Is there consideration?

Share this article

Neil Warren gives practical examples of when income is not subject to VAT

Key Points

What is the issue?

The decision about whether VAT is chargeable on a source of income is one of the most important tax challenges for any business or organisation. It is necessary to always consider whether the payment has a direct link to the supply of goods or services.

What does it mean to me?

There can be many grey areas about whether e.g. grants are subject to tax or are outside the scope of VAT. The article gives tips on the logical approach to adopt when determining the VAT liability of each source of income received by an organisation.

What can I take away?

There are occasions when a payment being standard rated as a consideration linked to a taxable supply of goods or services produces a good outcome for all parties, i.e. where both the supplier and customer can claim input tax.

Many readers will know that I question HMRC’s optimistic view that MTD will significantly reduce VAT errors when it is introduced next year. The reason is because so many errors in the world of the nation’s favourite tax are caused by human decision making, rather than processing errors in accounting records.

The decision to charge VAT or otherwise on sales and income is a major challenge for many business owners. In this article, I will consider practical situations where VAT is not charged, focusing on income that is outside the scope of VAT rather than exempt or zero-rated.

Compensation

There are two main reasons why a payment might not be subject to VAT:

- There is not a direct link between a payment and a supply of goods or services

- Where nothing is done in return for the payment

Examples of such payments could include compensation, donations, grants, project funding and some deposits.

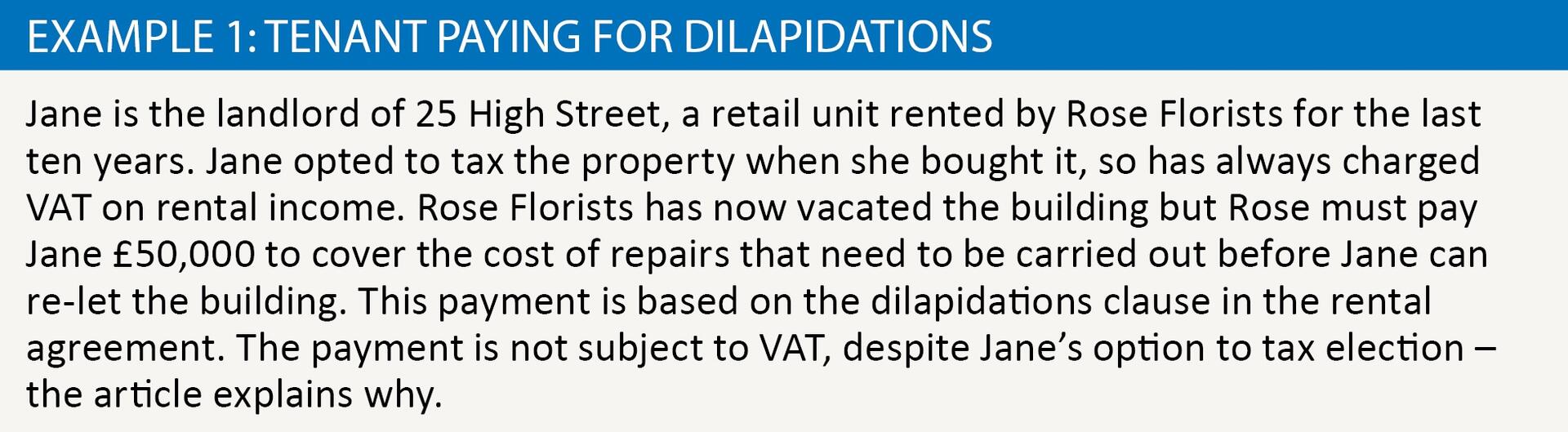

My favourite example of an error made by many property owners is shown at example 1. Jane takes the view (with some logic) that if she has opted to tax her property, then 20% VAT is added to all income connected to the building, subject to the usual overrides, e.g. for residential property. But this is not correct: in this example, the payment does not relate to goods or services that the tenant has received from Jane, and is wholly linked to the condition of the property left by Rose when she departs. The payment relates to damages, i.e. it is compensation rather than consideration, so is outside the scope of VAT (HMRC Notice 742, para 10.12).

What is consideration?

In the final sentence of the last paragraph, I introduced the word ‘consideration’ which is very important in the VAT world. HMRC’s supply manual makes the following definition in policy note VATSC30500:

‘The expression “consideration” means everything received in return for the supply of goods or provision of services...therefore in order that a supply for a consideration can be made, there must be at least two parties and a written or oral agreement between them under which something is done or supplied for the consideration. There is a direct link between the supply and the consideration because the supplier expects something in return for his supply and would not fulfil his obligation unless he thought that payment would be forthcoming.’

This analysis is very important when considering the VAT position for donations and grants.

Donations

Many years ago, I prepared the annual accounts for a rugby club, which received a £3,000 payment each year from a national company. The payment seemed very generous, especially as there was no obvious promotion of the company’s name or logo in any of the club’s literature. The club claimed that the payment was a donation to support local rugby and was therefore not subject to VAT. However, the main carrot for the donor was that it received the right to buy international rugby tickets at Twickenham by utilising the club’s allocation. These tickets are apparently like gold dust, something which I was unaware of at the time as my main sporting passion is linked to the round ball. But what is the VAT position?

HMRC’s supply manual is very helpful at policy note VATSC50400, and lists five key questions to consider (you could also extend these questions to grant income as well):

- Does the donor receive anything in return for the payment?

- Are there any conditions attached to the payment that go beyond merely having to mention it in account statements?

- What will the payments be used for?

- If the donor does not benefit directly, does any third party receive a benefit?

- Is there a contract and what are the terms and conditions?

So ‘yes’ answers to the first two questions make it clear that the company is paying the rugby club for the right to receive an allocation of rugby tickets, which is standard rated (even though the company will still pay for the tickets as a separate transaction, it is the ‘right’ to receive these tickets they are paying for).

Sponsorship

Most questions that I receive from accountants about sponsorship are linked to input tax issues, along the lines of: ‘We have a client who is sponsoring a racing car driver, and the company’s name will appear on the side of the car. Does this mean that input tax can be claimed on all of the car costs as a “sponsorship” expense?’ – and then two minutes later it emerges that the driver is the son of the managing director of the client’s company, i.e. it is really a private expense rather than one that is relevant to a genuine business purpose!

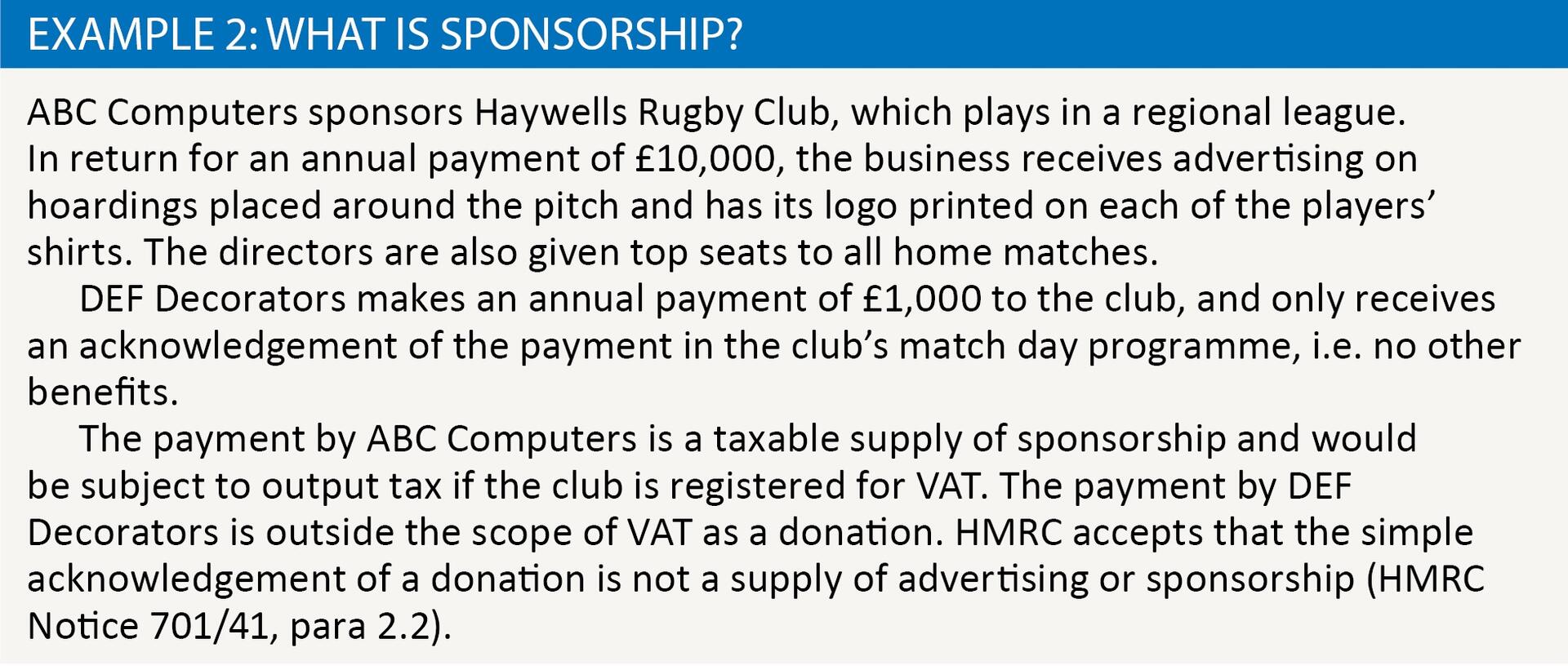

The key point about sponsorship income is that if it is linked to identifiable benefits received by the sponsor, it will always be classed as consideration for a supply. See example 2.

Grant funding

The idea for this article came from some recent consultancy work I carried out, concerning a VAT registered charity that received funding from the local council to take over the running of a public toilet located next to its office. The council’s proposal was to pay an annual grant to the charity in return for the charity opening and closing the toilet each day, and also regularly checking for and reporting any damage to the council. The council would still carry out maintenance and cleaning work.

My thoughts immediately turned to a well-publicised first-Tier tribunal case heard in 2014, involving Woking Museum and Arts and Crafts Centre (TC3315). The case considered payments made by Woking Borough Council to the charity in return for running a local museum, plus an arts and crafts centre and visitor information services. The court agreed with the taxpayer that the grant payments were standard rated because the taxpayer had to carry out a range of services, these services being clearly specified in the grant contract.

The same VAT questions that I considered earlier for donation income are also relevant to grants. There are usually conditions attached to a grant but this does not necessarily mean that it automatically becomes subject to VAT. The conditions are mostly in place to ensure that the money is spent wisely by the recipients. However, this is not the case if the business or organisation that receives the grant must deliver specific services that would be taxable, such as the charity managing the toilets and Woking Museum.

Twist to the tale

You might be wondering why the taxpayer in the Woking case claimed that grant income received from Woking Borough Council was standard rated, whereas HMRC’s approach was that it was outside the scope of VAT. Why would HMRC decline all of that lovely output tax being offered by the charity, I hear you ask? The reason is because the VAT charge by the charity meant that all input tax on the related costs of running the museum became linked to a taxable supply of services and could therefore be claimed. And the 20% VAT charge was not a problem to the council because local authorities can claim VAT on costs linked to their non-business community expenses under a ‘section 33’ claim. This is a final important point to conclude this article, namely that a supply being standard rated rather than outside the scope of VAT can sometimes be a winner for both the supplier and customer.