Winners and Losers

Share this article

Stephen Relf and Meg Wilson look at the upcoming changes to NICs

Key Points

What is the issue?

From April 2018, Class 2 NICs will be abolished and Class 4 NICs will be restructured to give the self-employed access to contributory benefits.

What does it mean to me?

There will be winners and losers as a result of the changes. Some self-employed individuals may need help in understanding their options and may benefit from paying additional NICs before April 2018.

What can I take away?

An awareness of the rules for NICs for the self-employed for 2018/19 onwards.

Following Philip Hammond’s decision to abandon planned increases in Class 4 NICs, you could be forgiven for thinking that there will be no changes to NICs for the self-employed in the near future. And yet government announcements made prior to the calling of the general election suggest that significant change is on the horizon: from April 2018, Class 2 NICs will be abolished and Class 4 NICs will be restructured to give the self-employed access to contributory benefits. For most self-employed people, this will mean more money in their pocket from the Class 2 NICs saved, and little else. However, the changes will not be welcomed by all and those paying Class 2 NICs on a voluntary basis will be hardest hit. This article considers the impact of the changes on the basis that they will be enacted in the next Parliament.

The current system: 2017/18

For 2017/18, the self-employed pay two classes of NICs: Class 2 and Class 4, and they are quite different: whereas Class 2 NICs are paid at a flat rate and give access to contributory benefits, Class 4 NICs are calculated as a percentage of profits and carry entitlement to, well, nothing.

A self-employed person with profits for the year equal to or in excess of the Small Profits Threshold (SPT; £6,025) pays Class 2 NICs at the rate of £2.85 for each week of self-employment in the tax year. A self-employed person with profits lower than the SPT has the option of paying Class 2 NICs on a voluntary basis. This is a popular feature of the system as it allows people who may not be able to do so otherwise to build entitlement to contributory benefits.

Class 4 NICs are calculated as shown in table 1.

The system for 2018/19 onwards

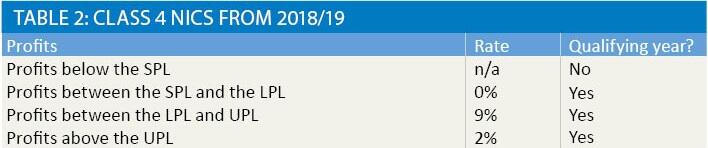

As stated above, from 2018/19, Class 2 NICs will be abolished and Class 4 NICs will be restructured to give access to contributory benefits for the self-employed. The main change to Class 4 NICs will be the introduction of a new Small Profits Limit (SPL). A self-employed person with profits above the SPL and below the LPL will be treated as having paid Class 4 NICs, giving that person a qualifying year for benefit entitlement purposes. The new SPL is similar to the Lower Earnings Limit (LEL) for primary Class 1 NICs and the government has stated that the SPL will be aligned with the LEL.

Therefore, Class 4 NICs will work as shown in table 2 from 2018/19.

A self-employed person with profits below the SPL may pay Class 3 NICs in order to secure access to contributory benefits including the State Pension and the contributory Employment and Support Allowance. The rate of Class 3 NICs is currently £14.25 per week. A single qualifying year of Class 1 or Class 4 NICs will secure access to Bereavement Support Payment (BSP).

Winners and losers

There are two main reasons for the change: (1) to make NICs for the self-employed simpler to understand and administer; and (2) to make the system fairer so that the self-employed have access to contributory benefits, and so those benefits can be accessed on a more equal basis. It seems reasonable to assume that the changes will deliver on the first objective: replacing two classes of NICs with one should make it easier for people to understand and calculate their liability, and for HMRC to collect it; but will it create a fairer system?

The government estimates that approximately 5.4 million people will be directly affected by these changes, and that this group as a whole will be better off to the tune of £360m a year once the changes bed in. However, there will be individual winners and losers, with quite different results depending on whether profits are less or more than the SPL. A person with profits above the SPL will have most to gain from the changes, paying £148.20 less for the same level of access to contributory benefits. As we will see, the position is quite different for those with profits below the SPL.

As stated above, a person with small profits who wants to secure access to contributory benefits will need to pay Class 3 NICs. Using 2017/18 figures, this is £741. In 2017/18, that person would have paid Class 2 NICs of £148.20 for a similar level of access. Therefore, as a result of these changes the self-employed person with very low profits will need to pay roughly £600 more. To put it another way, as a result of these changes the poorest self-employed will see their NICs bill increase by a factor of 5.

This point was made to the government during the consultation process by a number of bodies, including the Low Incomes Tax Reform Group (LITRG). In response, the government quoted figures showing that approximately 77% of people with profits below the SPL will have their State Pension record protected by payment or deemed payment of Class 1 NICs, or by NI credits, or they will already have a full State Pension record. In addition, the government pointed out that an individual needs 35 years of NICs and/or NI credits to qualify for the full rate of the new State Pension, meaning that they could have up to 15 years of gaps in their NIC record without affecting their State Pension entitlement.

Based on this, and transitional arrangements around contribution-based Jobseekers Allowance and contributory Employment and Support Allowance, the government expects that only 2% of all self-employed individuals will pay Class 3 NICs. However, 2% of 5.4 million is 108,000; that’s over 100,000 people who will have to pay roughly £600 more in NICs – out of a relatively small amount of profits.

There is some protection for self-employed women. From 2018/19, a woman will need to pay Class 3 NICs in order to access Maternity Allowance (MA) at the standard rate. However, only three Class 3 NICs payments will be required. This means that the cost of MA to the claimant will be roughly the same as the cost under the current system (13 weeks of Class 2 NICs).

Advisers who have clients with profits below the SPL will have an important role to play in communicating the changes and in encouraging/assisting clients to check their NI records and to consider the options open to them. And this will be a long-term commitment; there is a six-year window for paying Class 3 NICs.

For those clients whose profits are currently below the SPT and are likely to fall below the SPL when it’s introduced from April 2018, it may be worth considering paying Class 2 NICs voluntarily while it is available (if not already doing so). Those self-employed clients that haven’t been paying Class 2 NICs consistently should also review their NIC record for the past six years and if there are gaps they should consider voluntarily paying backdated Class 2 NICs for those years.

Special groups of Class 2 NICs payers

Class 2 NICs aren’t restricted to the self-employed; certain groups can pay Class 2 NICs in order to gain access to contributory benefits, often paying at a higher rate. These include share fishermen; volunteer development workers; people working abroad; mariners on foreign vessels and people who are classed as self-employed for NICs purposes, including examiners; foster carers; Ministers of Religion and some landlords. Attention will need to be paid to the revised rules for each group but in broad terms, those voluntarily paying Class 2 NICs will have the option of voluntarily paying Class 3 NICs from April 2018.

When the abolition of Class 2 NICs was first announced, the intention was that the changes would take affect for 2017/18 onwards. Thankfully, we have another year to come to terms with the changes and to advise clients, and HMRC have another year to ensure their systems can cope. Problems with the collection of Class 2 NICs through the Self-Assessment system has been a major issue for Working Together of late; let’s hope that this time around HMRC do all they can to ensure a smooth transition away from Class 2 NICs.