Preserving heritage: a changing inheritance tax landscape

Share this article

Inheritance tax relief caps threaten estate continuity, demanding liquidity modelling and careful structuring to preserve heritage assets.

Key Points

What is the issue?

From April 2026, agricultural property relief and business property relief will be capped at £2.5 million per individual, fundamentally altering how high-value estates pass between generations.

What does it mean to me?

Heritage and landed estates that once relied on uncapped reliefs may now face significant inheritance tax exposure, creating acute liquidity pressures where wealth is tied up in land, property and trading enterprises rather than cash.

What can I take away?

Succession planning must now focus on valuation, qualification for relief, cash-flow modelling and long-term sustainability. Early, integrated advice is essential to avoid fragmentation, forced sales or erosion of heritage assets.

Heritage estates do not fit neatly into the UK’s inheritance tax framework. They are not simply investment portfolios to be traded or businesses to be broken up. Their value cannot be measured in financial terms alone. A historic house, its contents, surrounding land and diversified enterprises comprise a constellation of assets that support its survival, and function as a single, interdependent ecosystem. Their value is rarely measured purely in financial terms. Continuity, stewardship and public benefit are often just as important as income and capital growth.

For many years, agricultural property relief (APR) and business property relief (BPR) have enabled these estates to pass intact between generations. Subject to satisfying the statutory conditions, both reliefs have operated without an upper cap on the value of the assets, allowing qualifying agricultural and trading assets to attract up to 100% relief from inheritance tax, regardless of value. This uncapped structure has been particularly valuable for large estates and stately homes with extensive land and commercial enterprises that are rich in assets but often constrained in liquidity.

That position is now changing, as HM Treasury seeks to raise revenue and restrict the extent to which high-value agricultural and business assets can pass free of inheritance tax. However, through integrated planning and early professional collaboration, advisers can support clients in navigating a landscape that blends historic tradition with modern fiscal reality.

From preservation to partial protection

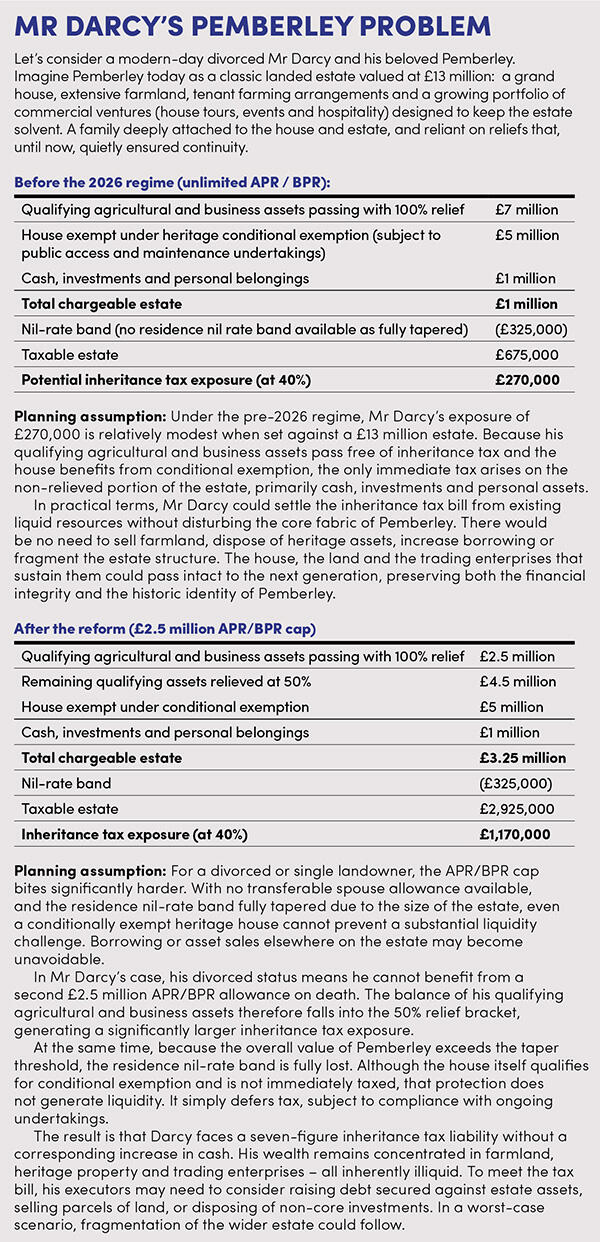

From 6 April 2026, 100% of combined APR and BPR assets will be capped at £2.5 million per individual. Any qualifying value above that threshold will attract reliefs at 50%.

The new regime applies to:

- deaths on or after 6 April 2026;

- potentially exempt transfers (lifetime gifts) made on or after 30 October 2024 where the donor dies within seven years of making the gift; and

- trust structures.

APR continues to apply to qualifying agricultural land, buildings and holdings, while BPR remains available for eligible trading businesses, unquoted shares and certain business property held for the requisite period. The qualification criteria are largely unchanged; what has altered is the scale of relief available.

Following consultation, the originally proposed £1 million cap was increased to £2.5 million and made transferable between spouses and civil partners. This allows up to £5 million of qualifying assets to benefit from full relief on second death. While significant, this combined allowance will still fall short for many substantial heritage estates.

The policy intention is clear: to restrict the extent to which high-value business and agricultural assets can pass free of inheritance tax. However, this risks overlooking the cultural, social and economic roles that country houses and landed estates play within their local communities and across the nation. Capital values may be high, yet income is often modest and directed towards conservation, maintenance and long-term preservation rather than commercial maximisation.

Where tax exposure increases without a corresponding increase in liquidity, the practical consequences may include borrowing, the fragmentation of estates or forced sales – with implications not only for families, but for employment and the preservation of nationally significant heritage.

The reforms mark a decisive shift in philosophy. APR and BPR are no longer mechanisms that can be assumed to secure intact succession. They now mitigate exposure, rather than eliminate it. Planning discussions must therefore now move earlier, be more integrated and focus squarely on valuation, liquidity and long-term sustainability in a post-cap environment.

Liquidity and longstanding vulnerabilities

One of the most profound consequences of the reforms is the renewed emphasis on liquidity. The stereotypical English estate – extensive land, a house of architectural and emotional value, modest income and minimal cash – has always been structurally vulnerable. Until now, APR and BPR largely concealed that vulnerability. Under the new regime, that protection is no longer absolute. Even with the ability to pay inheritance tax on qualifying assets by interest-free instalments over ten years, an effective 20% charge on value above the relief cap may materially affect viability.

Advisers may find themselves in difficult discussions with clients who are deeply attached to their property and its history, yet confronted by hard financial realities. Questions around land sales, borrowing or expanded commercialisation are now becoming unavoidable. For many heritage estates, separating agricultural land from the enterprises that support the historic house – or detaching the house from the wider estate – is neither practical nor desirable. Such fragmentation could diminish both financial viability and heritage significance. Yet many families will now confront precisely this dilemma: whether the family seat can be retained when the numbers no longer align.

For generations accustomed to passing estates intact, cash flow constraints can become crippling. Heritage estates often generate relatively low yield compared to net asset value, leaving owners ‘asset rich but cash poor’.

If heirs cannot meet inheritance tax liabilities without releasing capital, they may be forced to sell land, heritage assets or family treasures, risking the integrity of long-held estates. Even with instalment options, many estates lack sufficient income to meet staggered payments without monetising assets – particularly against a backdrop of rising National Insurance contributions and the forthcoming ‘mansion tax’.

Alongside inheritance tax reform, the Autumn Budget 2025 introduced a new high value council tax surcharge, dubbed the ‘mansion tax’. From 1 April 2028, properties valued above £2 million (based on 2026 valuations) will attract an annual surcharge on top of council tax, payable by the owner rather than the occupier, of £2,500 per year for properties between £2 million and £2.5 million. This rises to £7,500 per year where properties exceed £5 million.

This annual levy adds another layer of cost for high value property owners at the very moment they are re-evaluating estate strategies under the new inheritance tax regime. The charge does not itself alter inheritance tax reliefs, but it does change cash flow considerations. For estates already grappling with instalment payments on inheritance tax, ongoing annual charges further constrain liquidity.

The stately home problem

One of the most difficult aspects of advising heritage clients is explaining that historic importance does not, in itself, confer tax protection. While agricultural land and trading businesses may qualify for relief, the house itself frequently does not.

Land genuinely used for agricultural purposes – supported by appropriate valuation evidence and use tests – may qualify for APR. However, other land or buildings that do not meet the statutory definition of agricultural property will not benefit from the relief, even if forming part of the traditional estate. This can come as a shock to families who have long assumed that the house and land are treated as a single protected unit. The issue is not new, but the cap brings it into sharper focus.

Advisers should be carefully considering whether entering into the Conditional Exemption Tax Incentive Scheme may help to mitigate inheritance tax exposure for heritage assets of national importance.

What is conditional exemption?

The Conditional Exemption Tax Incentive Scheme allows heritage assets of outstanding historic, artistic or scientific importance – such as country houses, land or significant collections – to be exempt from inheritance tax, provided HMRC accepts their national importance and the owner enters into binding undertakings. These typically require proper maintenance and reasonable public access. The relief operates as a deferral of tax for as long as the conditions are met, but tax can crystallise if the undertakings are breached or the asset is sold without qualifying replacement. In certain circumstances, the scheme can also apply to lifetime transfers and capital gains tax.

Commercialisation and qualification for BPR

The distinction between qualifying and non-qualifying activities will become increasingly important as estates seek to maximise the limited 100% relief allowance. Many heritage estates have diversified into weddings, filming, visitor attractions, guided tours, farm shops, cafés and seasonal events. Clearly documented trading activities attract BPR where conditions are met, while also increasing revenue streams to fund inheritance tax liabilities.

However, HMRC scrutiny post-2026 is likely to intensify. Mixed-use cases will require careful analysis and robust evidence to satisfy trading tests. Passive ownership dressed up as commercial activity will not suffice. Advisers should ensure that there are comprehensive records evidencing trading intent, operational substance, commercial risk and genuine profitability.

Impact on existing estate planning

The introduction of the cap forces advisers to revisit open market valuations across the estate, particularly in relation to land that may not qualify for APR, commercial elements that may attract BPR, and any corporate vehicles used to hold heritage assets or trading ventures.

Even where relief is available, significant inheritance tax liabilities may remain. Advisers must therefore evaluate how those liabilities will be funded, including the availability of liquid reserves, the potential use of insured funding mechanisms such as life policies linked to projected exposure, and whether borrowing on favourable terms may be preferable to triggering the sale of heritage or core estate assets.

Across private client planning, familiar tools – including wills, trusts, lifetime gifting, corporate structures and heritage reliefs – remain relevant but none should be viewed as standalone solutions. A holistic approach is essential.

Many existing wills and trust arrangements were drafted when APR and BPR were uncapped, often assuming that qualifying assets would pass free of inheritance tax and that liquidity would not present an issue. This assumption can no longer be relied upon. Private client lawyers are actively reviewing existing documents and updating them to reflect the new relief caps and the increased likelihood of liquidity pressures on death.

Lifetime gifting continues to reduce taxable estates, but such gifts now consume part of the £2.5 million relief allowance. Incapacity planning should also be reviewed, particularly where attorneys have the power to make lifetime gifts. Advisers should examine historic lifetime transfers to determine whether the new limits could apply if the donor fails to survive the relevant period.

Trusts remain an important planning mechanism for heritage and complex estate, but they are not immune from reform. Each trust has its own £2.5 million 100% relief allowance, but this is not refreshed automatically. Periodic and exit charges must now be modelled carefully where APR and BPR assets exceed the cap. Therefore, trusts should be evaluated on case by case basis, and not assumed to be a magic bullet.

In conclusion

In this new environment, co-ordination and realism are essential. For accountants, financial planners and lawyers, mastering these reforms is not optional. Robust planning now may help to ensure that stately homes and heritage assets endure for future generations, without unintended forced sales or disruption to family legacies.

All private client advisers must work together to safeguard the future of these irreplaceable heritage assets. Trusted valuers must be welcomed into ‘the fold’ and we actively need to build a network of professional connections to support our clients. Robust valuations, careful analysis of qualification for relief, realistic cash-flow modelling and timely review of existing structures are essential. Our advice and support will be crucial to fulfilling our duty of care to clients whose lives, legacies and heritage hinge on effective strategic planning.

Figures are illustrative only. Actual outcomes will depend on valuation, qualification for reliefs, availability of nil-rate bands and individual circumstances.