Zero rated and exempt sales: getting the paperwork right

Share this article

Two VAT cases lost by taxpayers have highlighted the need for a business to keep proper evidence to support its zero-rated and exempt sales.

Key Points

What is the issue?

Two recent tribunal cases about medical care and VAT exemption were lost by the taxpayers. A key factor in the decisions was the lack of evidence produced by the suppliers to support their decision to not charge VAT on their fees.

What does it mean for me?

Taxpayers who make sales that are exempt or zero-rated should always hold proper evidence and documents to confirm that no output tax is due on these supplies. For example, proof of shipment must be retained to support the zero-rating of export sales.

What can I take away?

If the supporting evidence retained by a business is insufficient, HMRC can issue a ‘best judgment’ assessment for the last four years to treat sales as standard rated. The assessment could also be subject to interest and penalties.

Two cases recently heard in the First-tier Tribunal have given us an important reminder about VAT and record-keeping: if a business makes any sales or receives income where it does not charge VAT – or charges 5% VAT instead of 20% – then it must keep proper records and accurate information to support its decision. And, most importantly, these records and documents should be made available to HMRC if requested during a compliance review.

I’ll consider the cases in this article and other practical situations where inadequate record keeping could create a major VAT problem. Don’t forget that HMRC has the power to correct errors for the last four years, which could produce a large output tax assessment in many cases.

Medical care or cosmetic treatment?

The starting point in the world of the nation’s favourite tax is that all supplies of goods or services made in the UK by a taxable person are standard rated; some sales then escape a VAT charge because they are either exempt, zero-rated or outside the scope. The goods and services that qualify for zero-rating are listed in Value Added Tax Act (VATA) 1994 Schedule 8 and those which are exempt are contained in Schedule 9. Those supplies subject to 5% VAT – for example, smoking cessation products and children’s car seats – are included in Schedule 7A.

In the recent FTT cases of Illuminate Skin Clinics Ltd [2023] UKFTT 547 and Epem Ltd [2023] UKFTT 627, the court considered whether a range of skin and facial treatments carried out by two businesses run by registered medical practitioners qualified for VAT exemption as medical care or were standard rated as cosmetic treatment. To achieve exemption, the treatment must be carried out by a registered health professional and the purpose of the service must be to protect, maintain or restore the health of the patient. So, for example, a cataract operation qualifies as medical care because it improves the sight of the patient.

The problem with the cases – both won by HMRC – was that the patient records to support the business decision not to charge VAT were either inadequate, completely lacking or not made available to HMRC’s compliance officer because of client confidentiality. There was no third-party documentation or other evidence to support any medical care outcome. To quote the judge in the Epem judgment: ‘Whilst it may have made some VAT-exempt supplies as well, there was no evidence before me on which I could determine the extent of any such supplies.’ And, as a further reminder about the legal position: ‘The burden of proof is on the taxable person, Epem, to show that it made exempt services and the proportion of such services. In the absence of such evidence, the general rule applies and the services are to be treated as standard rated.’

Evidence to support zero-ratings

Going back about a hundred years, I was the Customs and Excise officer in charge of checking the VAT returns of a major UK clothes retailer – they are unfortunately no longer trading.

An important priority was to ensure that the business was correctly applying the zero-rating legislation for children’s clothing. To the credit of the manufacturing and merchandising departments, the record-keeping and audit procedures were impeccable: each garment had its own product card, with details of size measurements, target age range, how the item was advertised in the stores, and how the VAT liability was decided in accordance with the legislation and HMRC’s guidance.

This level of detail was what the judges and HMRC were hoping to find in the medical care cases.

As most advisers will agree, the VAT legislation about food and zero-rating is a minefield of confusion and complexity. It is completely out of date and in need of a major overhaul. It reminds me of a tribute band that needs to sing some fresh songs, rather than churn out the same old tunes from yesteryear. However, suppliers must work hard to achieve their zero-ratings.

I recently visited a well-known bakery to buy a bun and was impressed by the brightly written sign on the pasty display cabinet: ‘Please take care as the freshly baked products may be hot.’ Brilliant! This message is supporting the outcome that there is no sale of VATable hot food taking place, only a zero-rated product that is cooling down after the baking process. I am sure that if I had asked the retail assistant to heat a pasty for me in the microwave, she would have refused because it would then be subject to 20% VAT again. The business has completely ticked the zero-rating boxes.

High risk: export of goods

The biggest risk of an HMRC assessment as far as zero-ratings are concerned is probably for a business that exports goods. The risks have increased since 1 January 2021 because all sales outside of the UK are now classed as an export, including those to the EU.

The evidence retained by an exporter to support its zero-rating forms an important part of the business accounting records and must clearly show that the goods have left the UK and been shipped to another country. The package of evidence must be a healthy combination of both commercial documentation and transport details.

The onus is on the exporter to retain and produce adequate evidence. If this is lacking, HMRC has the power to issue a ‘best judgment’ assessment in accordance with VATA 1994 s 73(1) and treat the goods as being sold in the UK. HMRC Notice 703 has the force of law in both specifying the relevant time period for proof of export to be obtained by a seller – three months – and the quality of evidence that must be sufficient to show that the goods have been shipped abroad.

In the case of Pavan Trading Ltd [2023] UKFTT 79, an HMRC assessment about export evidence was overturned by the tribunal. The judge accused HMRC of ‘picking holes’ in the quality of the company’s export evidence for its sales of goods to America. He allowed the appeal and commented: ‘If ever there was a counsel of perfection for the provision of export documentation, then the appellant has achieved it.’ Well done to the directors!

Sales subject to 5% VAT

The evidence theme repeated itself in the case of Adrian McKiernan [2023] UKFTT 80, who did not keep adequate records to support the fact that he sold coal from his shop, subject to 5% rather than 20% VAT (VATA 1994 Sch 7A Group 1 Item 1). He submitted an error correction notice to HMRC for £61,106 for the period from January 2016 to December 2019, which HMRC rejected because he had not kept sales invoices, till rolls or other records to support the reduced VAT charge. His representative claimed that HMRC should ‘look at the situation from a lenient and sympathetic point of view’ but the judge dismissed the appeal.

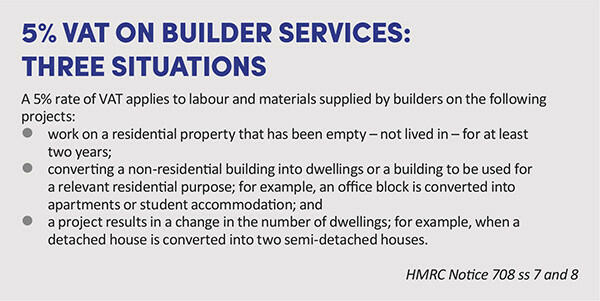

For many advisers, the 5% reduced rate is important for building projects (see 5% VAT on builder services: three situations). In each scenario, the onus is on builders to provide evidence to HMRC, if requested, that supports the 5% charge:

- In the case of the empty property rules, the evidence of a vacant building must be third party data, such as council tax records or information held on the electoral register. A signed statement from the property owner is not acceptable.

- In the case of residential conversions, the builder must be able to produce architectural drawings, photographs or other evidence to show that a building started as, say, an office block, and finished as six apartments that qualified as dwellings.

Outside the scope income

To complete the loop, a business must also be able to provide evidence to support any sales or income sources that are outside the scope of VAT; i.e. where neither a supply of goods nor services has been made in the UK. This is important for charities and not-for-profit organisations which often receive grants and funding from various bodies. HMRC might want to check that there are no conditions attached to the payments which could mean that VATable services are being supplied. The evidence is usually the grant contract and funding documents agreed between the two parties.

Most B2B services supplied to overseas customers are outside the scope of VAT because the place of supply is the customer’s country. It is usually easy to provide evidence to HMRC, if requested, that the customer is based outside the UK and is also in business in their own country. In the case of EU sales, the customer’s VAT number is usually the best evidence.

To share a tale about ‘outside the scope’ income, I recently enjoyed a restaurant meal where the cost was £25 and an extra 10% was added to the bill as an ‘optional service charge’.

The word ‘optional’ was crucial here; it meant that the extra £2.50 was outside the scope of VAT because it was not compulsory. To complete a tight VAT audit trail, the bill also specified the total VAT charged as £4.17; i.e. £25 x 1/6. The boxes had all been ticked to avoid an output tax liability on the service charge.

Conclusion

It might be a good time to check that there are no record-keeping gaps which could give HMRC the power to treat some sales as standard rated rather than exempt or zero-rated. It is important to spread the message that zero-ratings and exemptions are legislative privileges that need to be justified and earned, rather than assumed to be an automatic right.