The summer of tax calculations

Share this article

Jacqui Kimber considers the summer Budget announcements on dividends and the restriction of finance costs

Key Points

What is the issue?

Summer Budget 2015 changed the way individuals are taxed on dividend income and how tax relief is given to residential landlords

What does it mean to me?

If you take most of your income from a company in the form of dividends, you may need to rethink this strategy. For a landlord, the loss of higher rate tax relief could mean increasing rents to preserve profits

What can I take away?

There are some surprising scenarios emerging from the dividend tax changes. However, there is some time to act so consider paying dividends pre-5 April 2016. The interest relief rules are to be phased in over four years from April 2017. Refinancing, particularly in the short term, could be an option for some landlords

Of all the bombshells that rained on tax advisers in the chancellor’s summer Budget one has caused the most debate. This is the scrapping of the UK’s (partial) ‘imputation’ system of taxation of dividends in favour of a series of special rates applying to dividend income. The new rules will apply to dividends paid from 6 April 2016.

Another surprise was the phased restriction of finance costs for individual landlords. Relief will be gradually restricted to the basic rate in relation to interest and other costs of finance, such as guarantee fees, from 6 April 2017.

These changes, along with the removal of the employment allowance for national insurance contributions for companies whose director is the sole employee, will add another factor to consider when deciding the best business structure.

Taxation of dividends

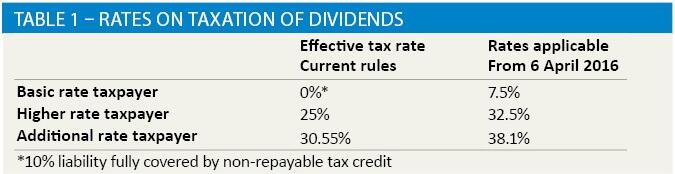

In the chancellor’s defence it could be argued that the imputations system of taxation is a dying breed, New Zealand being one of the remaining notable examples. All that George Osborne has done is continue the work of previous administrations in removing the last traces of the imputation system, which applied in the UK between 1973 and 1999. However, it is surprising that there was no consultation with business or the professional bodies over such a fundamental change, and that there was a conspicuous lack of a policy document accompanying the summer Budget announcement. See Table 1 for the current and proposed rates of tax on dividends.

Osborne confidently stated that these changes would either benefit or be neutral for 85% of taxpayers and simplify a ‘complex and archaic’ system of dividend taxation. Against that benign statement it is worth pointing out a couple of uncomfortable truths.

First, the changes are estimated to raise £6.8 billion of additional revenue for the government over the next five years. There will be winners and losers, but whether this is anything other than a mere revenue-raising measure is not clear, despite the chancellor’s rhetoric.

Second, there are some anomalies in how the rules operate. For example, after taking into account the personal allowance of £10,600 someone receiving a pension of £12,000 and £20,000 of dividend income would, under the current rules, suffer a total income tax liability of £280 (£1,400 x 20%). From 2016/17, based on the same figures, the individual would suffer income tax of £1,405 (£1,400 x 20% + ((£20,000 – £5,000) x 7.5%). However, if the individual had been a higher rate tax payer, say with employment income up to the higher rate threshold (after personal allowance) and £20,000 of dividend income, the tax suffered on £20,000 of dividends reduces from £5,000 (£20,000 x 25%) under current rules to £4,875 ((£20,000 – £5,000) x 32.5%). For an additional rate taxpayer, the saving is even higher: under current rules the tax payable on £20,000 of net dividends is £6,112 compared with £5,715 under the new rules. If dividends represent a modest proportion of overall income, therefore, the new rules offer small savings.

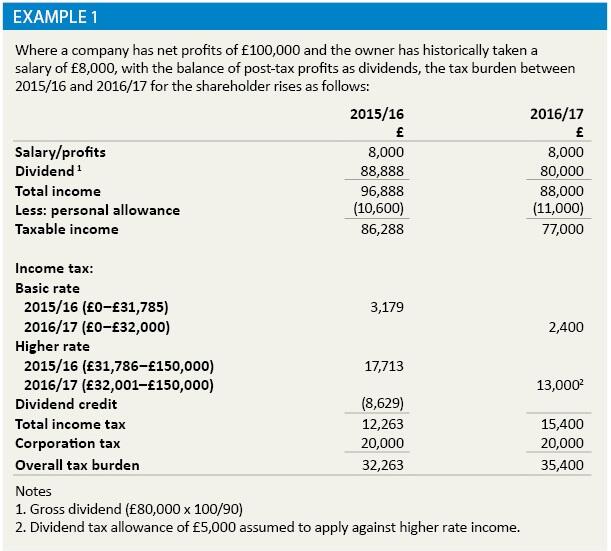

The brunt of the increased tax burden will fall on those with substantial dividend income as an overall proportion of income, whether as wealthy investors (for whom perhaps there will be little public sympathy) to smaller owner-managers who have taken relatively low salaries from the company with the majority of reward coming through dividends. See Example 1.

Incorporation

‘Should I set up a company?’ It is a common client question for most practitioners. The answer always depends on the particular commercial situation, but before the summer Budget statement, it was a safe bet that for many, a company would offer the best tax outcome. This was because of the combination of a low rate of corporation tax and the dividend tax credit system, which resulted in lower effective rates of income tax on extraction of profits by way of dividend. The employment allowance also meant that sole proprietor companies could be tax-effective, even if a salary above the earnings threshold was taken.

The position now is more complex. On one hand, we have the chancellor’s announcement that corporation tax rates will be reduced to 19% from 1 April 2017 and 18% from 1 April 2020 but, on the other, higher rates of tax will be payable on dividends. Although we have the guarantee of no increases in income tax or National Insurance Contributions (NICs) during this parliament, there is no commitment to reducing income tax rates. To do so would be expensive and politically difficult.

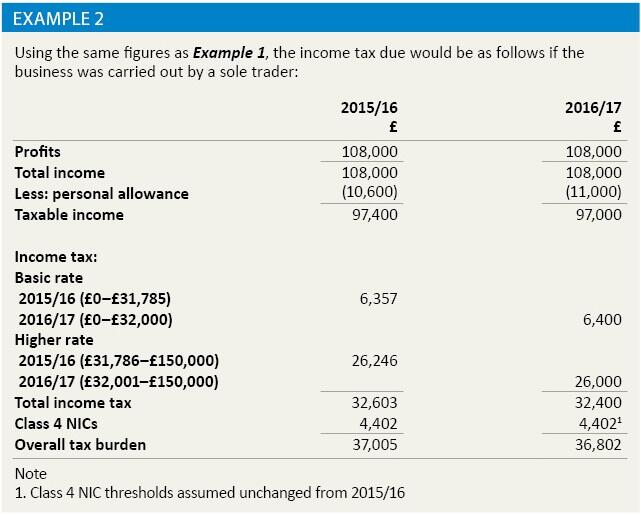

The choice, therefore, is between paying income tax on business profits at rates of up to 45% plus class 4 NICs if the individual chooses to operate as a sole trader or member of an LLP compared with 20% (and decreasing) corporation tax if a company is used, but with higher tax on dividends. Also, the shareholder will no longer benefit from the employment allowance (possibly unless a family member such as a spouse is also employed within the business, although it is difficult to believe HMRC would miss such an obvious planning strategy). However, even with the increased rate of tax on dividends, a company may still offer the better option due to the class 4 NIC burden on the self-employed. See Example 2.

In return for the increase in dividend tax rates, individuals will be given a £5,000 ‘dividend tax allowance’, although whether this will apply to all taxpayers, even those on the 45% additional rate, remains to be seen. There are also questions over how this new allowance will interact with the £1,000 exemption for savings income to be introduced from 6 April 2016 (£500 for higher rate taxpayers), and the savings allowance (£5,000 for 2015/16). It seems unlikely that these two allowances will extend to dividend income. The new dividend tax allowance should, however, ensure that most investors with modest equity portfolios will not pay tax on their dividend income and, more importantly, will not be brought into self-assessment as a result of the change.

Restriction on finance costs for landlords

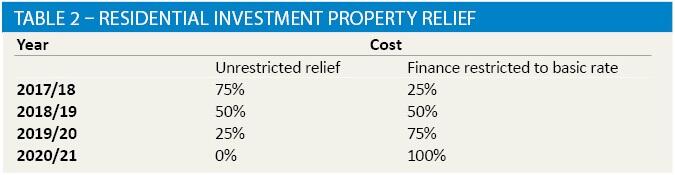

From 6 April 2017, landlords of residential investment property will have tax relief on interest and other finance costs restricted to the basic rate of income tax. Tax relief on commercial property is unaffected. The restriction is to be phased in over four years as set out in Table 2, perhaps to give landlords time to consider raising rents to preserve their rental profits.

The number of private landlords has dramatically increased in recent years, with 15% of mortgages taken out this year on buy-to-let terms. Under pressure to take some of the heat out of the residential property market, private landlords were easy targets for the chancellor. The restriction on tax relief on finance costs will particularly affect landlords who have released funds on rental properties by taking out new or enhanced mortgages to fund non-business expenditure. This type of planning did not appear to offend HMRC in the past, and indeed their manuals make specific reference to it, but it will now be available to owners of commercial investment property only.

There are no restrictions applying to corporate landlords, so the question arises again as to whether a company might be the preferred vehicle to conduct business. Incorporation of an existing property business is unlikely to be cost effective due to stamp duty land tax charges. However, for new properties being acquired for letting, it may be worth setting up a company. Despite the issue of a double layer of taxation to consider, given that the shareholder may have a measure of control over when and to what extent dividends are paid, it may be possible to manage tax liabilities effectively.

Conclusion

There is no indication that anti-forestalling measures will be introduced in advance of the changes to the taxation of dividends or the treatment of finance costs for landlords. To the extent that distributable reserves and cash flow permits, family companies are likely to want to pay out profits before 5 April 2016 to take advantage of the generally lower income tax rates applying under the current regime. Similarly, landlords may wish to consider refinancing, both to increase borrowings against rental profits while full relief is available and to manage interest costs to mitigate the effects of the tax changes.