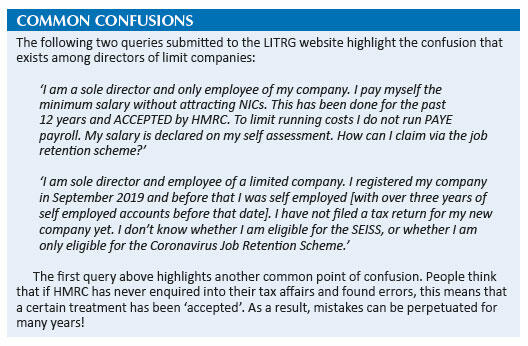

Unforeseen complexities

Share this article

Victoria Todd considers the various difficulties that low-income, unrepresented taxpayers can face when working through a limited company

Key Points

What is the issue?

Over recent years, LITRG has seen an increase in the number of low-income, unrepresented taxpayers put into limited companies without their knowledge or who have set up a limited company without fully understanding the consequences and without proper advice.

What does it mean for me?

You might see clients who have previously set up limited companies without a proper understanding of the obligati ons and consequences or who have been put into limited companies by an enti ty in their supply chain, and who have compliance issues to deal with.

What can I take away?

It is cheap and easy to set up a limited company. Limited companies are not well understood by unrepresented taxpayers. Although many will struggle to deal with their own corporate compliance, the LITRG website has some informati on highlighti ng what people must think about before se tti ng up a limited company or who need to close one down.

In October 2020, LITRG published a website arti cle ‘Thinking of se tti ng up a limited company? Pause and Think!’ (tinyurl.com/44emautu). Its purpose was to highlight a new guidance section on the LITRG website on working through a limited company (tinyurl.com/47nmd55d). This was the first time LITRG had published information about limited companies.

Some people might assume that limited companies are set up either by represented taxpayers who have taken advice or by unrepresented taxpayers because they have fully researched the positi on and decided that is the best option for them. In many cases, that is true. And indeed, a limited company may well be the right choice for someone setting up a business.

However, over recent years, we (and others, such as TaxAid) have seen an increasing number of low-income, unrepresented taxpayers getting involved in limited companies, having set their company up themselves because a friend or an internet search has suggested that it reduces their tax liability and provides them with protecti on if anything goes wrong; or perhaps because they are under the misconception that to be in business necessitates having a limited company.

As it is so cheap and easy to set up a company, they do so without any understanding of the consequences, including the tax ramifications and the other legal requirements that come with it. Often, people in this situation believe they are self-employed, and they cannot separate out their own affairs from those of the company.

Other low-income, unrepresented taxpayers are told to set up a limited company by an agency or umbrella company in their supply chain. Temporary and flexible work is growing rapidly and such work oft en involves agencies that use umbrella companies.

The umbrella companies sometimes set up, or help to set up, limited companies through which the worker is paid. In some cases, the worker is not aware of the limited company structure. Even if they are aware of it, they might have little choice but to work in this way if they need the job and may not understand what it means.

‘Self-employed directors’

There is longstanding confusion about the difference between self-employment and being a director of a limited company. Throughout the coronavirus pandemic, we have seen numerous references to ‘self-employed directors’ in the media, in Parliamentary debates and on other consumer websites. This confusion is not helped by the fact that universal credit treats most single/partner company directors as if they were self-employed. We explain more about this on our website www.revenuebenefits.org.uk (see tinyurl.com/vtdfas4t).

It is therefore not surprising that we have seen cases, brought to light by the coronavirus support schemes, where people have not understood that their company’s money is not strictly their own.

One example we know of is someone who set up a small gym/personal training business with a friend six months before the pandemic started. Previously, they were both self-employed personal trainers. Both are low-income workers. A friend told them they should incorporate because it would protect them if anything went wrong, which they did through an online company for £20. Both tried to claim grants from the Self-Employment Income Support Scheme (SEISS) during the pandemic as they thought they were self-employed and were trading. They were not eligible. That they had been withdrawing money from the company in the belief it was theirs, as it was when they were self-employed. They did not understand that the money belonged to the company. They had not taken any steps to set up a payroll or deal with any of the tax requirements for the company, such as registering with HMRC. They thought it would all be declared on their next tax return, as they had always declared their self-employed earnings.

This is not an unusual case. It takes just over 10 minutes and can cost as little as £12 to set up a limited company online.

Agency workers

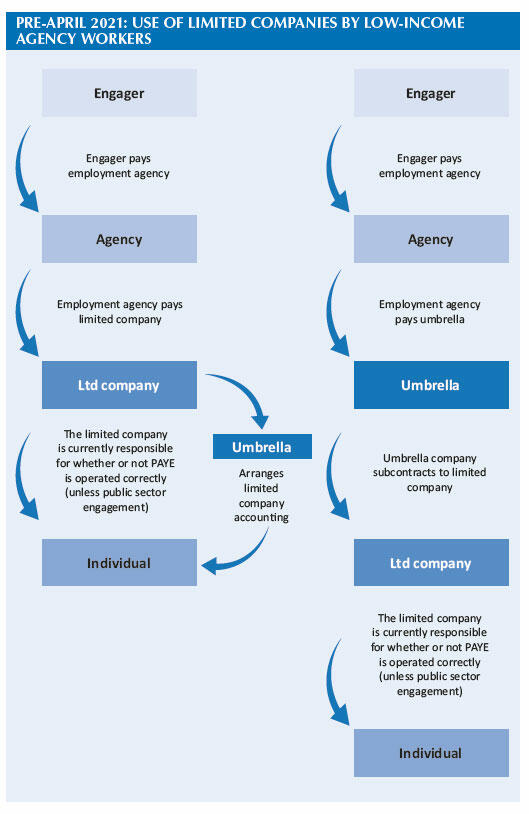

Historically (pre 6 April 2021), there has been a problem with lower-paid workers being encouraged or put into limited companies inappropriately at the behest of agencies and umbrella companies.

In some cases, a limited company was used as an alternative to an umbrella company in a supply chain; in other cases, it was used by an umbrella company to form another level in the supply chain between the engager and the worker (see the diagram on the next page for details).

In the first model, often workers may not have fully understood the implications of having a limited company. This could have damaging consequences; for instance, if the relationship between the worker and the limited company accountant breaks down (sometimes the accountants involved will not belong to a professional body and have minimal contact with their clients) and the worker falls into non-compliance.

In the second model, some lower paid workers may not have even realised that a limited company had been established on their behalf, again leading to non-compliance.

The driving force behind having a limited company at some point in a low-income agency worker supply chain has usually been to increase profit and/or reduce obligations. If an agency or umbrella pays a limited company rather than a worker, then it is a business-to-business transaction and they do not have any ‘employer’ costs or responsibilities, which can save them money.

There can also be an additional revenue stream created from the fact that most workers in limited companies will need help from an accountant with running the limited company and so can be charged for this service. We look at this state of affairs in more detail in our recent report on employment intermediaries (see tinyurl.com/2jedh97c). The recent off-payroll changes will likely have removed the limited company incentive in this particular situation going forward.

Case study

The following correspondence is an example that sets out some of these issues:

‘I have been an agency lorry driver for the last nine years. I have had only one day of driving in the last three weeks, as all the firms that I drive for are closing down due to Covid-19. I have all my previous wages and tax returns on file.’

The person in this correspondence refers to himself as an agency driver. However, we discovered through further correspondence that he had been handed to an umbrella company, which in turn had set up a limited company.

The writer viewed himself as an agency worker or an employee of his umbrella company. He could simply not understand why his umbrella company would not furlough him and claim support with his wages through the Coronavirus Job Retention Scheme (CJRS). The answer was that they could not furlough him: they had set up a limited company for him and, as a director of his own limited company, he had to furlough himself (because he was employed by his own limited company, not the umbrella company). Furthermore, he had no personal relationship with the umbrella company accountants who did his books and did not know how to get hold of the information he needed to make the CJRS claim on behalf of his limited company, let alone be able to do complex calculations.

In the end, with help from us to understand the situation and break the deadlock, we were told that the umbrella company accountants helped him to prepare a CJRS grant claim, for a further fee. As noted above, often those providing the accountancy services are not members of any professional body.

HMRC engagement

We have raised these issues with HMRC. For example, we raised the issue of people in limited companies trying to claim SEISS because they thought they were self-employed. HMRC welcomed our input and suggestions for changes to the GOV.UK guidance – which now makes it clear that you cannot claim SEISS if you are trading through a limited company.

We are concerned that the off-payroll changes in the private sector, from 6 April 2021, will cause a shift of workers from limited companies to umbrella companies and a mass abandonment of limited companies. (HMRC estimates that 180,000 personal service companies will be affected by these changes.) Some of these will be low-income workers, such as the person in the case study above, who may be left to deal with trailing liabilities and messy compliance issues if the limited companies are not closed down properly.

Those at the low-income end of the income spectrum often have very little understanding of how personal service companies operate. In our experience, they often cannot separate out their own affairs from those of the personal service company, and stand very little chance of closing down the personal service company’s tax affairs correctly, let alone dealing with the Companies House requirements.

While our experience is that Companies House is really helpful in striking off a company, things can get complicated where a creditor or HMRC object to the striking off. This may well happen in these cases, if there are outstanding corporation tax (or VAT or PAYE) issues.

We have raised these points in recent consultation responses with HMRC and have recently met with HMRC officials to discuss in further detail.

LITRG’s response

At LITRG, we have been highlighting limited company issues for a number of years in our consultation responses.

However, we have started to see more cases involving limited companies in recent times. TaxAid has also reported an increase in people seeking such help, but it does not have the resource or capacity to help with limited company issues. We therefore felt we needed to produce some guidance to:

- educate people and raise awareness about limited companies and the consequences of setting one up;

- help people to understand the differences between self-employment and being a director of their own company; and

- highlight issues that may impact people following the April 2021 off-payroll changes.

Our free website guidance covers these issues in outline, helping low-income, unrepresented taxpayers to understand more about limited companies and how to start to unravel problems if they find themselves in a difficult situation.

However, due to the complex nature of trading through a company, we also stress that people should seek professional help and, where people can afford to pay for advice, we recommend approaching a CIOT or ATT member.