Student loans: the increasingly complex matter of repayment

Share this article

The repayment of student loans is becoming increasingly complex due to the growing number of repayment plans. We consider the different plan types, how and when student loans are collected through the tax system and how repayments work if the borrower has more than one type of loan.

Key Points

What’s the issue?

Many student loan borrowers repay their loans through the UK tax system (under The Education (Student Loans) (Repayment) Regulations 2009). The number of borrowers repaying student loans through the tax system will continue to increase each year and the introduction of the ‘lifelong loan entitlement’ will mean even more people repaying their loans through PAYE and/or self-assessment.

What does it mean for me?

Tax advisers completing self‑assessment tax returns need to understand how loan repayments through the tax system work for the various plan types and in different circumstances, such as working overseas or changing jobs.

What can I take away?

The importance of obtaining complete information from individuals on their student loans and understanding how repayments work, especially if they also have a postgraduate loan, unearned income or are working abroad.

From 1998 onwards, income-contingent student loans are usually collected by HMRC on behalf of the Student Loans Company either through a deduction via the PAYE system or through self-assessment tax returns. This article explains about the different plan types, how and when student loans are collected through the tax system and how repayments work if the borrower has more than one type of loan. It also discusses some quirks within the repayment process.

The Student Loans Company’s online repayment service is evolving with increasing options to make changes online. The ‘more frequent data sharing’ process between HMRC and the Student Loans Company should mean that loan balances are updated after every PAYE deduction.

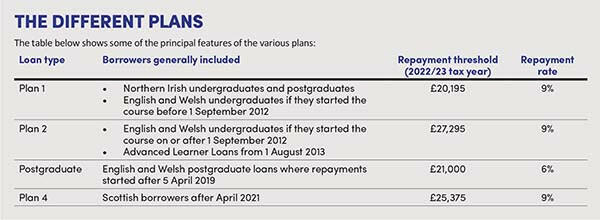

Income-contingent student loans fall under various ‘plan’ types and repayments differ according to which loan (or loans) the borrower has. A new loan repayment type, Plan 4, was introduced in 2021/22 for students who received loans from the Student Awards Agency Scotland. Borrowers on Plan 4 loans include new borrowers who started their repayments after April 2021 and Scottish Plan 1 borrowers whose loans have been moved to being repaid under Plan 4.

The 2021/22 self-assessment tax returns will be the first time Plan 4 loan repayments are included. Taxpayers filing their tax returns using HMRC online services should have any loan repayments deducted through the PAYE system automatically pre-populated on their self-assessment tax returns.

Student loan repayments

Student loan repayments usually start from the April after graduating or leaving the course if the borrower is earning above the relevant repayment threshold. So, if graduating in the summer of 2022, the first time a loan repayment will be made is April 2023, assuming that earnings are above the repayment threshold for the relevant plan type and there are no other income-contingent loans from previous courses.

Employees

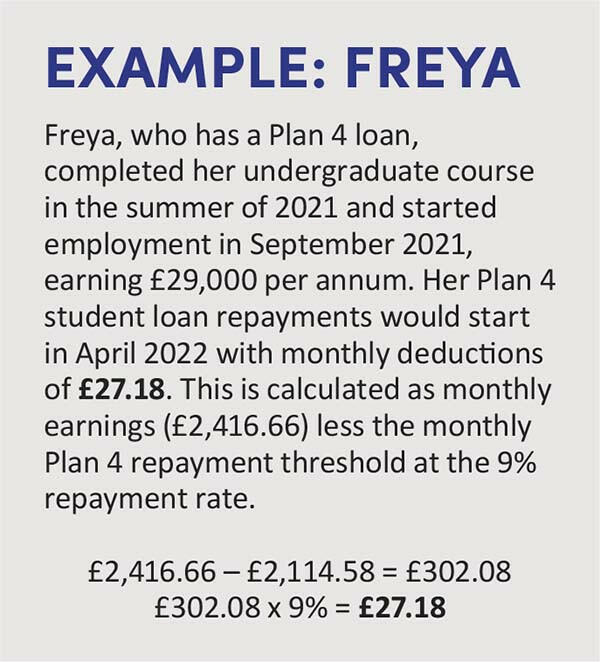

Employees will have their earnings for student loans purposes calculated in the same way as they are for National Insurance contributions (NIC), as shown in Example: Freya above. The repayments are deducted through PAYE so it is important that the correct plan type is used by the employer – the employee should state the correct loan plan on their starter checklist.

If student loan repayments are not due at the point of starting a job, no such box will be ticked on the starter checklist. If repayments are then due to begin from the following April, HMRC should send a start notice to the employer at the appropriate time.

If an employee’s monthly wages vary and they earn above the monthly repayment threshold in some months, then the student loan repayments will be deducted, even if their annual earnings are below the annual threshold.

If an employee has two unconnected jobs which individually pay below the repayment threshold but cumulatively are above the repayment threshold, no student loan repayments should be deducted through PAYE as each job is looked at separately. However, this position changes if a self-assessment tax return is filed (see below).

Self-assessment

Taxpayers filing a self-assessment tax return will have their student loan repayments calculated as part of the self-assessment process. Payments will be due on 31 January following the tax year and are not included in payments on account. There are some additional points to be aware of when completing a self-assessment tax return:

- If the taxpayer has changed jobs during the tax year, their P60 will only have the student loan repayments from their most recent employment, and details of loan repayments through a previous job will not be shown on their P45. Individuals in this position need to check payslips from their previous employments to include the correct amount of loan repayments on their self-assessment tax return.

- Student loan repayments will be calculated on all earned income (employment income and profits from self-employment). So, if an individual has more than one employment, their repayments will be calculated on the cumulative earnings even if the jobs are unconnected and individually pay below the relevant repayment threshold.

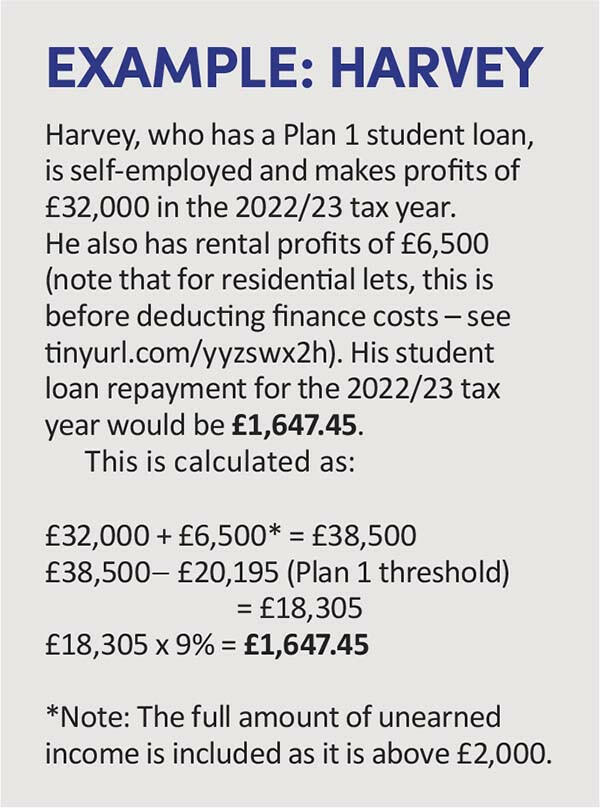

- Where there is earned income above the relevant loan repayment threshold and the taxpayer has unearned income above £2,000 per tax year, then the whole amount of the unearned income is included in the loan repayment calculation (see Example: Harvey).

Image

Nearing full repayment

When coming to the end of repaying student loan(s) there can be a risk of overpaying, so the Student Loans Company recommends that borrowers in the last 23 months of expected repayments switch to paying them directly by direct debit rather than continue paying via HMRC. The Student Loans Company should contact affected borrowers, so it is important that they have up to date contact details for the taxpayer.

More than one student loan

Some borrowers will have more than one student loan. As explained above, loan repayments usually start the April after finishing a course, so if a borrower starts earning above the relevant repayment thresholds upon completion of a second course, then they will start loan repayments for the earlier loan immediately. However, repayments for the second loan will start from April.

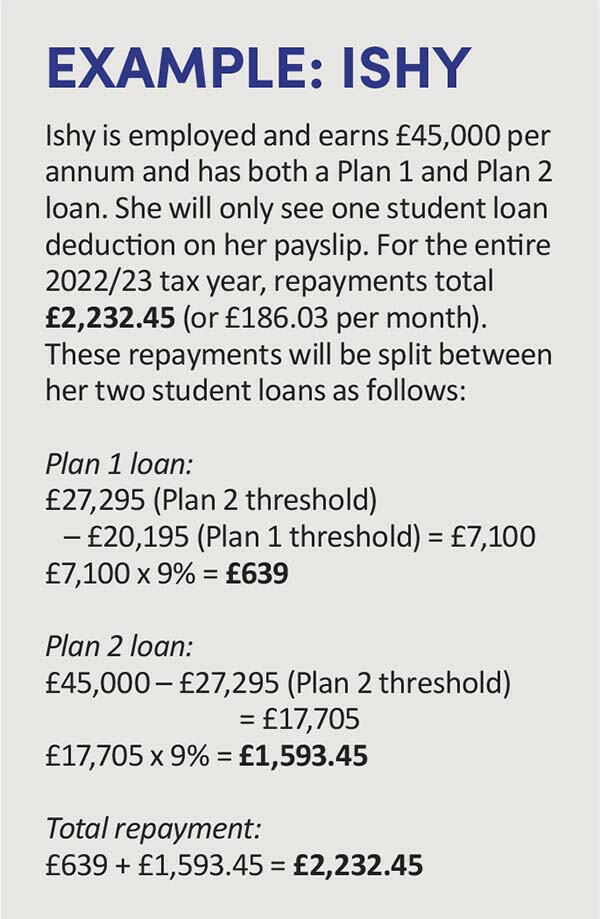

Except for postgraduate loans (see below), one repayment is deducted through the tax system but this is split between the loans. This allocation is best shown in Example: Ishy.

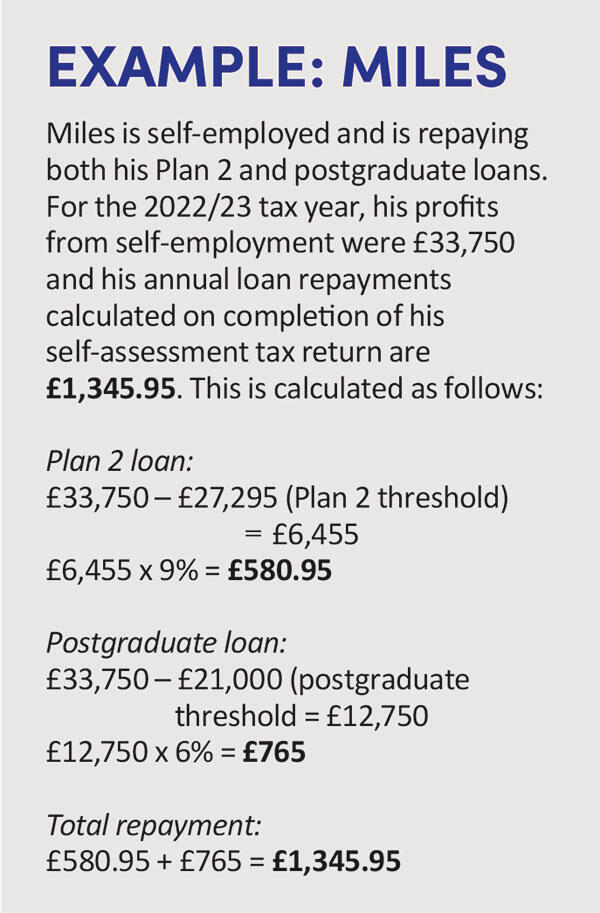

However, when paying back both graduate and postgraduate loans the repayments are calculated and, if applicable, repaid concurrently. This is illustrated in Example: Miles.

Other points to note

This article touches on some of the basic points regarding how student loan repayments are calculated and collected through the tax system but below are a few additional facts that may be helpful.

Cancelling student loans on death

The Tell Us Once process of notifying a death to various government departments such as HMRC does not include the Student Loans Company. It will have to be notified separately to cancel any outstanding student loan debts.

Going abroad

If going abroad for more than three months, the taxpayer must notify the Student Loans Company. Also, if the individual is working and being paid abroad then upon evidence of their salary they will probably make repayments directly to the Student Loans Company through a direct debit, so no longer via HMRC. There are different repayment thresholds for different countries, which are calculated by considering relative costs of living.

On returning to the UK after paying the Student Loans Company directly, there may be an issue when completing the relevant self-assessment tax return. Loan repayments are usually calculated on worldwide income but the overseas income has already been accounted for by the direct repayments to the Student Loans Company. HMRC should be contacted to make sure the taxpayer does not make overpayments.

Future changes for borrowers in England

There have been some recent announcements affecting student loans such as a new loan plan (Plan 5) from September 2023.There are also new Higher Education short course loans available from September 2022 (treated as Plan 2 loans for repayments) and the development of the ‘lifelong loan entitlement’, which aims to allow people to study either full time or in shorter intervals over a longer period. These new loans will continue to be repaid through the tax system and further details will be published in due course.