VAT savings tips for SMEs: practical ways to improve cash flow

Share this article

At a time of rising costs for business owners, here are some practical tips about how a small business could reduce its VAT bills or improve its cash flow.

Key Points

What is the issue?

If a business cannot fully claim input tax – because it is not registered for VAT or is partially exempt – check opportunities to reduce VAT on expenses. For example, ask a property landlord if they can revoke their option to tax election with HMRC and not charge VAT on future rental invoices.

What does it mean for me?

It is important to review VAT issues affecting businesses at least once a year. For example, could they adopt and benefit from VAT schemes such as cash accounting or might it be worthwhile for them to leave a particular scheme?

What can I take away?

If a business is VAT registered and imports goods, make sure it elects for postponed VAT accounting, which is a cash flow winner for any business and also speeds up the process of importing goods into the country. Finally, be prepared to challenge penalties issued by HMRC if they are unreasonable.

VAT is often the forgotten tax. Charge VAT on your sales and claim it back on your expenses. Submit and pay a return once a quarter. End of story.

However, there are many concessions and opportunities in the legislation to reduce the VAT bill at the end of a period and also to improve the VAT cash flow for a business. An obvious example is the cash accounting scheme, available to a business with annual taxable sales of £1.35 million or less excluding VAT, where output tax is not declared on a return until customers have paid their dues. Input tax cannot be claimed until suppliers have been paid but it is a winner in most cases because debtors usually exceed creditors.

In this article, I’ll consider some potential VAT savers and cash flow opportunities.

Saving VAT on premises rent

For any business or organisation that is either not registered for VAT or is registered but partially exempt, then VAT paid on overheads will be a cost to the business. A major overhead is usually the rent of an office or other trading premises, where the landlord will often charge VAT because they have opted to tax their interest in the building.

However, there is potential good news for tenants: if a landlord opted to tax their interest in a building more than 20 years ago, they can revoke it in most cases by submitting form VAT1614J to HMRC. Future income they earn from the building – rent and selling proceeds – will be exempt from VAT. The priority is to ask landlords if they made their election more than 20 years ago – tenants could perhaps offer to pay some extra rent as an incentive. The option to tax rules were introduced in 1989, so many elections have been in place for more than 20 years and can be revoked.

Input tax: staff benefits

There are many opportunities to claim input tax on staff-related expenses. For example, input tax can be claimed on the costs of entertaining staff but not for non-employees; e.g. suppliers or customers.

As a VAT saving tip – particularly relevant to the construction industry – input tax can also be claimed on the subsistence expenses of subcontractors paid for by a business, as long as the subcontractors are treated the same as employees (see VAT Notice 700/65, para 2.3).

However, there are many other staff expenses where input tax can be claimed, for example:

- accommodation provided to employees in many cases;

- gym memberships available to all staff;

- relocation expenses; and

- protective clothing and staff uniforms, such as wigs and gowns for a barrister to wear in court.

Here is a potential VAT trap: even though input tax can be claimed on the costs of entertaining staff – for example, the office Christmas party – there is an input tax block where the role of staff at an event is to act as host for the guests (see VAT Notice 700/65, para 3.3).

Save VAT by deregistering?

A recent VAT query I dealt with involved a retail business with annual sales of £90,000 including VAT. Turnover had been consistent at this level for many years. All sales are standard rated, so VAT exclusive sales are £75,000. I asked the client’s accountant if deregistration was an option on the basis that taxable sales in the next 12 months are expected to be less than the deregistration threshold of £83,000: ‘They wouldn’t be,’ he said, ‘because they will still be £90,000. The client sells her goods on a VAT inclusive basis.’

The accountant is correct but if the client reduced her prices by 10% when she deregistered, her gross sales will now be £81,000 – and therefore less than £83,000. The VAT saving is being shared with her customers, although her loss of input tax must be considered.

Many service businesses might be able to reduce their turnover below the deregistration threshold by working fewer hours. The benefits of a four-day working week are being well publicised at the moment. Again, this strategy would only have potential gains if customers are unable to claim input tax and if prices are increased to offset the loss of input tax caused by deregistration.

Note: don’t forget about a potential output tax liability on the final VAT return for stock and assets still owned by a business on the deregistration date, where input tax was claimed when they were purchased.

Annual windfall: partial exemption de minimis limits

If a partially exempt business qualifies as de minimis in a VAT quarter or tax year, it can claim input tax on costs that relate to its exempt activities. The main de minimis test is that exempt input tax (including the proportion of input tax not claimed on general overheads and mixed costs) must be less than £625 per month on average and also less than 50% of total input tax – a potential annual bonus of up to £7,500.

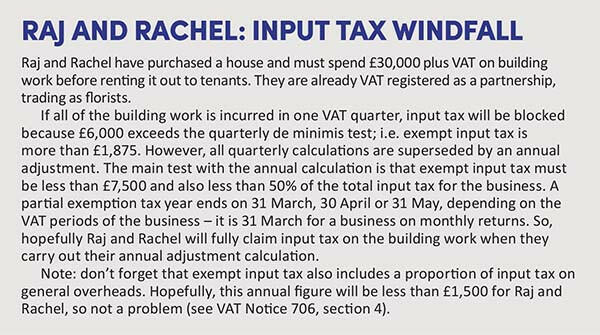

The impact of partial exemption can be wider than is often realised. See Raj and Rachel: input tax windfall.

Note: a property purchased in joint names is always classed as a partnership (see VAT Notice 742A, para 7.3).

Outside the scope income: register for VAT?

Imagine that you have taken on a new client, a lawyer, who only provides legal services for businesses in America. Her annual fees are £100,000 and she is not VAT registered.

The reason why she does not need to register for VAT is because her fees are outside the scope of VAT under the general place of supply rule for B2B services – and not taxable – as the place of supply is America where her customers are based. However, there is a potential VAT saver here:

- A UK business can still register for VAT and claim input tax if the services they provide for overseas customers would be VATable if supplied to UK customers; i.e. subject to VAT at 0%, 5% or 20%. Legal services are standard rated, so tick this box. This outcome is often known in VAT speak as ‘outside the scope with recovery’.

- The VAT registration will be voluntary and the legislation allows it to be backdated by up to four years if requested by a taxpayer. This produces an excellent outcome for our lawyer because no output tax is payable on her past income but there is a four-year input tax windfall on her UK expenses.

- On the first long-period VAT return, she can take advantage of another concession and claim input tax on some pre-registration expenses – stock and assets bought by her business in the previous four years and still owned on her registration date, with a six-month window for services.

Postponed VAT accounting

The message has got around – hopefully – that postponed VAT accounting is a ‘win win’ for all imports of goods as a VAT cash flow saver for a business. It means that no import VAT is payable when goods arrive in Great Britain from outside the UK (or outside the EU in the case of a Northern Ireland business) and a reverse charge entry is made on the next return by the importer. The reverse charge entries are based on the VAT shown on monthly import VAT statements, which can be downloaded from HMRC’s Customs Declaration Service. An election is made for postponed VAT accounting on each shipment of goods.

Note: the Box 4 entry of the reverse charge must take account of any input tax reduction needed for exempt, private or non-business use of the goods in question.

Challenge VAT penalties

Human error; careless error; deliberate error. Underpayments of VAT on past returns are categorised into one of these behavioural groups by HMRC officers issuing an assessment. The penalty for underpayments is based on a percentage of the tax underpaid, and the penalty rate rises according to the severity of the taxpayer’s behaviour. There is no penalty for human errors but a maximum penalty of 100% for underpayments that are deemed to be ‘deliberate and concealed’.

As well as being prepared to challenge HMRC’s categorisation of an underpayment if it is unfair, advisers should also ask HMRC to suspend a penalty in the case of careless errors, if it relates to weaknesses in the accounting system that can be corrected. And, finally, make sure that the mitigation allowed by HMRC for co-operating with their enquiry is reasonable. The reductions in the maximum penalty percentages are often known as the ‘telling, allowing and giving’ concessions.