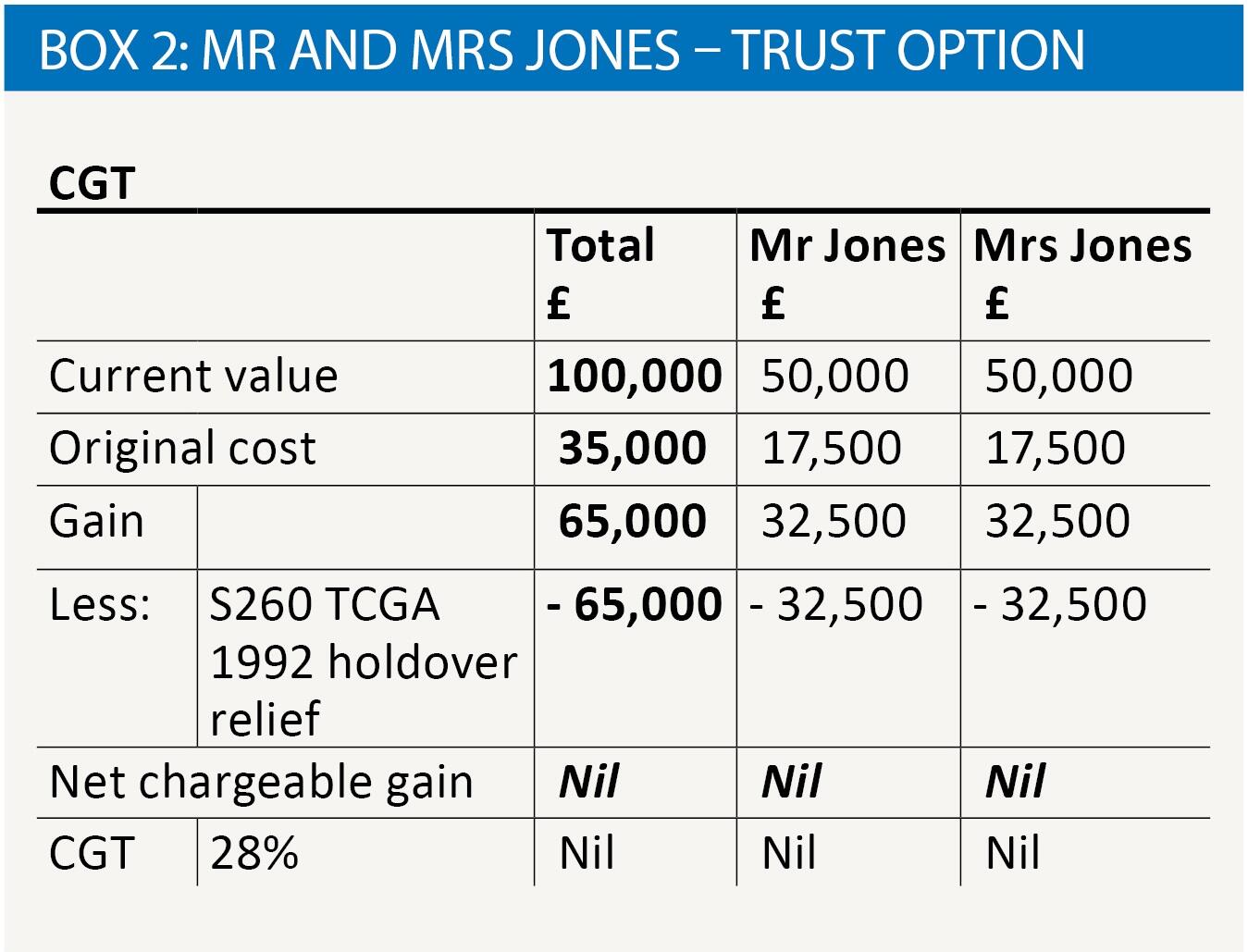

The CGT position remains the same as if they were to gift the land to their children directly. However, as explained earlier it is possible to hold-over the gain under IHTA 1984 s 260, deferring any CGT due. See box 2.

Mr Jones hasn’t made any other CLTs in the previous seven years however Mrs Jones set up a trust for the children with some inheritance she received from an aunt. The value of the CLT was £100,000 and therefore only of £225,000 her Nil Rate Band can be used to place value into a Trust by her before a lifetime IHT charge will arise.

Given the land value as it stands neither Mr nor Mrs Jones will create a lifetime IHT charge providing the land is gifted into the trust before the hope value is attached to the asset. Under this option they could potentially save £275,200 in inheritance tax, as per box 1 (without any CGT on the gift).

The inheritance tax position is the same as stated previously, therefore please refer to the previous tables.

Whichever option Mr and Mrs Jones decide the potential tax saving is fairly significant and worth carrying out before the land increases too much in value.

Farming land

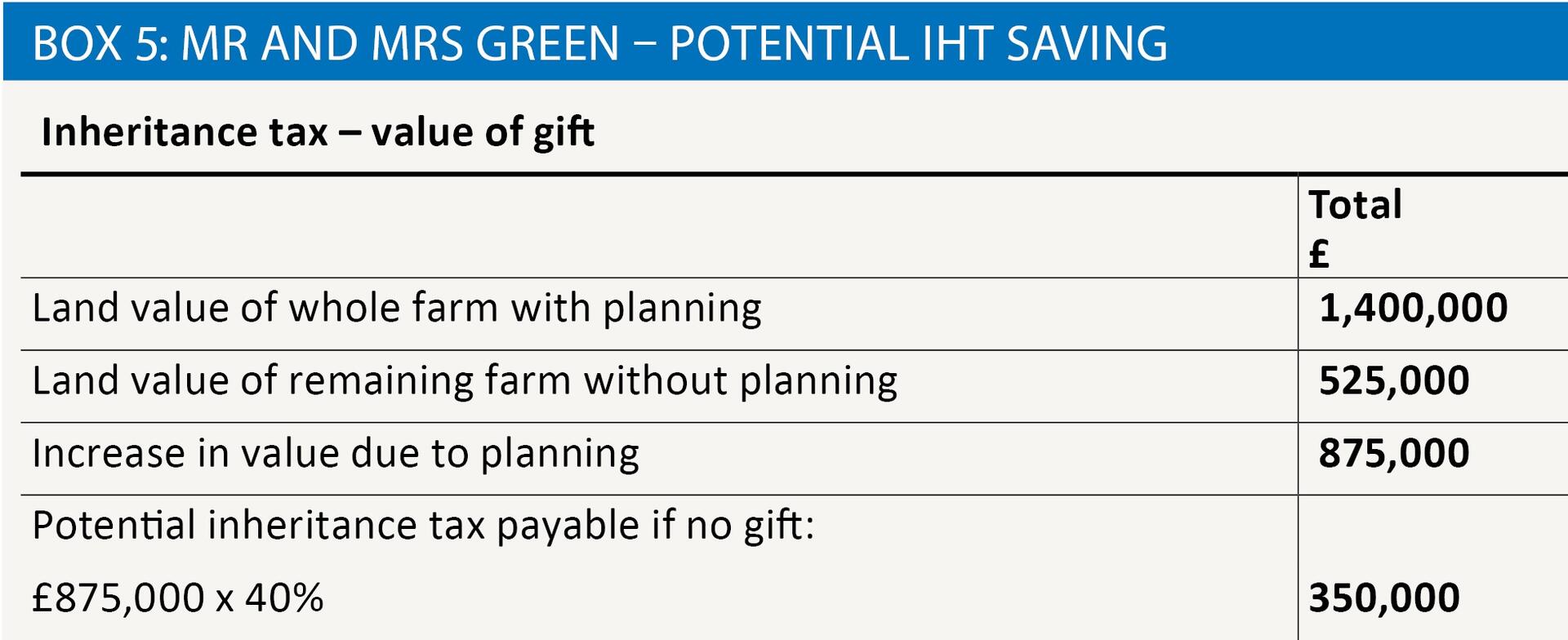

Mr and Mrs Green have owned and farmed the land adjacent to their home since 1980 when they inherited from Mr Green’s father. Part of their land could be of interest to a developer given the house building happening in their area. The land is farmed by Mr Green but is owned jointly by them. The land is owned separately to the business. Both Mr and Mrs Green are higher rate tax payers.

The land subject to potential development is approximately five acres. The value of the land at present is £125,000 and the valuer has confirmed that 80% of the value is agricultural value and 20% is not.

The valuer has estimated that the land could be worth £1,000,000 if planning permission were granted in the future.

As the land was owned prior to 31 March 1982 a value at this date is required. The valuer has confirmed it is £4,165.

Mr and Mrs Green want to help their son and his family financially but currently are asset rich and cash poor. They therefore feel that transferring this land to him now could help him out in the future, if not immediately. They also wish to look at inheritance tax planning as they are conscious that they haven’t done anything beyond writing their wills.

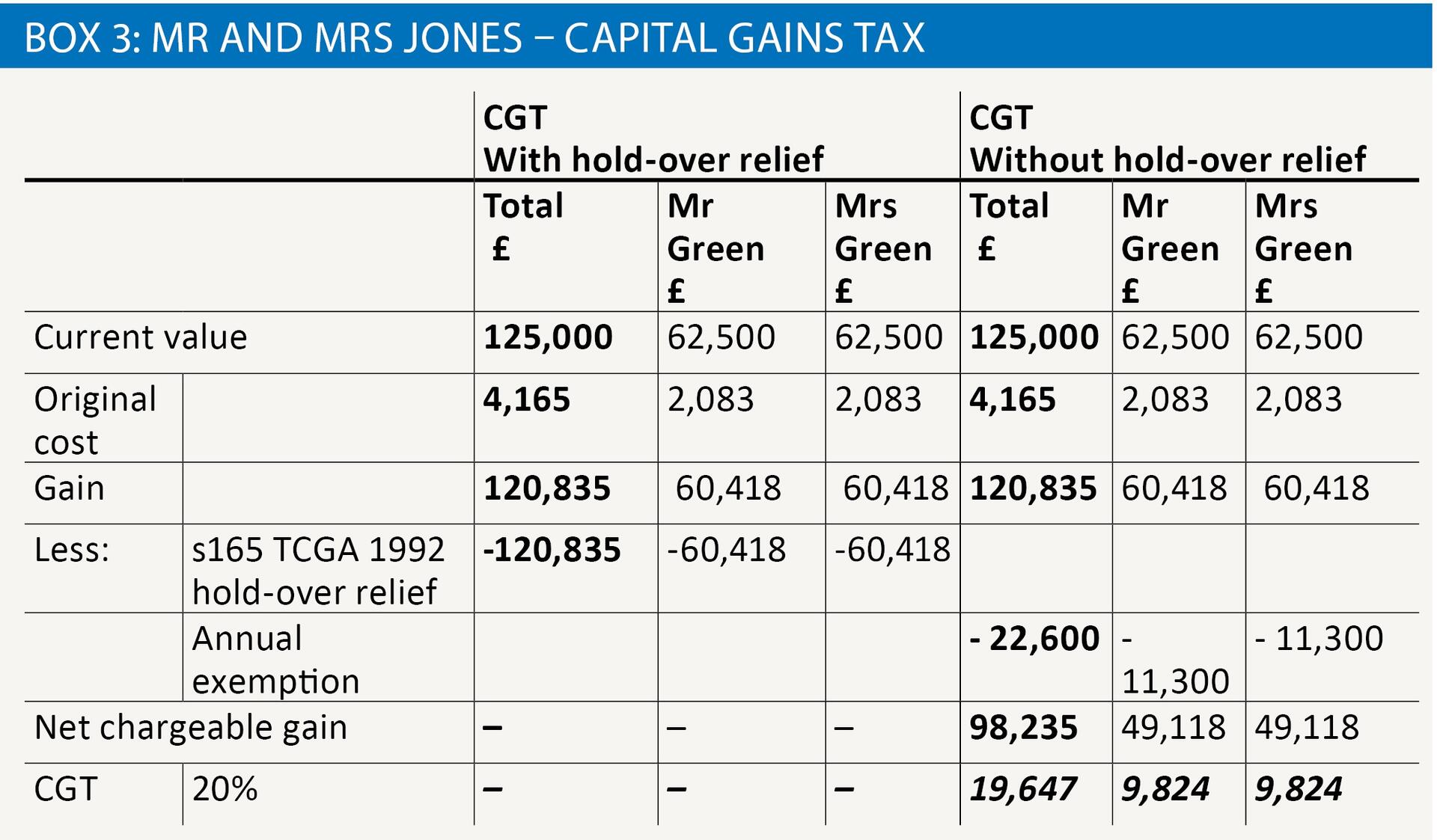

We first need to look at their CGT position. The transfer of land would be a disposal for CGT purposes. For Mrs Green as this is not a business asset for her she will only be able to claim hold-over relief if the land was transferred into a trust (or if she qualifies for APR, which is likely and can therefore claim in accordance with TCGA 1982 s 165(5) which extends business asset holdover to qualifying agricultural property).

For Mr Green as the asset is used in his business he will be able to claim TCGA 1992 s 165 holdover relief allowing him to defer his share of any CGT liability.

Based on the current value of the land the CGT liability would be £Nil if the land was given to their son absolutely. For Mrs Green, as the land is used for agricultural purposes and assuming that she qualifies for APR (see more below) then hold-over relief will be available. Please note that in these circumstances, the holdover is NOT restricted to the agricultural value and full relief can be claimed, even though there is hope value in the property which will not qualify for APR.

If hold-over relief was not available then their potential CGT liability would be £19,647. See box 3.

Assuming both parents qualify for holdover relief their son will have a base cost of the March 1982 value being £4,165.

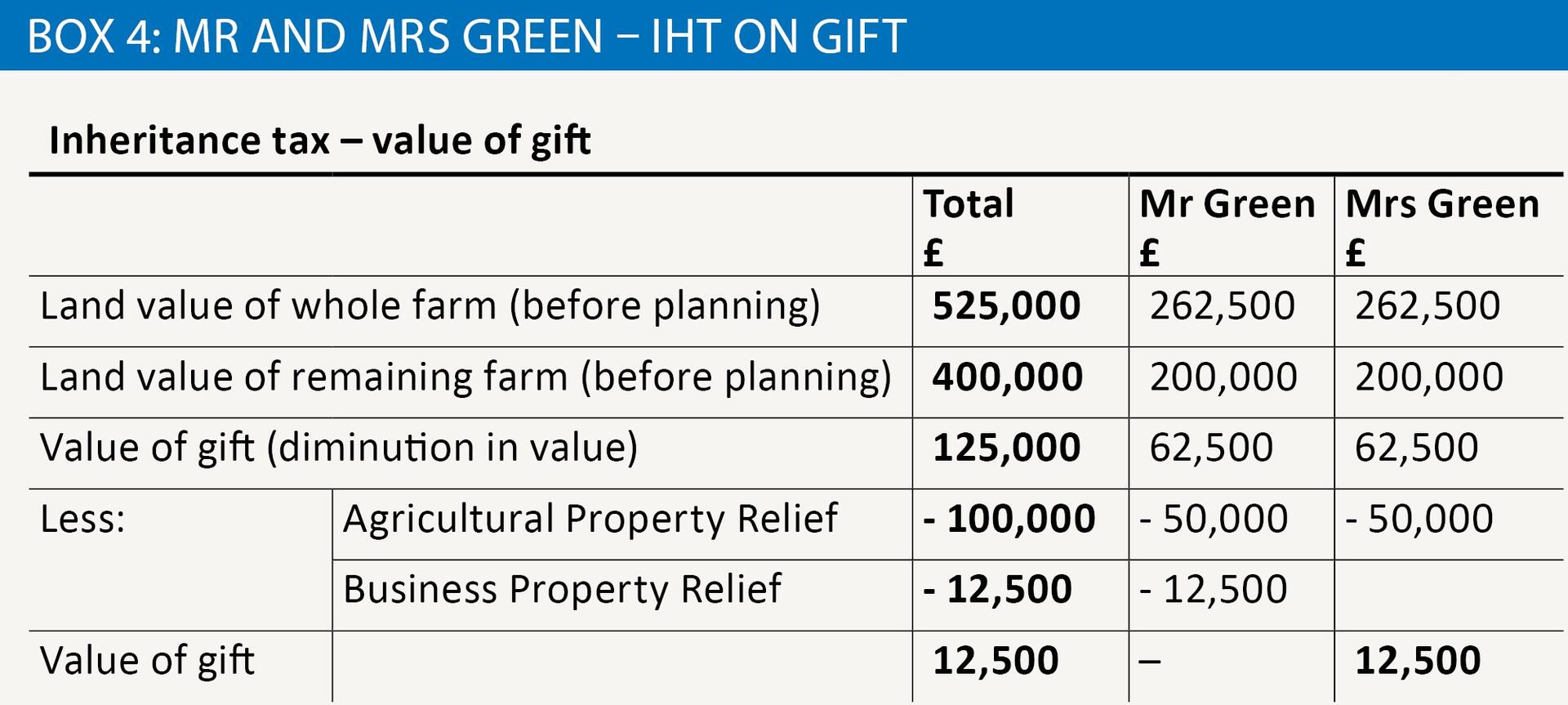

Although Mrs Green is not using the land herself, her husband is farming it and she should therefore still be able to claim APR as the land has been farmed for seven years up to the date of the gift. As only 80% of the current value of the land is agricultural value she will only be able to claim APR against 80% of her gift for IHT purposes. Mr Green will be able to claim both APR and BPR on the land reducing the value of the gift to Nil.

If the land was gifted to their son absolutely then a claim for either APR or BPR would not need to be filed unless either of them died within seven years of making the gift. If the land was transferred to a trust then the relevant claims would be made at this point. Based on the values of the land this would mean Mr Green doesn’t use any of his Nil Rate Band whereas Mrs Green uses £12,500 of her Nil Rate Band. Please note Mr and Mrs Green already use their IHT annual exemptions each year. See box 4.

As the land was inherited from Mr Green’s father there is no mortgage on the property therefore we do not need to consider SDLT.

Due to hold-over relief likely to be available on a direct gift; under both options Mr and Mrs Green will save a potential IHT liability of £350,000. See box 5.

Assuming the land continues to be used for farming until its sale it is worth discussing with the family whether any changes can be made to the current arrangements to try and maximise any Entrepreneurs’ Relief claim in the future. This may involve the son becoming a partner in the farming business but this is outside of the scope of this article.

In addition, as Mrs Green jointly owns the land but doesn’t farm it herself her estate is losing out on valuable IHT reliefs in the future. It would therefore be worth considering the current business structure to see whether it would be advisable for her to be introduced as a partner of the business to help maximise relief. This would need to be considered in conjunction with how the land is owned (i.e. inside or outside the partnership). If land is outside of a partnership only 50% relief applies. If the land was introduced into the new partnership and became a partnership asset, then 100% BPR would be available to both Mr and Mrs Green.

Due to the CGT relief’s available there is no difference in giving the land directly to their son or into a trust. However, the trust option would allow the money to stay separate from their son’s estate and help with future IHT planning for the family as a whole.