Pensions paper trail

Share this article

Kelly Sizer reflects on the pensions money purchase annual allowance, how taxpayers might avoid triggering it and compliance pitfalls

Key Points

What is the issue?

The money purchase annual allowance (MPAA) restricts future pension contributions if triggered by taking flexible benefits.

What does it mean to me?

It is important to understand when the MPAA might be triggered, when it might not, and what taxpayers must do if it has been triggered.

What can I take away?

Taking flexible pension benefits brings with it an obligation for the individual to notify not only all other pension schemes of which they are an accruing member that the MPAA has been triggered, but also an ongoing requirement to give such notification to any further schemes they join in the future.

When pensions flexibility (or ‘pensions freedom’) was introduced from 6 April 2015, the government – understandably – wanted to prevent taxpayers from doubling up on tax relief through ‘recycling’, by taking pensions savings out and then re-contributing them. The money purchase annual allowance (MPAA) was therefore introduced by the Taxation of Pensions Act 2014 Schedule 1 Part 4 (amending Finance Act 2004).

Once pension rights have been accessed flexibly, the MPAA effectively limits annual payments into defined contribution schemes by triggering an annual allowance charge if it is exceeded. On introduction from 6 April 2015, the MPAA was set at £10,000 a year, but from 6 April 2017 it was reduced to £4,000 a year. Any unused allowance cannot be carried forward. Triggering the MPAA also means that an alternative annual allowance of £36,000 then applies in respect of defined benefit pension savings.

This article looks at:

- how the MPAA is triggered;

- how the MPAA might not be triggered in certain circumstances; and

- what the taxpayer has to do if the MPAA has been triggered.

Of course, tax advisers must always be wary of the boundary between tax advice and regulated investment business. Members should be familiar with the CIOT’s Professional Rules and Practice Guidelines, which provide more information on this subject.

What triggers the MPAA?

Flexibly accessing money purchase pension rights triggers the MPAA. Flexible access can come in different forms. The individual might, for example, be taking a series of uncrystallised funds pension lump sums, or they might be entering into a flexible annuity contract.

The timing of when an individual first takes a flexible payment and therefore triggers the MPAA is set out in FA 2004 s 227G (for HMRC guidance, see the Pensions Tax Manual (PTM) 056520). If an individual therefore wishes to maximise pension contributions before drawing down accumulated money purchase pots, it will be important to review the timing of the transactions.

How might the MPAA not be triggered?

Some methods of drawing benefit from defined contribution pension schemes do not trigger the MPAA. HMRC’s PTM 056530 gives a list, but it is worth highlighting a couple of them.

First, an individual can still take what we might call a ‘traditional pension’, together with a pension commencement lump sum, and not trigger the MPAA. This might be a life annuity, or a scheme pension (subject to meeting the relevant criteria).

Second, taking ‘small lump sums’ does not trigger the MPAA. This is an important point for people who want to ‘cash in’ pension savings in full.

The MPAA in practice

Let’s consider the example of Philip. He lives in England and has earnings of £20,000 in 2019/20, and no other income. He has three personal pensions:

- Pot A: £8,000

- Pot B: £9,000

- Pot C: £100,000

Philip is 57 and, having developed some health problems, is no longer fit to continue his plumbing business. He has always been a keen photographer and thinks he can pursue this hobby as a new business, but he needs £10,000 to buy some more equipment to get himself up and running. He is averse to getting into debt so is looking at accessing his pensions. He plans to work for at least a further 10 years and is hoping, if successful, that he will be able to top up his pension savings again in the future.

How can Philip raise £10,000 or more, net of tax, without restricting his future pension savings ability?

Using the small pots rules is one potential answer. To find the applicable rules, we have to look at regulations made under FA 2004 s 164 – The Registered Pension Schemes (Authorised Payments) Regulations 2009, SI 2009/1171. Regulation 11A allows personal pension scheme benefits up to £10,000 to be commuted in full as a lump sum, provided the member has reached the minimum pension age (55 in most circumstances) and has not taken more than two previous such lump sums (meaning that three can be taken in total). Philip could therefore cash in his personal pension pots A and B in full under these small lump sum rules, without triggering the MPAA.

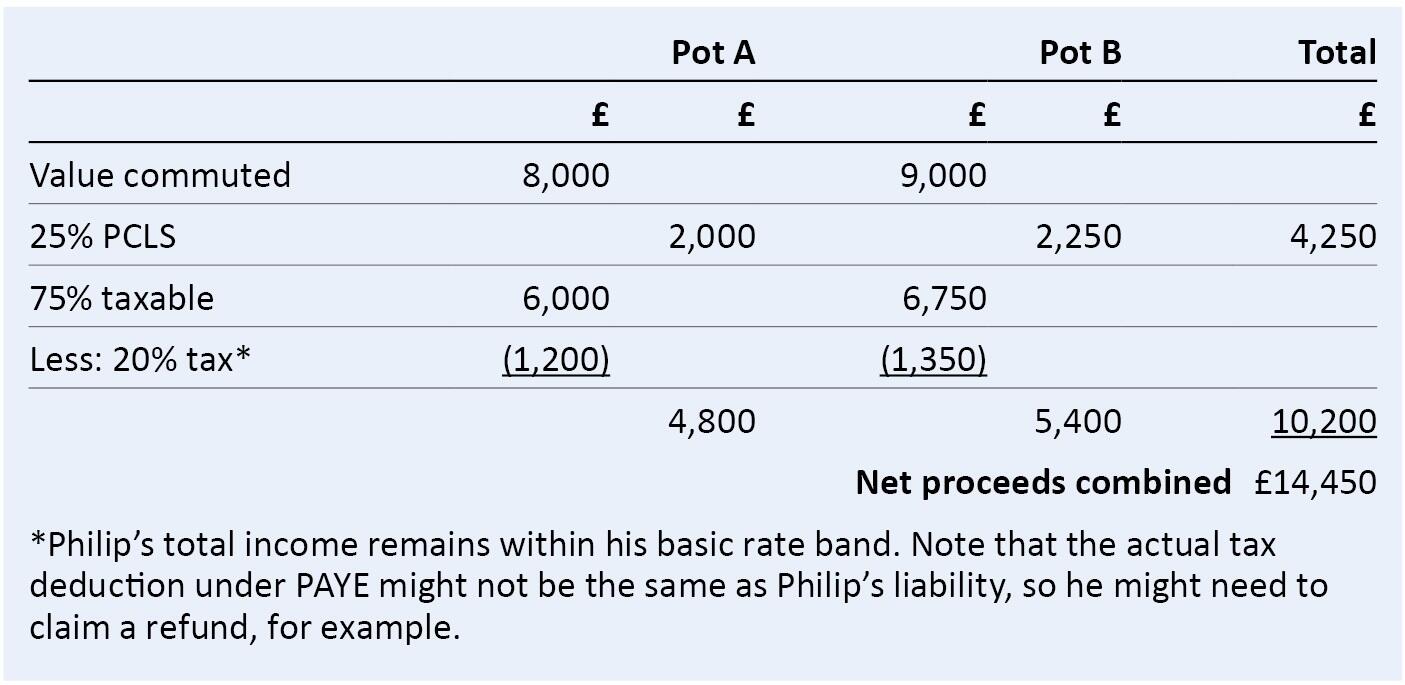

As Philip’s pension savings are uncrystallised at the point of commutation, 25% of each lump sum is non-taxable as these would be pension commencement lump sums (PCLS). The remaining 75% is taxable as pension income in the year of commutation. So, net of tax, Philip will be left with £14,450, as shown in the table below.

Pension providers must notify HMRC via PAYE real-time information (RTI) of taxable authorised payments and under which rules they have been made. The RTI data items list differentiates small pot lump sums from flexible pensions (see items 145, 146, 148 and 168).

When arranging with his pension providers to encash pots A and B, Philip therefore needs to make sure they apply the small lump sum rules, rather than paying the amounts under the flexible pension rules.

MPAA compliance

Philip in the above example might of course only have had personal pension pots exceeding the ‘small pot’ cap of £10,000; say, one pot of £17,000 and the other of £100,000. Nevertheless, deciding he would rather be restricted by the MPAA in future than otherwise borrow to raise the cash he needed, he might have still used pensions flexibility to take the required lump sum.

When an individual flexibly accesses their pension rights under a scheme for the first time, the pension scheme administrator is required under The Registered Pension Schemes (Provision of Information) Regulations 2006, SI 2006/567, Reg 14ZA to provide them with a statement. No such statement is required if the scheme administrator has been notified previously that the individual has previously accessed pension rights under another scheme.

This Reg 14ZA statement must give the date when the individual has first flexibly accessed their pension and explain that the MPAA will apply in respect of relevant future pension inputs. The statement must also explain that the member has obligations to fulfil under Reg 14ZB. See also PTM 166200.

The member’s obligations under Reg 14ZB (see also PTM 166400) are to notify, within 91 days of receipt of the Reg 14ZA statement, any other pension schemes of which they are an accruing member that they have triggered the MPAA. This means that all other registered pension schemes of which the person is an active or contributing member must be notified – not just money purchase schemes. The regulation defines the required notice to be given, but the simplest way of fulfilling the obligation is to pass on a copy of the Reg 14ZA statement itself.

Further, Reg 14ZB imposes an ongoing notification obligation on the individual in respect of any schemes of which they become an accruing member in future. Therefore, if they join a new scheme and start contributing to it, this triggers a further 91 day notification period. It is easy to see how this could be missed; for example, in the context of automatic enrolment into a new scheme on changing jobs. Would someone who had taken flexible pension rights just after the introduction of flexibility in April 2015 remember now that they have a Reg 14ZA notice tucked away in a drawer and realise that they need to dig it out and send a copy to their new employer’s pension scheme administrator? Unlikely, perhaps!

Advisers aware of pension rights having been accessed flexibly might therefore wish to remind their clients of this obligation and check they have fulfilled their Reg 14ZB obligation if they have started contributing to a new pension.

What happens then if people do not give the required notice to their other active pension schemes? In the tax world, we can always be fairly certain that where there is an obligation to do something, there will be a penalty for non-compliance.

And, indeed, there is such a penalty in this instance. TMA 1970 s 98 provides for a penalty of £300, together with daily penalties of up to £60 per day for continued failure. This is applied in respect of multiple obligations (see the table in s 98(5)), amongst which we find obligations imposed by regulations made under FA 2004 s 251(1)(a) or (4). The 2006 regulations above (SI 2006/567) were made by exercising HMRC’s power under s 251, so fall within the scope of s 98.

Interestingly, I can find no mention of this penalty risk for scheme members in the Pensions Tax Manual, though the application of s 98 penalties as far as scheme administrators are concerned is mentioned at PTM 159000. Also, the manual does point out that s 98 penalties can apply to individuals in other instances; for example, in respect of failure to notify HMRC of a loss of fixed protection (PTM 093400).

What is not clear to me is how HMRC would in fact administer penalties for an individual’s failure to meet Reg 14ZB obligations, given that the notification has to be made not to HMRC, but to other pension scheme administrators. Presumably, then, a failure would only come to light if HMRC found on enquiry into an individual’s affairs that the MPAA had been triggered and asked the taxpayer to prove that the notification had been made.

Nevertheless, it is worth advisers helping their clients to avoid falling foul of these somewhat obscure rules by keeping a watchful eye on what they are doing with their pensions and pointing out the paper trail they need to follow.